The Italexit shock looms, via Reuters (chart from Bloomie):

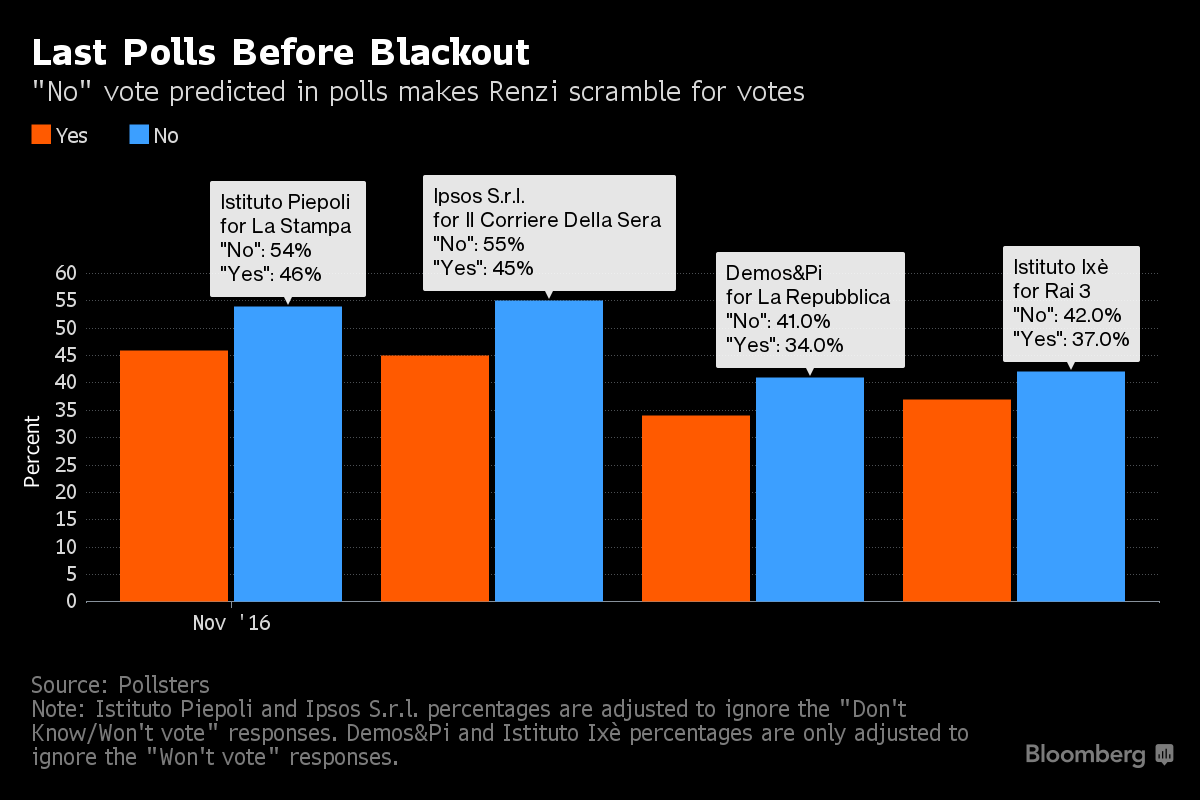

Italian Prime Minister Matteo Renzi’s hopes of winning his referendum on constitutional reform are dwindling fast as previously undecided voters are choosing to oppose his plan, according to pollsters.

Renzi has promised to resign if he loses the Dec. 4 ballot over his proposal to reduce the role of the Senate and transfer powers to central government from the regions, increasing political uncertainty in the euro zone’s third largest economy.

The heads of several polling agencies contacted by Reuters said Donald Trump’s surprise victory in the U.S. presidential election last week — based on a wave of anti-establishment sentiment — seemed to be a factor behind a widening lead for the ‘No’ camp.

Others had additional explanations, but all agreed that sentiment was hardening against Renzi, giving him a very tough task to turn around the polls in the next two weeks.

“There’s a clear acceleration for ‘No’ and the Trump factor seems to have tipped the balance among many who were undecided,” said Roberto Weber, head of the Ixe agency.

Of 42 polls by 15 different agencies since Oct. 21, every one has the ‘No’ camp ahead. And the margin is growing.

“Trump’s victory was important because Renzi strongly backed Hillary Clinton and so people link him with the loser and the mainstream establishment that Clinton was seen as representing,” said Alessandra Ghisleri, head of the Euromedia agency.

Ghisleri’s latest poll gives ‘No’ a lead of eight percentage points, widening from four points just 10 days ago.

The fallout in Europe from the election of Donald Trump is perhaps nowhere as stark as in France. A country that has the largest far-right party on the continent is fast heading towards key elections. Marine Le Pen, leader of the Front National, has felt elated by the US vote, just as she was by the Brexit referendum. On 9 November she applauded “not the end of the world but the end of a world”. She hopes to replicate in France what Trump has achieved in the US. Whether Ms Le Pen can attain her goal is by no means a certainty. In France’s two-stage electoral system, to win the presidency a candidate needs to come top or second in the first round of voting and then win the run-off between both finalists. Ms Le Pen is all but guaranteed to pass the first hurdle, with polls putting her support at around 30%, but will struggle in the second. But Ms Le Pen in the Elysée Palace is no longer a far-fetched idea. France stands at a dangerous crossroads. Who her opponent might be becomes a matter of not just European, but global import.

The chances of the left are dismal. It is increasingly divided and the Socialist president, François Hollande, has approval ratings of just 4%. The announcement this week that Emmanuel Macron, his former economics minister, will run for the presidency has added another blow. Macron’s youthful “moderniser” image carries some appeal, but he lacks the backing of a party structure and his programme is as yet unknown. So the main contest is being waged within France’s mainstream right, which will start holding its primaries on Sunday. If none of the seven candidates reaches 50% in this first round – which is likely – a run-off between two finalists will be held on 27 November. The main contenders are the former prime minister Alain Juppé and the former president Nicolas Sarkozy. Another name, recently gaining ground, is François Fillon, a former prime minister under Mr Sarkozy for five years and a firm conservative. This cast of politicians, whose careers stretch over decades, speaks little of democratic renewal. Yet the contrasts between them are significant.

Mr Sarkozy has opted to echo some of Ms Le Pen’s xenophobic themes, especially on Islam and immigration. Mr Juppé has chosen, by contrast, to combat them, convinced that pandering to FN voters will only galvanise Ms Le Pen, not counter her. He believes a message of moderation and inclusiveness is what the country needs, at a time of crisis and trauma resulting from terrorist attacks and rising social ills. He is also wants to shake up economics, wanting to loosen up the labour market to tackle unemployment. Mr Sarkozy hopes a Trump-type contagion in France can benefit him – but Mr Juppé has the edge in polls.

Front National leader Marine Le Pen has taken a sizeable lead over Nicolas Sarkozy in a new French presidential election poll.

The far-right leader had 29 per cent of the vote when pitted against Les Républicains’ former president, who was eight points behind, and held a 15-point lead over the Parti de Gauche’sJean-Luc Mélenchon in the poll released by Ipsos.

It was one of five scenarios for the first round of France’s 2017 presidential elections on 23 April, although one that did not include Les Républicains’ Alain Juppé – who remains strong favourite to succeed Francois Hollande as leader.

While Mr Juppé holds leads of between 4 and 7 per cent in three other scenarios including him, the results are likely to add to growing fears that the rise of global populism could see Ms Le Pen secure a surprise victory in the wake of the UK’s Brexit vote and Donald Trump’s US election win.

The referendum matters as it could accelerate the path towards euro exit. If Mr Renzi loses, he has said he would resign, leading to political chaos. Investors might conclude the game is up. On December 5, Europe could wake up to an immediate threat of disintegration.

In France, the probability of a presidential election victory by Marine Le Pen is no longer a remote risk. Of all the candidates that have declared, she is the best prepared. There are some who could beat her, like Emmanuel Macron, the former reformist economics minister, who declared his candidacy on Wednesday. But he may not make it to the final round of the elections as he lacks a party apparatus. If Ms Le Pen became president, she has promised to hold a referendum on France’s future in the EU. If that referendum were to lead to Frexit, the EU would be finished the next morning. So would the euro.

A French or Italian exit from the euro would bring about the biggest default in history. Foreign holders of Italian or French euro-denominated debt would be paid in the equivalents of lira or French francs. Both would devalue. Since banks do not have to hold capital against their holdings of government bonds, the losses would force many continental banks into immediate bankruptcy. Germany would then realise a massive current account surplus also has its downsides. There is a lot of German wealth waiting to be defaulted on.

Therein lies the problem. Any exit from the euro is an instant Lehman moment, only much, much larger. Huge sovereign and private defaults would trigger a run on the exiting country’s assets, as well as those at risk of exiting. It would make holding euro and euro-denominated assets as reserves a laughing stock and throw global markets into unimaginable chaos as counter-parties everywhere shock froze. Within a few months it’s likely that the world would sink into a second Great Recession, if not worse. And that economic fallout would probably make the politics of fragmentation even worse.

The fallout worldwide would be a (probably permanent) current account reset, effectively ending Australia’s externally-funded growth model overnight, much as it did in the shocks of the 1890s. The Great Australian Housing Bubble House would crash given this time we have little policy support to offer it as rate cuts hit zero, fiscal policy was hit by successive downgrades and immigration reversed on Trumpian politics.

Advertisement

The global policy response would be wholesale helicopter money in support of government debt and deficits. The G20 may be able to rally to support a global Marshall Plan for helicopter-funded global infrastructure so once past an shock reset, with asset prices reset, Australia could recover OK with commodity demand.

This is why I see gold as a necessary holding. Although the US dollar would rocket, I can’t imagine how this kind of monetary chaos could transpire without gold also launching. Perhaps the safest bet is to hold both in a pair trade.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.