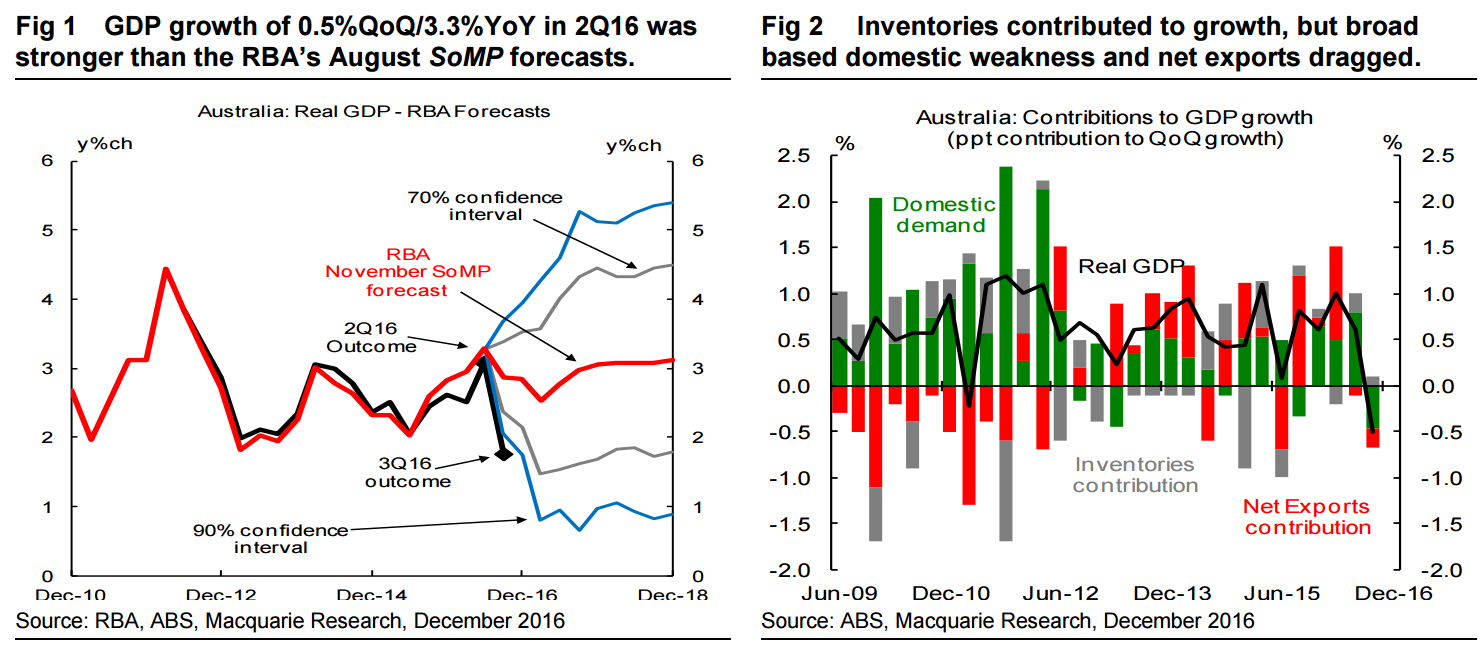

The 3Q GDP outcome will come as a shock. A casual contentedness around Australia’s economic performance had grown since the 3.3%YoY outcome reported in 2Q16. The outcome is a catalyst for expectations around policy to shift over coming weeks.

The A$ is too strong for the economy We don’t think the weak GDP outcome should be a shock, and have long been arguing that the exchange rate was too high for the economy’s transition. Continued import strength, and signs that the traded services sector’s contribution to growth is reversing, are clear evidence of this dynamic.

Although the currency has come a long way down from parity, on a tradeweighted basis it has not yet come far enough to rotate sufficient demand into the economy to balance the labour market and stoke a non-mining business investment recovery. Particularly whilst the economy continues to endure a fiscal consolidation. Firm commodity prices may hamper the currency’s decline, creating friction for policymakers.

Weak economy a wake-up for policy The GDP outcome will cause a reassessment of policy prospects. The consensus on either monetary or fiscal policy, or both, needs to shift. Whilst there is a swing to fiscal policy emerging globally, Australia is lagging on this front, with a focus on budget repair in acquiescence to ratings considerations taking primacy over the need for demand support within the economy.

The argument for fiscal consolidation of ~1/2ppt of GDP makes sense if the economy is growing at or above trend. But as it is now likely to be some time before the economy’s growth pulse recovers to trend-type growth rates, some reassessment of the fiscal stance will be needed. The GDP outcome reinforces the existence of a large output gap that underemployment trends within the labour market were already indicating. That gap needs to close to avert further internal disinflation. The MYEFO due in coming weeks is too soon to shift in response, and it’s a long time before the May Budget.

Fiscal absence places the burden on rates The longer fiscal policy continues to exert a contractionary impact on a weak domestic economy the more work will be required of monetary policy. We think that the economy’s broader policy settings, and the GDP outcome mean a rate cut in February (our base case) is now much more likely. The 3Q16 GDP outcome is a major miss (1.8%YoY vs 2.9%YoY) compared to the RBA’s November forecast. An outcome this weak is below the 90% confidence range of the RBA’s forecast ‘fan charts’. There’s always a wide range of uncertainty around the economy’s performance, and then there’s this.

Is it temporary? One key question from the sharp plunge to a sub-2% GDP growth rate is how much of the GDP outcome is a one-off? Certainly, some aspects of the public demand weakness will normalise, as state infrastructure programs continue to progress. Non-residential construction outside of the mining sector should improve in 4Q and beyond given the approvals track and weather impacts in 3Q. Resource export volumes should improve as production comes online. But the enduring strength of the A$, on a broader TWI basis and particularly against key importers like China, suggests to us a reasonable chance that import competing sectors may struggle. Some rebound is likely, but the strength of the bounce may disappoint.

Is the economy on track for a recession? No, we don’t think so. As we highlighted recently the economy is just four quarters away from taking the record for the longest economic expansion. The underlying population data within the GDP figures point to a continued pick-up in population growth. Firm commodity prices suggest the resource export volume picture remains intact. These two growth supports alone should drive growth of ~2.5%pa, and make it quite difficult for the economy to experience 2 consecutive quarters of contraction.

But weak internal demand growth amidst strong population supply means the continuation of weak internal inflation pressures will remain a feature of the economy’s outlook for some time. For the equity market the outcome may not be as negative as it is from a policy perspective. The stronger terms of trade supported nominal GDP, which rose 0.5%QoQ, to be 3.0%YoY. Rising mining profits were a key driver of the nominal outcome, despite the softening in resource export volumes and mining production. Price rises are coming through as capex is declining.

Will the terms of trade help, or hurt? The key question around the terms of trade boost for the broader economy over 2017 is whether the rise in the terms of trade, and associated currency strength, spills over into the broader domestic conditions. As we highlighted in our 2017 outlook a number of the links in the transmission chain (especially the fiscal channel) are expected to respond differently to the recent (mid-2000s) experience. We think the economy will experience a degree of hangover into 1H17 from the strong A$, before the recovery in non-mining investment and public infrastructure broadens and gathers momentum from 2H17 onwards.

Quite right on all but one point. This notion that “recovery in non-mining investment and public infrastructure broadens and gathers momentum from 2H17 onwards” is wrong. H2 2017 will begin the capex cliff 2.0 as the dwelling construction boom goes bust. Non-mining investment is not going to rebound then it’s going to get worse.

The RBA is going to zero, or as close to it as it can without triggering a financial crisis, and it’s still not going to matter.

The only thing that can fix this economy is a very extended period of dollar weakness below 50 cents.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.