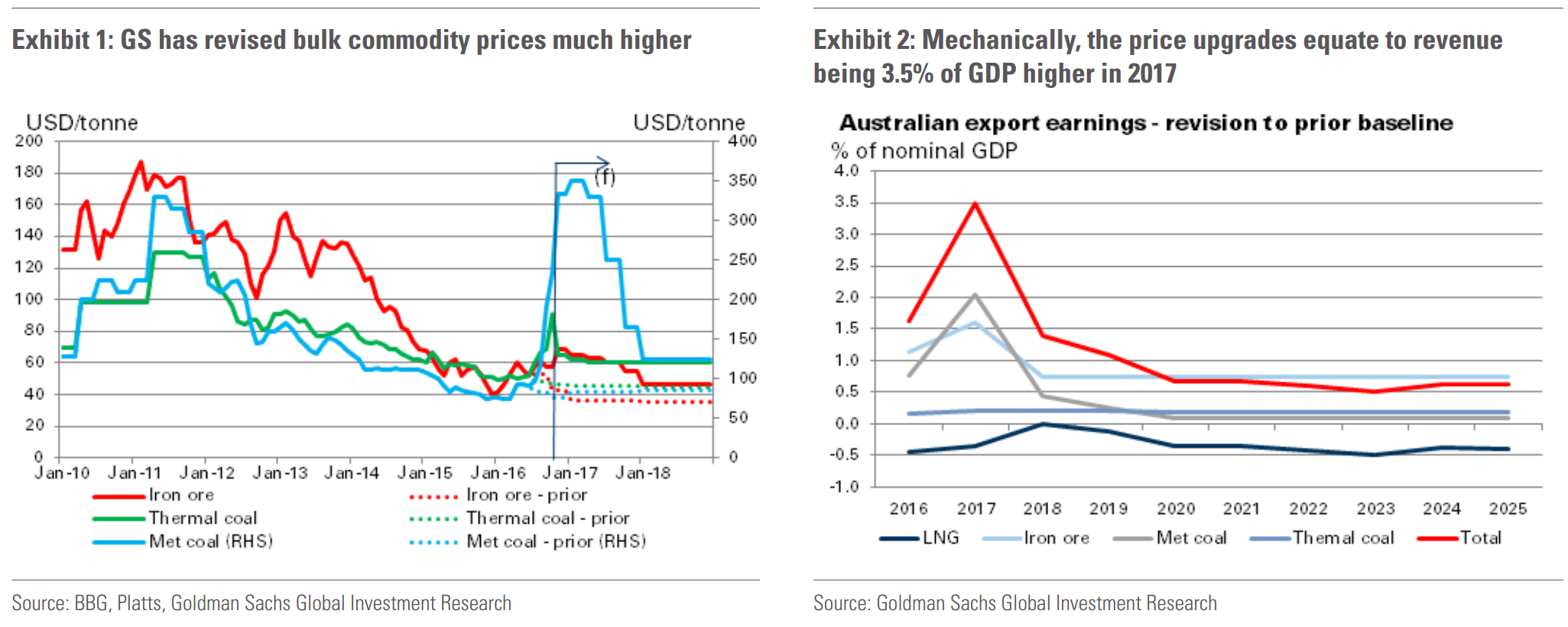

Following on from the material contraction in GDP reported for the September quarter, Monday’s mid-year economic and fiscal outlook incorporated news of a further deterioration in Australia’s public finances. Against this negative backdrop, it is not surprising that surveyed sentiment has been under some pressure recently. However, consistent with increasingly upbeat rhetoric from the RBA, we caution against getting too negative on Australia’s outlook. Looking ahead, alongside a far more supportive global backdrop, Australia is now on course to receive a very significant positive income shock from higher commodity prices, in our view.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.