First it was the Business Council of Australia and the Turnbull Government calling for a 5% cut to company taxes at a huge cost to the Budget.

Today, we have KPMG’s partner Grant Wardell-Johnson and HSBC’s Paul Bloxham urging Australia to slash to top marginal tax rate to New Zealand’s level of 33% in a bid to raise workforce participation and fire-up economic growth. From The AFR:

Cutting the top marginal tax rate would encourage labour participation and help return the budget surplus, economists argue.

Writing in The Australian Financial Review, KPMG partner Grant Wardell-Johnson said lowering the top marginal tax rate from 49 per cent to the New Zealand level of 33 per cent could encourage labour participation, particularly among women.

“While many assert that participation rates are relatively insensitive to marginal rates for many groups of men, this is not true for some men and most women,” Mr Wardell-Johnson said…

HSBC chief economist Paul Bloxham said adopting a NZ-style tax reform would help the budget bottom line because it would boost the revenue through economic growth and cut the spending on welfare.

“If you shift the tax base away from income tax towards consumption tax, it gives you more incentive to work,” he said.

“Because [the tax system is] not indexed and because income has been gradually rising, we’ve got an increasing proportion of the population moving into the higher tax brackets, discouraging labour market participation…”

I do have some sympathy with this view. Without reform, Australia’s tax system will become increasingly reliant on personal income taxes via bracket creep, which are also highly regressive in addition to being inefficient.

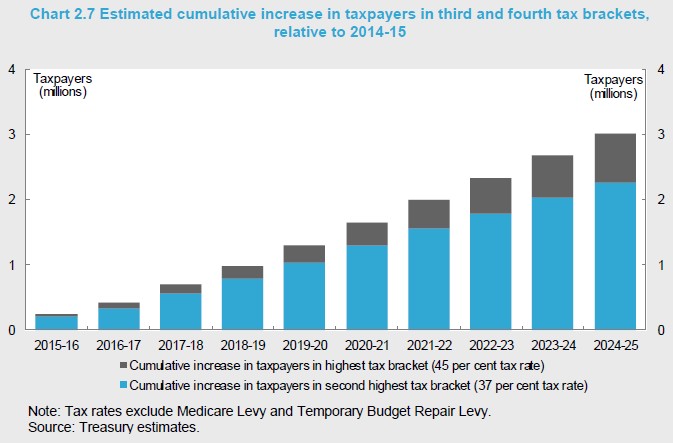

Indeed, the Australian Treasury’s Tax Discussion Paper , released last year, forecast that Australia’s reliance on inefficient personal income taxes would rise inexorably over the next decade (to 56% of taxes by 2024-25), making reform an imperative as the population ages and the share of workers across the economy declines:

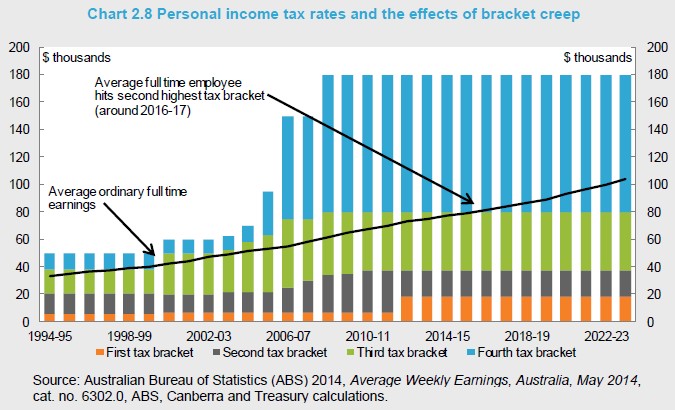

Treasury also noted that this bracket creep is highly regressive and inefficient:

…average ordinary full-time earnings were around $75,000 in 2013-14, and are expected to be around $104,000 in 2023-24 (see Chart 2.8). Someone on average full-time earnings therefore had an average tax rate of 22.7 per cent in 2013-14, increasing to 27.4 per cent by 2023-24. By contrast, someone with only half that income earned $37,500 in 2013-14, increasing to $52,000 in 2023-24. However, their average tax rate will increase from 10.3 per cent to 17.8 per cent. Someone earning twice the average full-time wage is on $150,000, increasing to $208,000 in 2023-24, but their average tax rate will only increase from 30.5 per cent to 34.3 per cent.

For some people, particularly those on relatively low incomes, bracket creep can reduce incentives to work. At higher incomes, bracket creep increases the incentives for tax planning and structuring, and even overseas relocation. Bracket creep is therefore not just an issue because of its effect on progressivity, but because over time it exacerbates the other problems in the individuals income tax system.

Wages growth has been lower than initially projected, so any bracket creep will likely be slower than anticipated above. But the central points still remain.

That said, the second highest tax threshold has already been raised from $80,000 to $87,000 by the Turnbull Government, and there is little evidence to suggest that slashing the top rate to 33% would do much to boost participation and growth.

First, the government will have to make-up the lost revenue in other ways, such as cutting expenditure on public services or raising taxes elsewhere. Hence, it will give with one hand and take with the other, thus mitigating any positive impacts on growth.

Higher income people also have a higher ‘marginal propensity to save’ (MPS). That is, they are more likely to save some of that tax cut than poorer people. Hence, it could actually lower growth compared to the government spending the money on services or infrastructure, or giving a tax cut to those on lower incomes, who have a lower MPS.

Second, just because you have lowered tax rates at the upper end doesn’t mean they will work more. These higher income earners are just as likely to choose to work less, play golf, and receive the same take-home pay. So the impacts on labour participation are ambiguous.

Third, there are the equity issues. Giving the highest income earners a large tax cut would undoubtedly worsen inequality.

If the goal of tax cuts is to boost aggregate demand, growth and jobs, then it would seem better to fix-up incentives at the lower end of the tax scale to encourage would-be second income earners to move into the workforce, thus boosting labour participation. It would also be more equitable.

In any event, these piecemeal calls for tax reforms – be it cutting the company tax rate or lowering the top personal tax rate – are not what Australia needs. What we need is a comprehensive tax reform package that broadens the base and shifts the tax burden away from productive effort.

These should include a combination of income tax cuts, welfare increases, broad-based land taxes, consumption taxes, unwinding inefficient and inequitable tax concessions, and possibly even company tax cuts. The important thing is that the package is comprehensive so that the overall tax base is broadened and built around more efficient and equitable sources.

Unfortunately, Labor had a golden opportunity when it was in Government upon the release of the Henry Tax Review, but blew it. And this Government has done the same thing by abandoning its Tax White Paper process and throwing its support behind a narrow cut to company taxes.

Such is the dysfunctional and stillborn nature of Australian politics, whereby neither side has been capable of crafting a comprehensive tax reform package that carefully balances efficiency with equity.