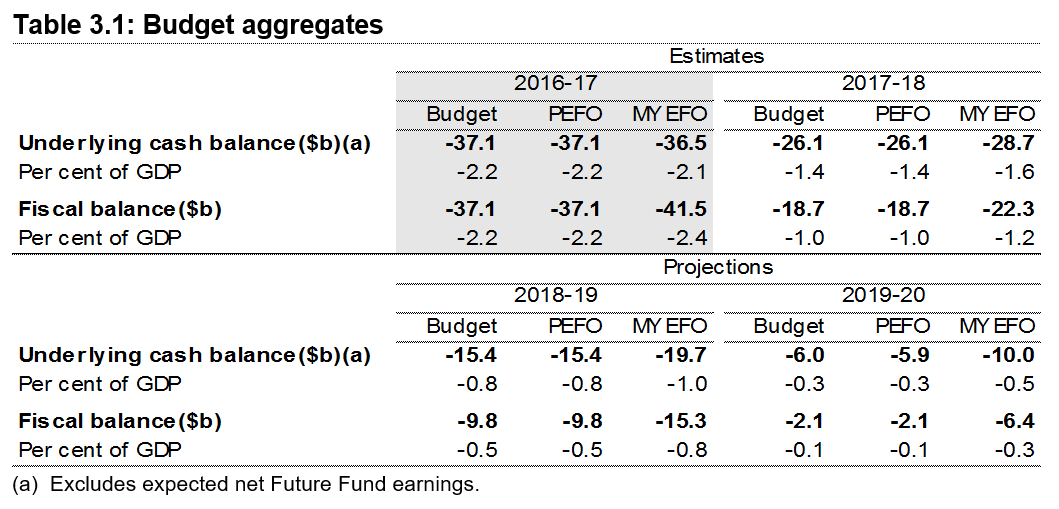

He just never learns. Having placed the nation on downgrade watch owing to lies in May, Treasurer Scott Morrison has doubled down in his MYEFO. He has downgraded the Budget outlook by $10.3bn over four years:

But is still projecting a surplus in 2021:

Even though has absolutely no way to get us there.

Except lying of course, and here the untruths:

Here is my table of before and afters for this year, which doesn’t matter too much:

| Budget | Actual | MYEFO | |

| GDP | 2.5 | 1.8 | 2.75 |

| Household consumption | 3 | 2.5 | 3 |

| Dwelling investment | 2 | 7.2 | 4.5 |

| Business investment | -5 | -8.5 | -6 |

| Private demand | 1.5 | 1.5 | 1 |

| Public demand | 2.25 | 4.8 | 3 |

| Net exports | 0.75 | -0.2 | 0.75 |

| Nominal growth | 4.25 | 3 | 5.75 |

| CPI | 2 | 1.3 | 1.75 |

| Wage price index | 2.5 | 1.9 | 2.25 |

| Unemployment rate | 5.5 | 5.6 | 5.5 |

| Terms of trade | 1.25 | 15 | 14 |

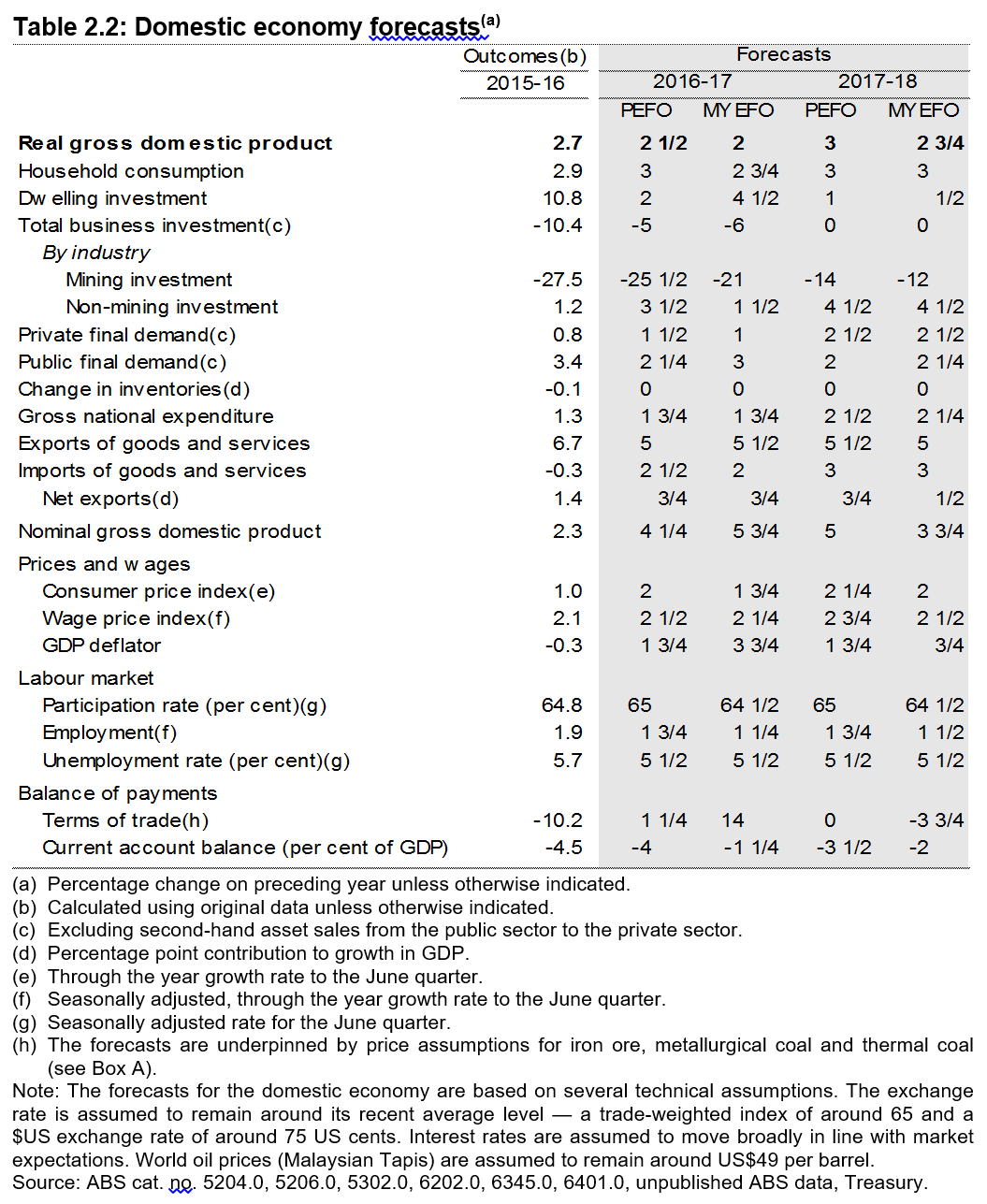

And more to the point for 2017/18:

| Budget | MYEFO | MB | |

| GDP | 3 | 2.75 | 1.5 |

| Household consumption | 3 | 3 | 2 |

| Dwelling investment | 1 | 1 | -5 |

| Business investment | 0 | 0 | -2 |

| Private demand | 2.5 | 2.5 | 1.5 |

| Public demand | 2 | 2.5 | 5 |

| Net exports | 0.75 | 0.5 | 0.75 |

| Nominal growth | 5 | 3.75 | 2.5 |

| CPI | 2.25 | 2 | 1.5 |

| Wage price index | 2.75 | 2.5 | 1.8 |

| Unemployment rate | 5.25 | 5.5 | 6 |

| Terms of trade | 0 | -3.5 | -14 |

The two major divergences from realty is the terms of trade, and thus, nominal growth and income. On the terms of trade, commodity prices are sensibly projected to retrace but too slowly:

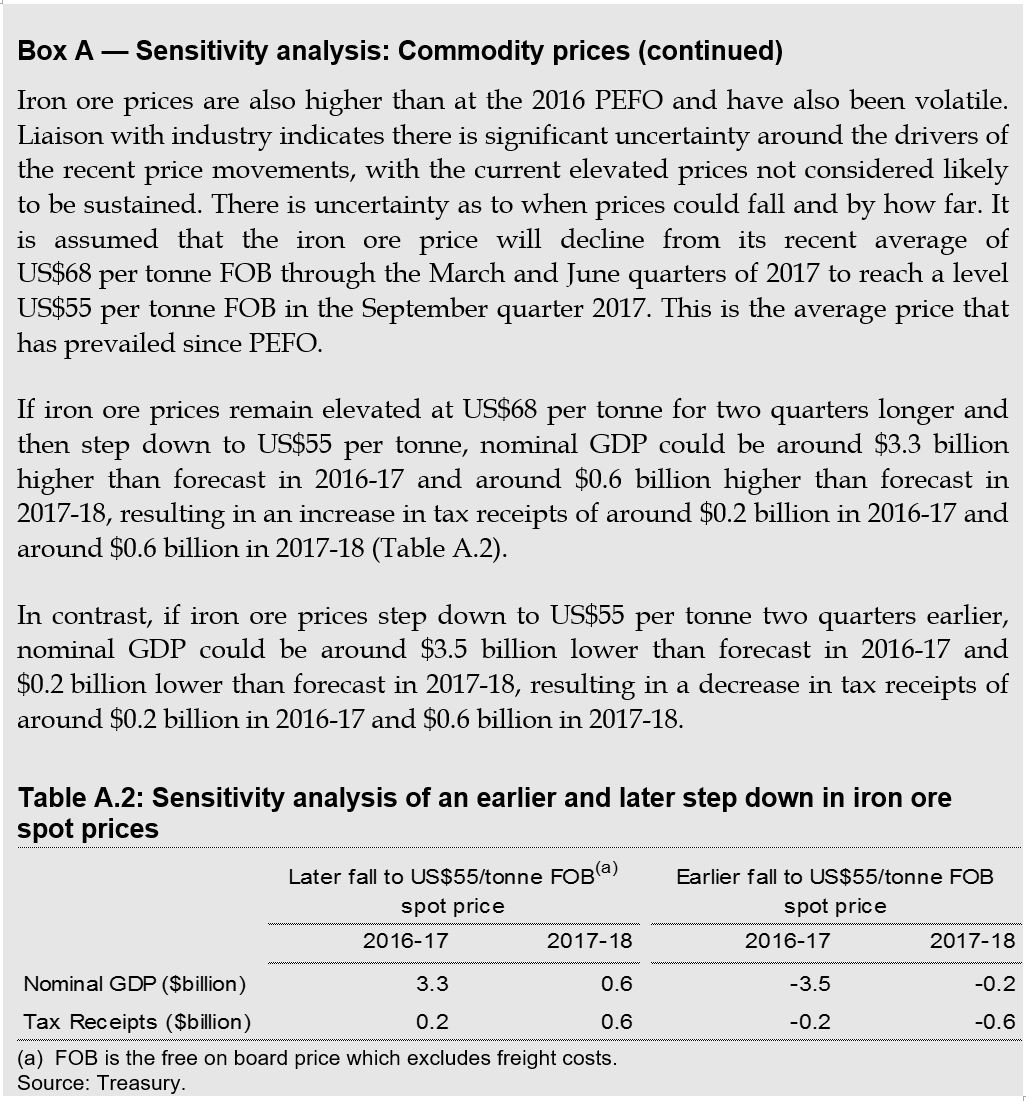

My outlook is for spot coking coal at $120 by Q3 and contract for Q4 2017 and for iron ore at $50 by mid-year but averaging $45 through 2017/18 versus Downgrade Morrison’s $61-62.

How is income going to suddenly bounce with falling terms of trade, a stalled labour market and lousy productivity growth? Answer: it’s not.

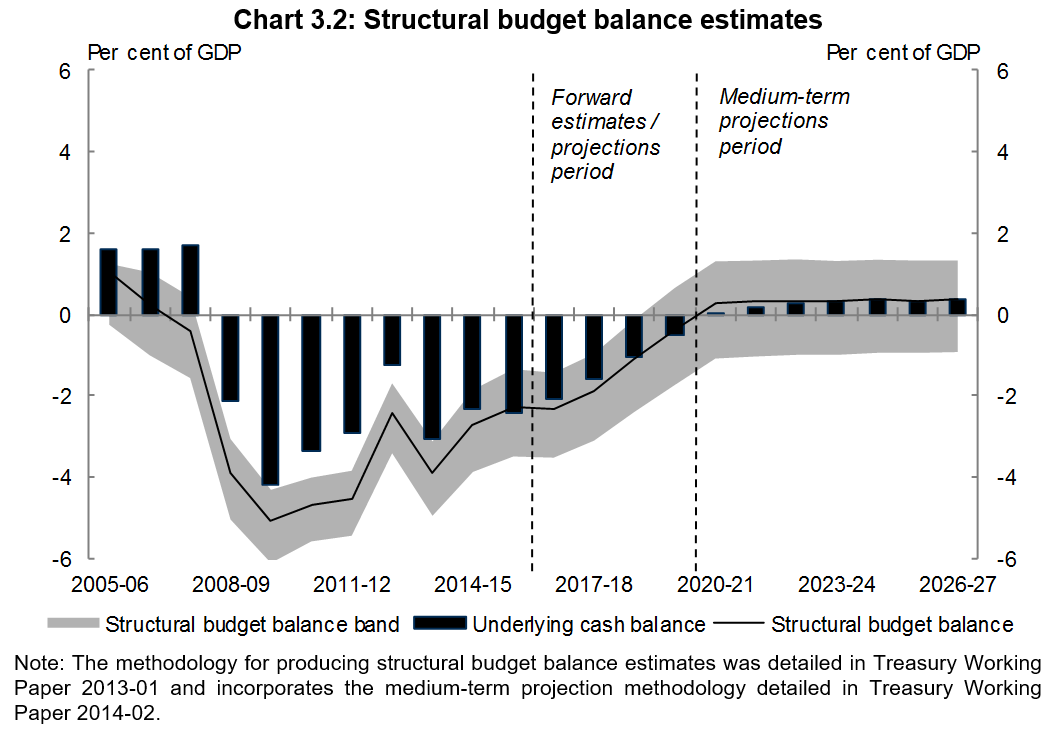

But the booked 2017/18 uplift pales in comparison to the boom that’s coming in 2018-2021:

Despite a still falling terms of trade, a collapsing dwelling boom, ongoing mining capex cliff and shuttering car industry, nominal growth and wages are going to roar back and rescue the Budget eighteen months out. I might add that mid-4% for nominal growth is the average since 1991 which contained three booms, first productivity, then housing, then mining. Where’s the next boom coming from?

If only lies added to GDP then we’d have a shot at it.

So, will we be downgraded? Should be. This is just more lies from a serial liar.