As summarised earlier, the Australian Bureau of Statistics (ABS) has today released its labour force report for October, which registered a 9,800 rise in total employment but a stable headline unemployment rate 0f 5.6%.

The result missed analysts’ expectations of 16,000 jobs growth.

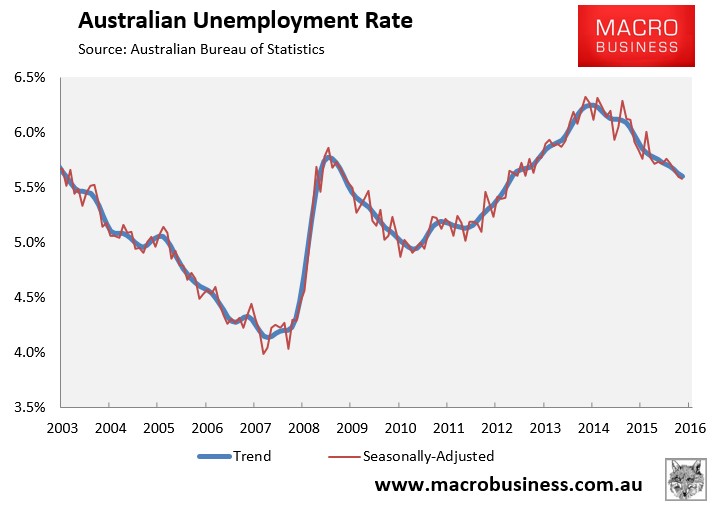

In trend terms, the unemployment rate fell from 5.63% to 5.60%:

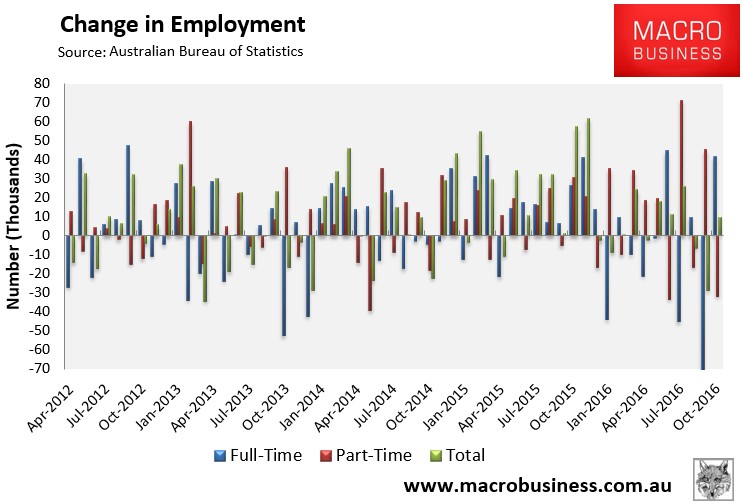

Again, total employment rose a seasonally adjusted 9,800 to 11,938,900. Full-time jobs jumped by 41,500 more than offsetting a 31,700 rise in part-time jobs:

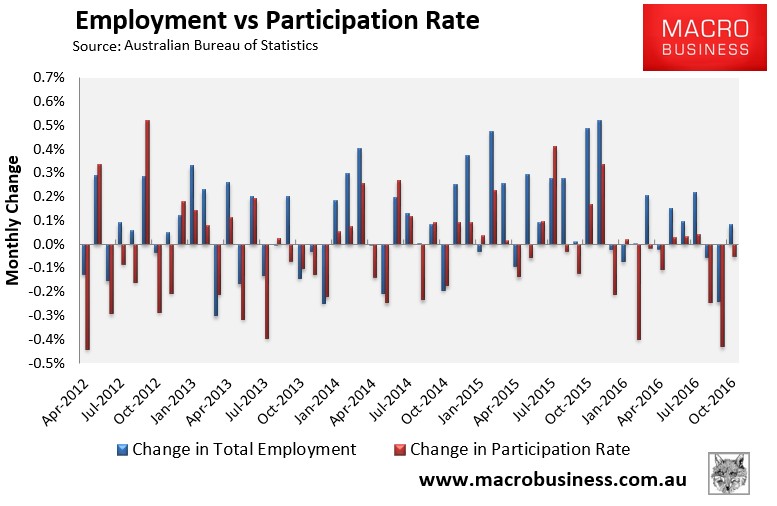

The participation rate fell ever so slightly to 64.4% over the month:

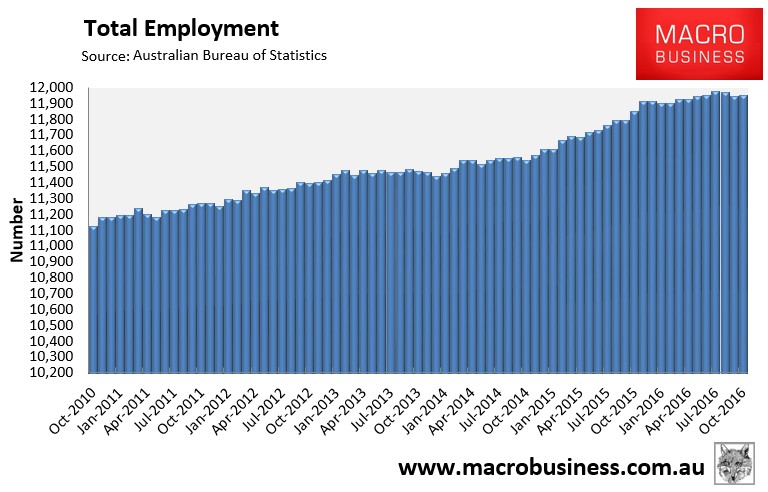

The trend in total employment continues to flatline after last October’s and November’s numberwang surge:

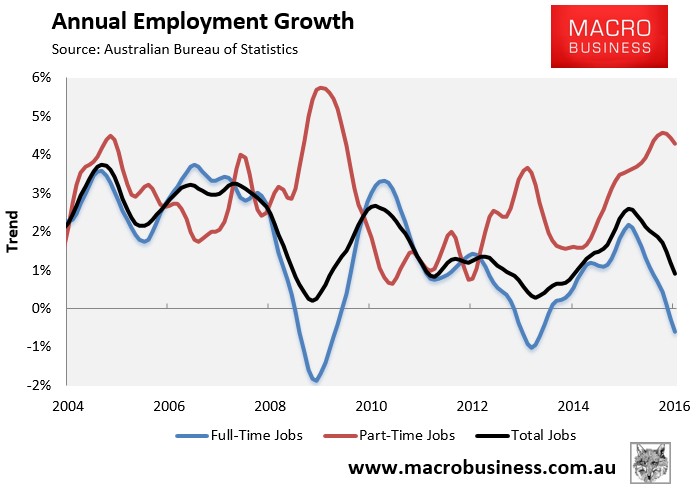

And because last October’s surge has rolled-off, trend annual employment growth continues to weaken and is being driven exclusively by part-time employment, with full-time jobs contracting:

As shown above, trend full-time jobs growth has turned negative at -0.6% versus 4.3% growth for part-time jobs.

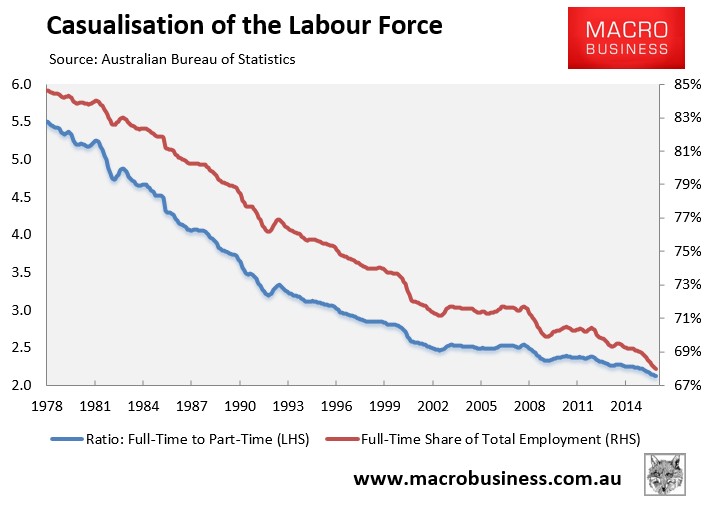

The proportion of the population in full-time work has also hit a fresh record low:

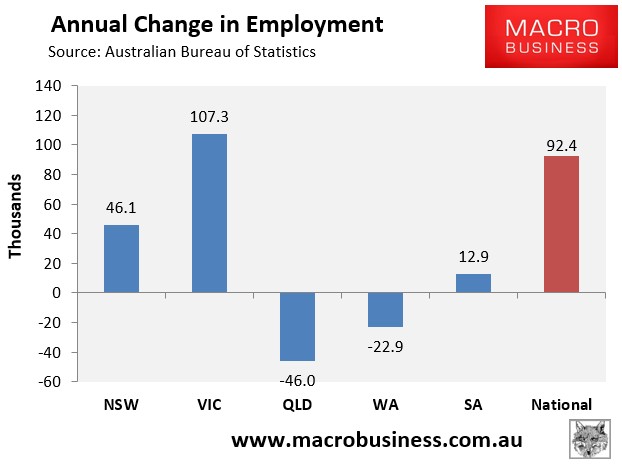

The housing bubble epicentres of New South Wales (Sydney) and Victoria (Melbourne) continue to drive all of the jobs growth over the past year, accounting for 50% and 116% respectively of national jobs growth in seasonally adjusted terms:

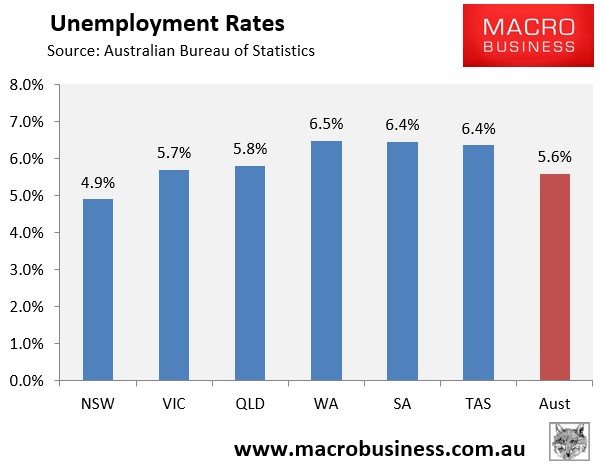

In a reversal of fortunes from the mining boom days, Western Australia now has the highest seasonally adjusted unemployment, whereas the bubble epicentres of New South Wales and Victoria have the lowest (see next chart).

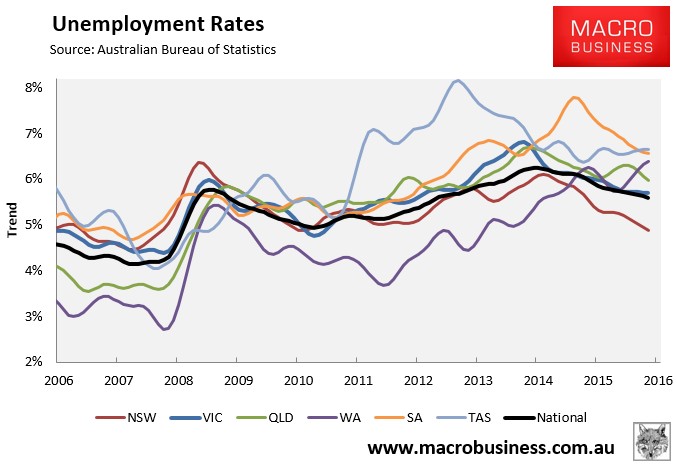

The state seasonally-adjusted figures are notoriously volatile and subject to a big margin of error. As such, the below chart shows the ABS’ trend unemployment rates, which again shows the bubble epicentre of New South Wales with by far the lowest unemployment, South Australia and Tasmania with the highest with Western Australia catching-up fast, whereas Victoria has average unemployment and Queensland has above-average unemployment:

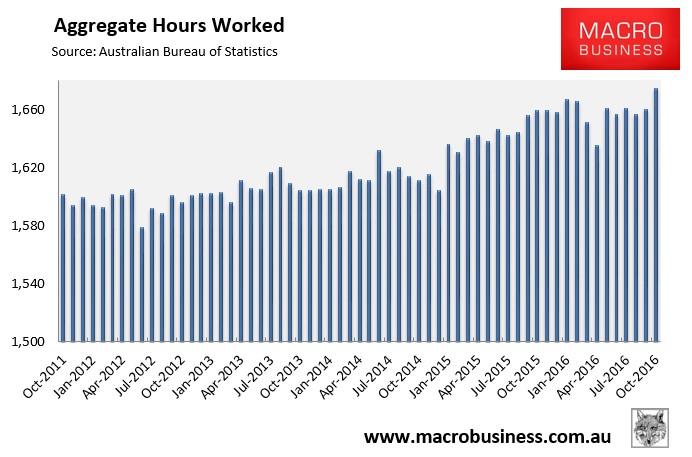

The aggregate number of hours jumped in seasonally adjusted terms, rising by 14.3 million hours or 0.86% in October. However, hours worked have risen by just 0.9% over the past year:

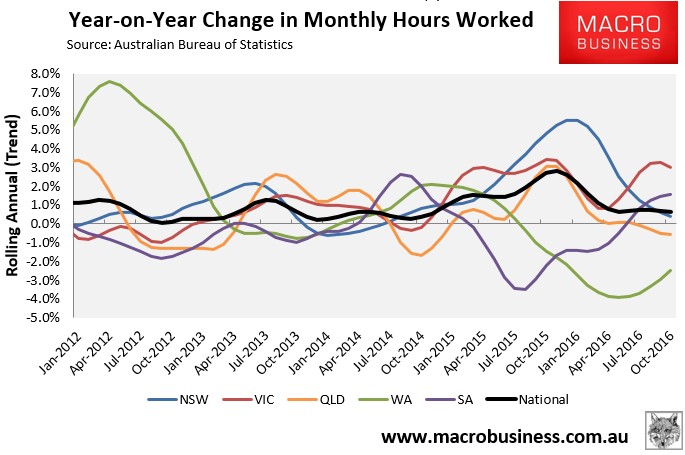

The below chart, which tracks the annual change in hours worked on a trend basis, paints a sobering picture. It shows that Victoria (Melbourne) has driven the lion’s share of growth in hours worked, with most other jurisdictions showing minimal or negative growth. Nationally, trend growth in hours worked was just 0.6% in the year to October and continues to fall gradually:

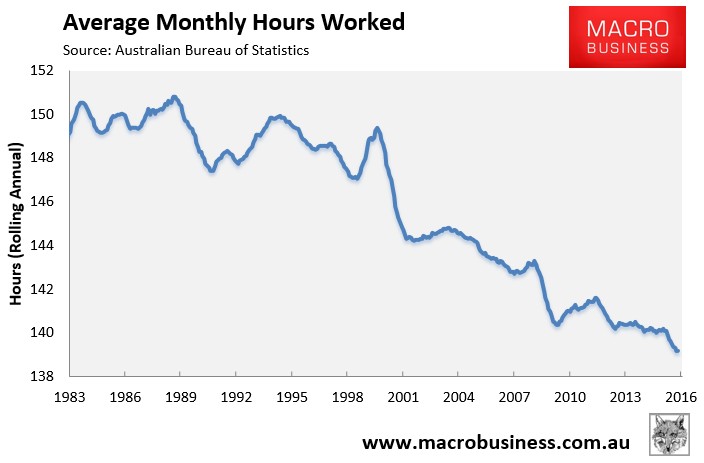

Average hours worked is also at a record low:

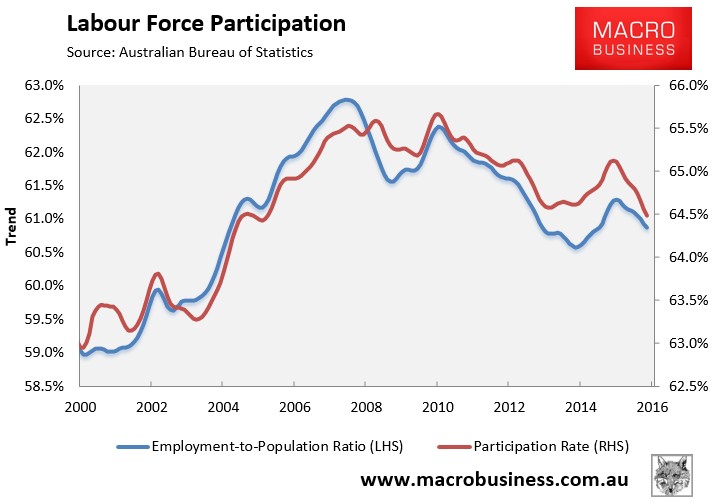

And workforce participation is weakening:

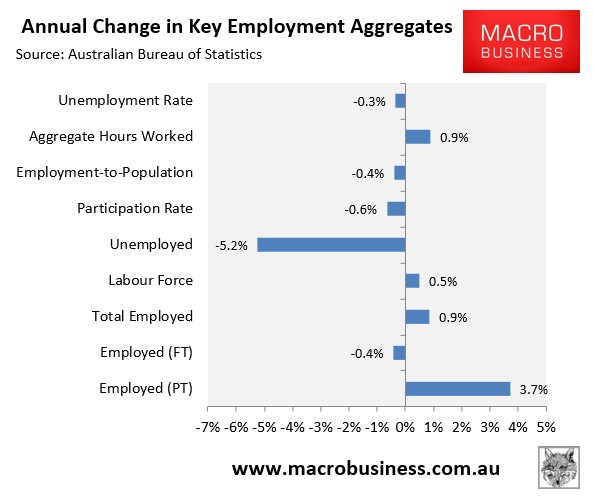

To round things out, the next chart summarises the annual change in the key employment aggregates on a seasonally-adjusted basis, which shows a mostly negative picture:

Despite this month’s seasonally adjusted bounce in full-time jobs and hours worked, the labour market remains precarious.

Virtually all of the jobs growth is coming from the two ponzi markets of New South Wales (Sydney) and Victoria (Melbourne). Trend growth in full-time jobs is negative. Trend growth in hours worked is weak. And labour force participation is falling.

Annual employment growth is also set to take another hammering next month when last November’s surge rolls-off.

When the dwelling construction boom eventually rolls over, along with the closure of the car industry, the employment picture will obviously weaken further. What can realistically rise up to fill the void?