This year’s massive rise in coal prices is both bewildering and exhilarating.

Coal is Australia’s second largest export — 11 per cent of the total, just behind iron ore, which is 15 per cent. If the full rise in coking and thermal coal prices flows through to contract prices, it would boost exports by close to $US40 billion ($52bn), or 2.5 per cent of GDP.

For example, this week, Glencore said it was going to reopen the Integra coalmine in the NSW Hunter Valley, just weeks after announcing it would reopen the Collinsville mine in Queensland. These businesses will employ people, pay taxes, add to GDP.

…If it keeps up, and that is still a big if, Australia’s economic growth will accelerate, wages and inflation will rise, interest rates will move up and bring down Melbourne and Sydney house prices, and the federal budget will more quickly head back into surplus, without the need for significant spending cuts.

In other words, Australia’s entire economic narrative is in the process of being transformed.

Kohler is a pretty useful “magazine cover indicator”, having form ringing the bell at previous major market turning points. He’s not alone today of course, the RBA also sees a commodity price bottom, from yesterday’s SoMP

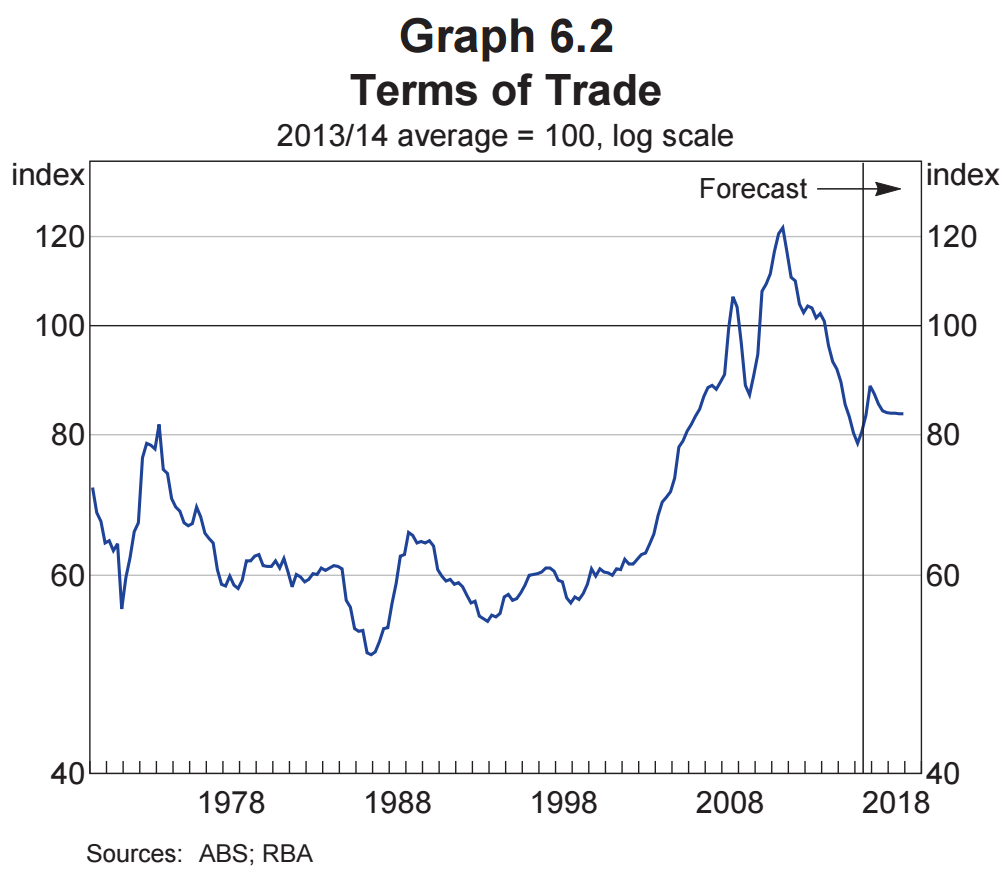

Australia’s terms of trade increased in the June quarter for the first time in 2½ years, and look to have risen again in the September quarter, led by higher bulk commodity prices. The terms of trade are forecast to remain above the levels reached in early 2016 (Graph 6.2). The outlook for commodity prices, particularly coal prices, is more positive than previously thought, reflecting an improved outlook for Chinese steel production in the near term and cuts to the production of bulk commodities in China, although current levels of spot prices are not expected to be sustained.

Advertisement

Though it, too, has a very poor record:

It’s going to be right eventually. Is this it, still above the highest terms of trade in history pre-China boom?

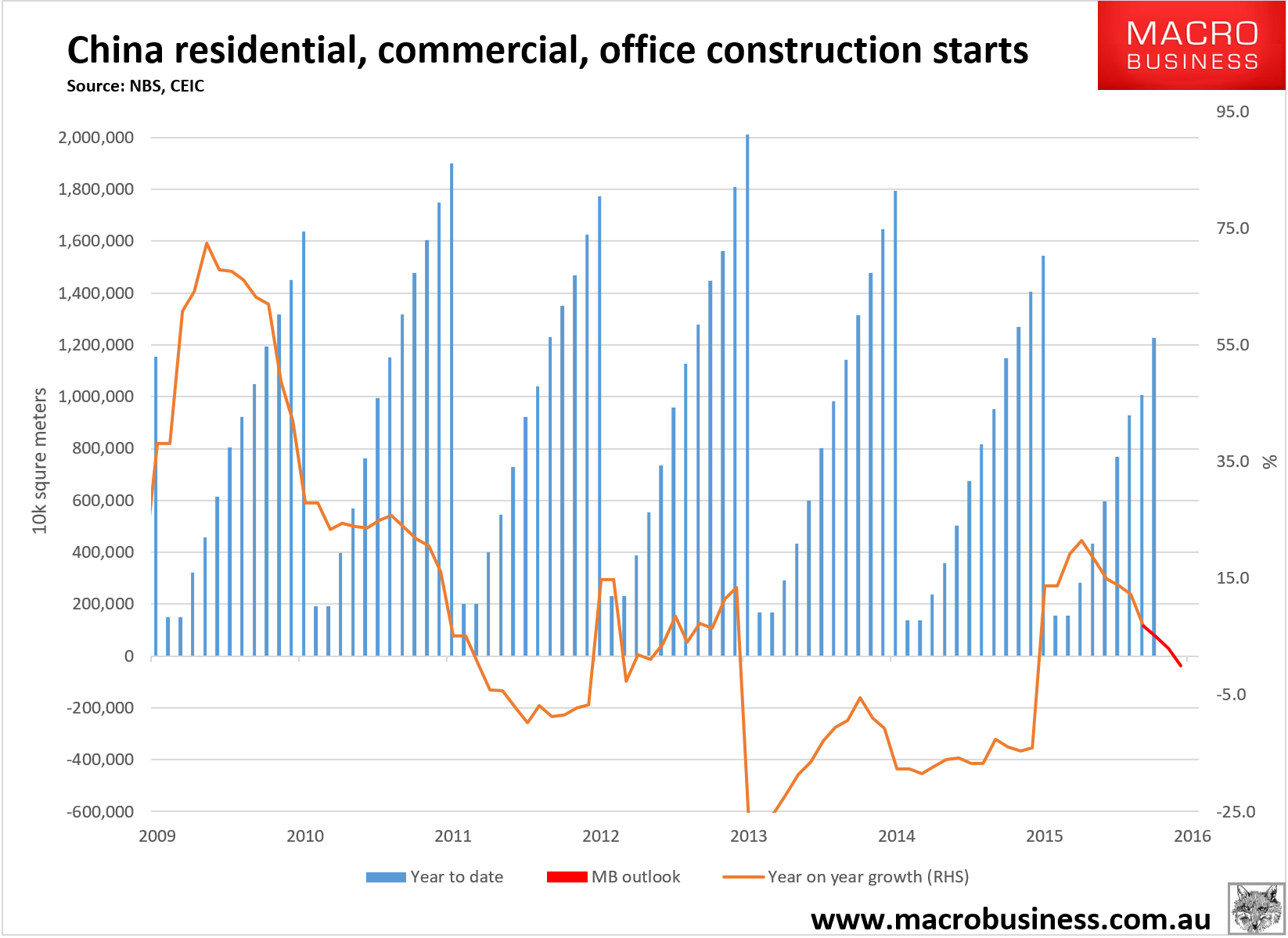

I don’t think so. My own outlook for iron ore this year has proven too bearish even as I got coal right. But the evidence still points towards a full correction of the current terms of trade boomlet and then even more downside. The key is Chinese construction starts which continue to decelerate quickly as expected:

Advertisement

Indeed, on some measures they are already falling. The improved fundamentals are real but slipping.

Meanwhile, all three bulks are in (not so) little bubbles. From the FT:

Advertisement

Chinese hedge funds are providing margin finance for leveraged bets on the country’s booming commodity futures market, in an echo of the practices that led to last year’s stock market boom and bust.

…Rising commodity prices have in turn fuelled speculation in the futures markets. Trading volume in front month coking coal futures in Dalian hit 7.6m in October, the third-largest month on record behind March and April, when China was first gripped by a commodities frenzy.

Commodity trading has surged in China as retail investors, rich individuals and wealth managers use the sector as a quick and easy way to place leveraged bets on the domestic economy or government reforms.

The surge in speculation activity has rattled global commodity markets, causing a sharp run-up in the price of raw materials such as steel and iron ore futures. That has astonished western trading houses and analysts accustomed to following the fundamentals of supply and demand.

Some hedge funds are using structured investment products to provide margin loans to investors looking to ride the futures boom. Hedge funds generally buy the senior tranche, which promises a fixed return. Punters buy the equity tranche, which pays fixed returns to the senior tranche as interest on the margin loan. After the interest is paid, punters keep any additional profits from the futures trade.

A hedge fund manager in Shanghai said: “These are hedge funds looking for fixed returns. They’re not familiar with commodities, so [this] strategy looks good to them. Someone else takes the big risk.”

But this form of margin lending, known in Chinese as peizi, mirrors the type of shadow bank-style margin financing that helped fuel the Chinese stock market boom last year. Once the market turned, margin calls amplified losses as investors were forced to liquidate their holdings to repay loans.

Regulated margin lending through securities brokerages for stock market investment caps leverage at Rmb2 of borrowed funds for every Rmb1 of the investor’s own money. The 21st century Business Herald reported on Wednesday that peizi for commodity futures investment can reach as high as 4:1.

An official at the National Development and Reform Commission, China’s top economic planner, told state media this week that recent increases in coal prices are “irrational”, citing speculation as one explanation.

A trader at a futures brokerage in Shanghai said: “The speculative element in the market is very big right now. End users and those trying to do hedging are getting killed.”

It must always be remembered that every market that China touches eventually turns to shit and now it is bulk commodities turn for a bit. The question that Australia’s over-excited doyens of dirt should be asking is when will it pop?

My views on that are unchanged. All three bulks are enjoying major restocking pulses but:

Advertisement

thermal coal is an abundant and flexible market and China has already rebuilt half of its inventories so the price is going to peak this quarter (maybe already). I see it at half current levels within a year;

coking coal is less flexible but as Alan points out the supply response is underway. The spot price is probably somewhere near its peak today given the restock is also roughly halfway done but will remain higher for longer because mines need to be re-opened and that takes time. I still see it at half current prices within a year as well;

iron ore is also a flexible and abundant market so its peak must be very close too. It’s restock only has 5mt to run before ports have the most dirt in history. Next year it’ll see another new 50mt of super-cheap ore. I see it down a third within a year.

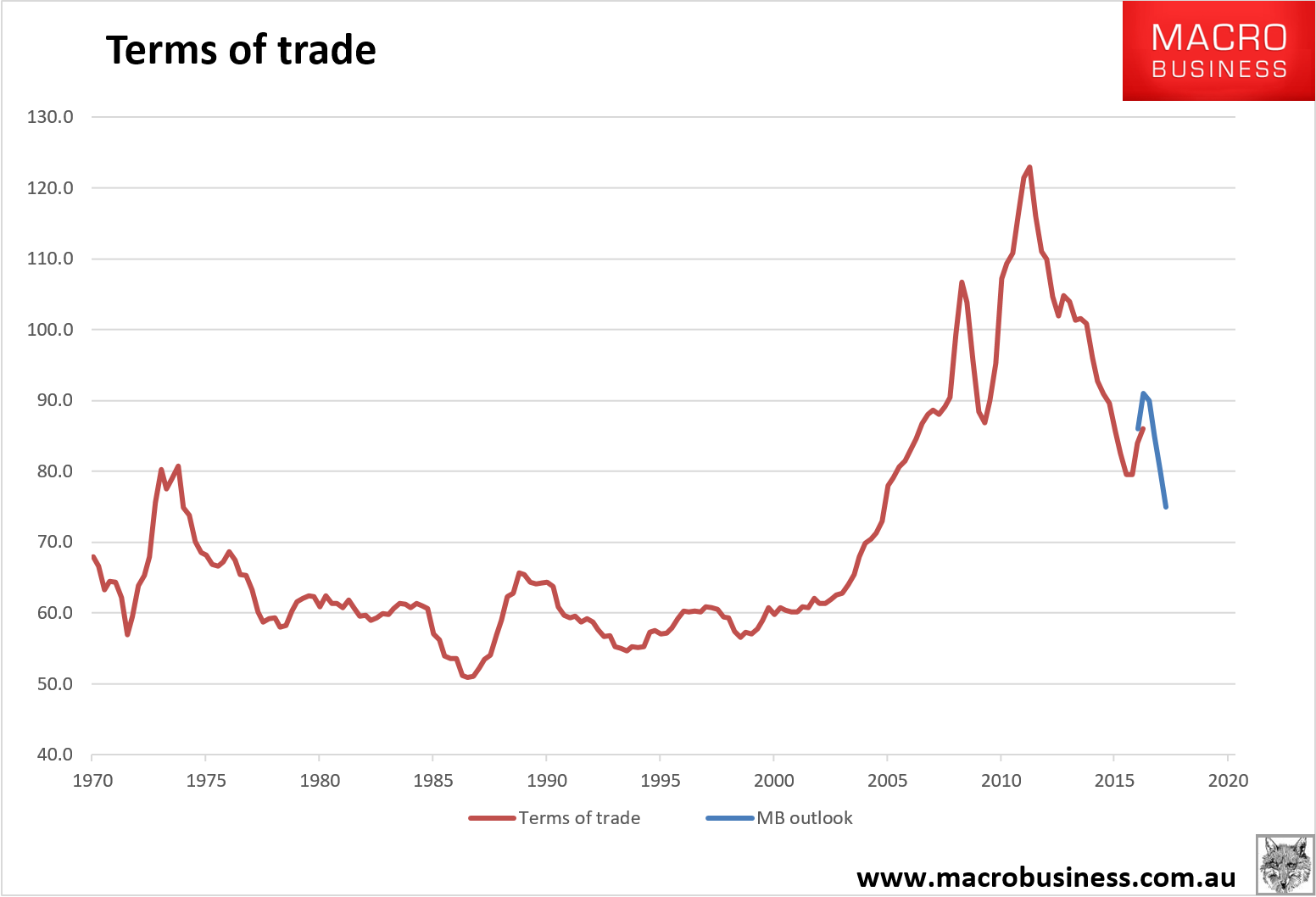

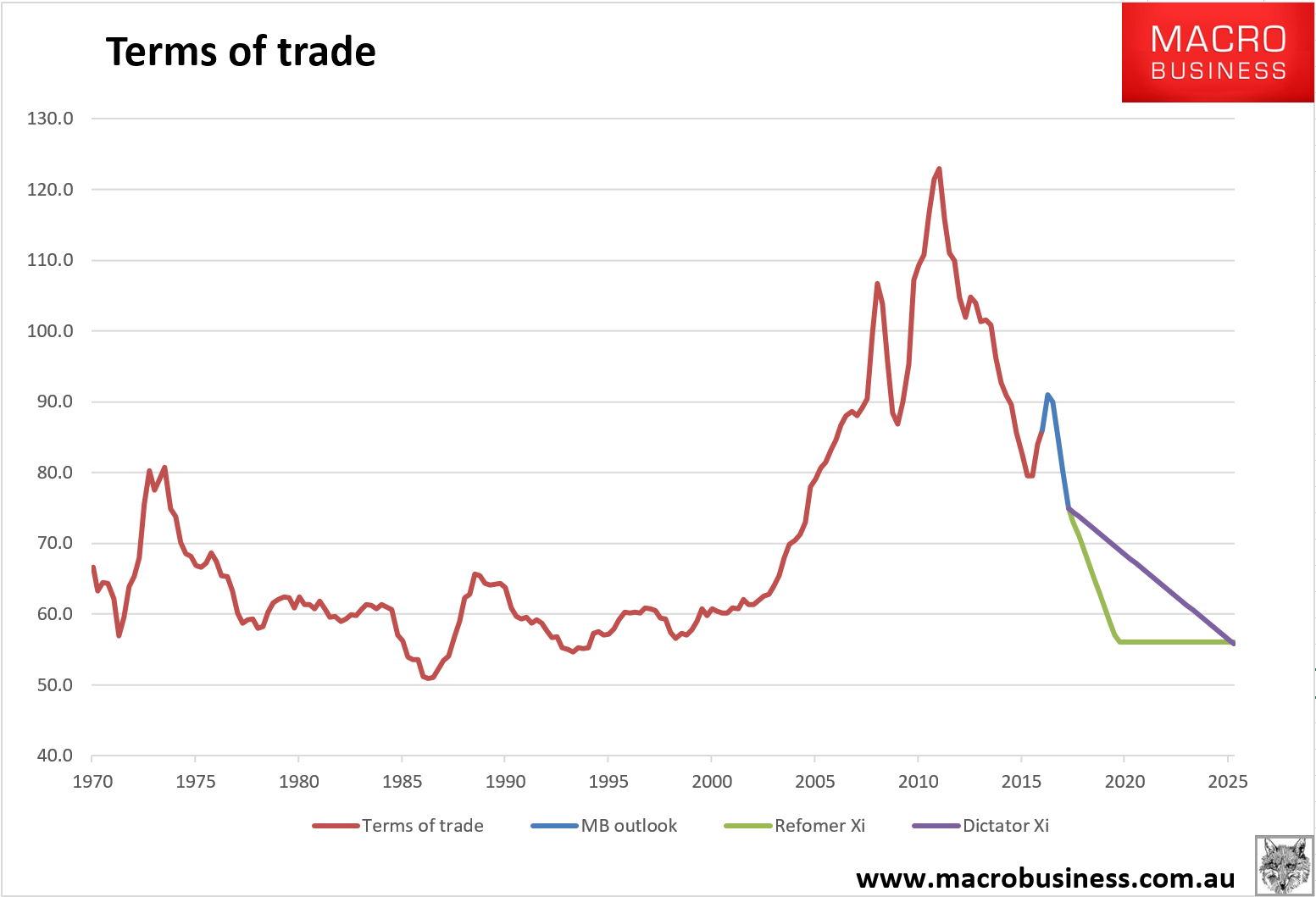

That’ll look like this for the terms of trade:

The big question for me now is at what pace will it continue to correct after the bubblet pops? Chinese policy-making has undergone a transformation in the past year. The economics of what China needs to do to escape the developmental “middle income trap” are obvious. It needs reform to reboot productive capital allocation.

Advertisement

But as Xi Jinping morphs into the new Mao Zedong, a “Paramount Leader” increasingly likely to hold power beyond his allotted ten year tenure, what China needs and what Xi needs may no longer be the same thing. I have until now reckoned that the CCP under Xi considered reform a priority because the alternative path of debt-charged super growth risked crisis at some point and it was therefore an symmetric bet on retaining power. But if China has proven anything in the past eighteen months it is that it has the resources to continue down the Japanese-style stagnation path more or less indefinitely without such a crisis appearing.

Thus Xi may now reason that it is the path of reform, and the many losers that it creates, that is his and the CCP’s most obviously risky path in terms of retaining power.

So, today I am tossing up between a Xi that returns to reform-oriented policy after he stacks the Politburo at next year’s 18th National Congress of the Communist Party of China. And a Xi that deliberately takes China down a path of slow stagnation that he can rule relatively comfortably via increasing centralisation for as long as wishes.

Advertisement

The end result is the same for Australia’s terms of trade over a decade but the paths getting there are different given the commodity-intensity of Chinese growth will differ materially:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.