From the ABC:

Having just spent $200 billion over the best part of a decade to become the world’s biggest exporter of LNG, Australia is now looking down the barrel of having to import gas for domestic users.

In a 21st century variant of “selling coals to Newcastle”, energy supplier AGL has flagged it may need to spend up to $300 million to build an LNG import depot to shield itself from soaring gas prices and increasing difficulty in finding reliable local supplies.

While the original idiom of shipping coal to the coal-mining heartland in England’s industrial north was the very essence of pointless and wasteful economic activity, AGL may well have little alternative.

While far from a done deal, AGL executives unveiled the idea at its recent investor day briefing as a plank in the next stage of $700 million worth of “growth initiatives”, with $17 million already set aside for a feasibility study over the next two years.

There’s a reasonable chance AGL may well find it is cheaper to import gas from any number of low-cost producers in the Middle East, Asia or the US rather than tap into supplies under its feet.

AGL, who along with Origin Energy supplies around three-quarters of domestic east-coast gas, has looked ahead and is more than a bit worried.

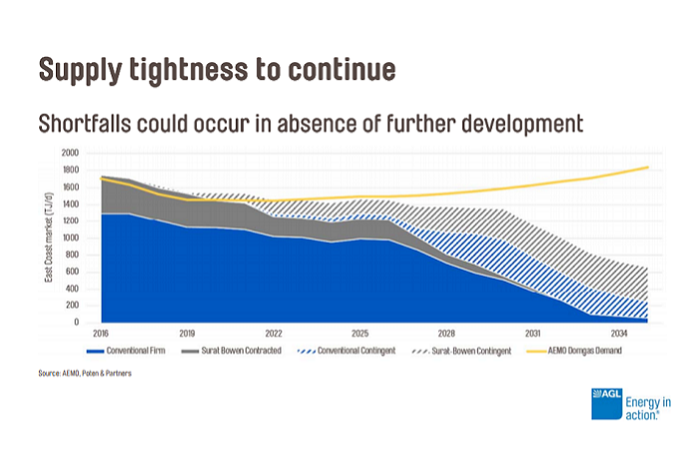

Future cheap gas supplies locked up for exports

AGL’s contracted gas supplies start declining next year, a trend that accelerates through to 2020 when its key deal with the Gippsland Basin joint venture partners ExxonMobil and BHP expires.

Without development of new gas fields, the domestic situation will move from merely tight to shortfall from around 2020 onwards.

There is a lot of gas out there, but the cheap gas is largely dedicated to the export market out of Gladstone and locked up in long-term contracts.

The Australian Energy Market Operator forecasts by 2018, 70 per cent of gas demand will be Queensland LNG exports, with domestic and industrial users a bit under 10 per cent each, and a shrinking slice set aside for power generation.

Remove the cheap gas from the equation and what is left is expensive gas.

Gas imports would create competitive tension for domestic contracts

So what is the break even point where it is cheaper to import LNG than use what is already here?

UBS analyst Nik Burns has crunched the numbers and suspects it is around $11 per gigajoule (GJ).

Currently AGL is said to be paying the Gippsland JV around $7.50/GJ but the asking price is expected to be well above $10/GJ come the next round of contract negotiations.

“Not only would this LNG price be at (oil-linked) LNG netback prices, but would also require the addition of around $2/GJ for gas transportation to NSW and more if to Victoria.”

If the oil price continues to recover, export prices for Queensland gas could be well north of $13/GJ down the track, so it looks an unlikely source for AGL in the current regime.

Mr Burns said the price of LNG imports depended on a number of variables, but the outcome would not be cheap.

Factoring in a US-based Henry Hub price of around $US3.20/GJ and the various liquefaction, shipping and re-gassing charges, Mr Burns said LNG could be landed in New South Wales or Victoria at $10.50/GJ.

“The logical outcome would be to renegotiate the Gippsland Basin contract, but AGL needs to create some competitive tension,” Mr Burns said.

Floating import terminals are cheaper options

The betting is rather than building a plant onshore, AGL would employ a floating storage and regasification unit (FSRU), similar to one used by Hawaii Gas, which has an infrastructure cost of around $US200 million ($270 million).

AGL didn’t flood the investor presentation with details about its import plans beside saying a number of potential sites had been identified and regulatory and community consultations would start early next year.

A terminal could be operational by 2022.

Macquarie’s utility team has also had a look at the numbers and found there is “some attraction” for AGL in importing gas.

“The (FSRU) infrastructure cost over ten years, assuming the facility was used at 75 per cent of capacity, is around $0.20/GJ.

Combined with the cost of rental and conversion, the cost of a re-gas facility is around $0.75/GJ,” Macquarie said in a recent research note.

“Such a cost is materially cheaper than the cost of shipping gas from Wallumbilla to Victoria or NSW at around $2/GJ.”

Wallumbilla is the major transit point between Queensland and east coast gas markets – including export terminals – and provides a centralised distribution and trading hub, including the benchmark futures platform used in domestic pricing.

Deutsche Bank’s utilities and energy analyst John Hirjee said New South Wales would be the most likely place to moor a floating terminal given it represents a large market for AGL and there is limited domestic gas production in the state.

“At this point, we believe this could be an attempt to generate a Government response to increase the availability of onshore gas acreage for development -such as New South Wales CSG.”

At the moment, getting a NSW government to back coal seam gas again seems more far-fetched than importing gas into a gas rich country.

Gas consumers will be paying more

With or without gas imports, domestic gas users will pay more.

Wholesale prices are looking like being more than double where they were 3 or 4 years ago.

So while households won’t necessarily feel all that pain, big industrial users paying very close to AGL’s wholesale price are likely to be paying around 100 per cent more for gas.

The gas issue is becoming a political imperative with industrial lobby groups talking about more factory closures and big users such as the fertiliser and explosives maker Incitec Pivot shifting operations to the low-cost energy environment of Louisiana in the US.

On top of that, ACCC chief Rod Sims is demanding the regulatory rulebook for the gas industry be rewritten, while taking the pressure off domestic users is a key agenda item at the Council of Australian Government meeting next month.

The potential embarrassment of the world’s biggest gas exporter having to import gas may be just the incentive politicians need to get consumers a better deal on soaring energy prices.

The response from gas suppliers will be interesting too as it is hardly in their interests to open up the domestic market to cheaper international imports.

As for the “coals to Newcastle” analogy, it could be pointed out that the Port of Tyne had been receiving coal since the 1990’s but ceased this year as coal-fired power stations and steelmakers in the UK continue to shut up shop and more renewable energy is brought on line.

This last point is one key. A dumb or corrupt Federal Government appears intent on making gas power the marginal price setter for eastern electricity markets by looking at it as some kind of capacity backstop for base load power increasingly taken up by renewables. That will only exacerbate the gas shortage and, because gas sets the marginal price of east coast electricity, drive prices wild.

In that event gas imports will be viable and they may not be quite as expensive as they appear. The Asian market for LNG is still largely based upon contracts that inhibit any change in destination for gas shipments. This is to prevent, say, Japanese bought gas from Curtis Island from being resold to someone else looking for quick supply. It’s a way of ensuring that producers control supply and prices. But Japan is currently in the process of investigating the legality of these clauses. Europe long ago declared them illegal and Japan is almost certainly going to do the same.

This opens up the possibility of AGL buying gas from Curtis Island via one its Asian customers. The price then would be the oil-linkage plus a trading margin and shipping. Even in the long term I don’t think oil is going to get much above $50, and I expect contract margins to get squeezed by the glut as well. So Japan could be buying USD6mmBtu LNG from Curtis Island then on-selling it to AGL at AUD10 delivered.

Needless to say, this is pretty perverse stuff even if it might help cap the gouging of the east coast cartel. It might even result in them being forced to drop prices now to prevent it so it’s not a bad idea for AGL to pursue this line in inquiry.

But, there really is a much simpler answer. It’s two words: domestic reservation.

Policy could simply be shifted so that the gas cartel is forced to sell a certain volume of its gas locally. If it doesn’t then it loses the gas. It’s really just price regulating what is now an effective gas monopoly.

The Australian public and its gas-consuming businesses did not create or sign-off on the mad gas bubble in QLD that led us to this impasse, so they most certainly should not have to pay for it. If the gas cartel buggered up its own investments by misunderstanding that the political economy would not stand for being gouged like it is right now then that is its problem.

Reserve the gas now. If there’s not enough for delivery of export contracts then good. It’ll help mitigate the global glut and support offshore prices so that Asian households pay for the gas not Australian.

If it results in write downs or bankruptcy in producers then too bad. Gas producers dug this hole and they can lie in it.