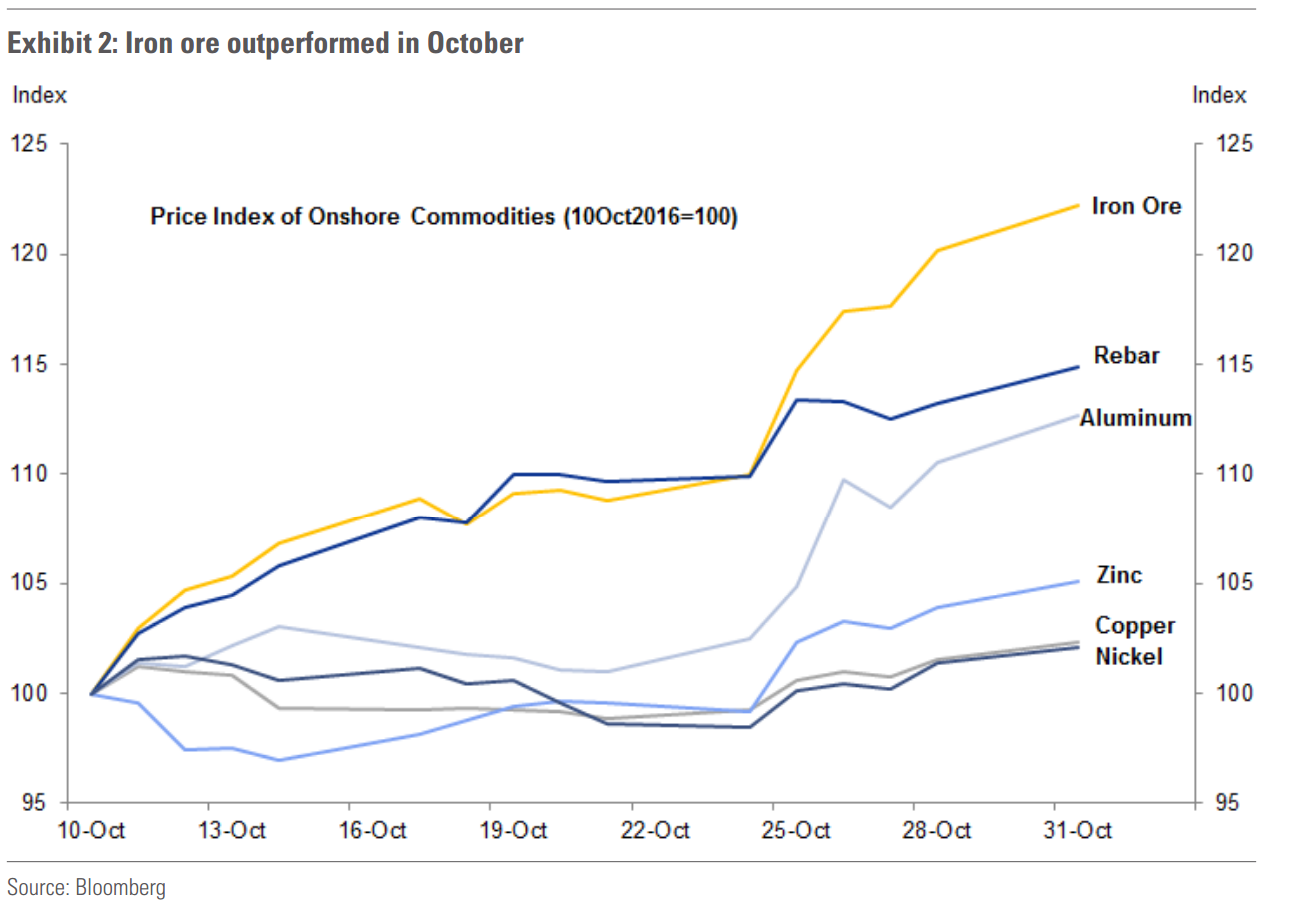

Over the past three weeks, iron ore in the Chinese onshore market experienced an impressive 22% price gain and outperformed other commodities (Exhibit 2). At the same time, there have been several new economic and market developments in China. The September credit data released in mid-October surprised to the upside. Coal prices continued to climb despite recent government announcements to encourage production. After pausing in Q3, CNY resumed its depreciation against the US Dollar. Do these developments help explain the October ferrous rally? In this note, we examine the contribution of the three factors –growth expectations and supply/demand fundamentals, coal prices, and $/CNY – to the recent iron ore price rally. We conclude that the weaker currency may be the most important driver.

Is it growth expectations and supply/demand fundamentals? Unlikely

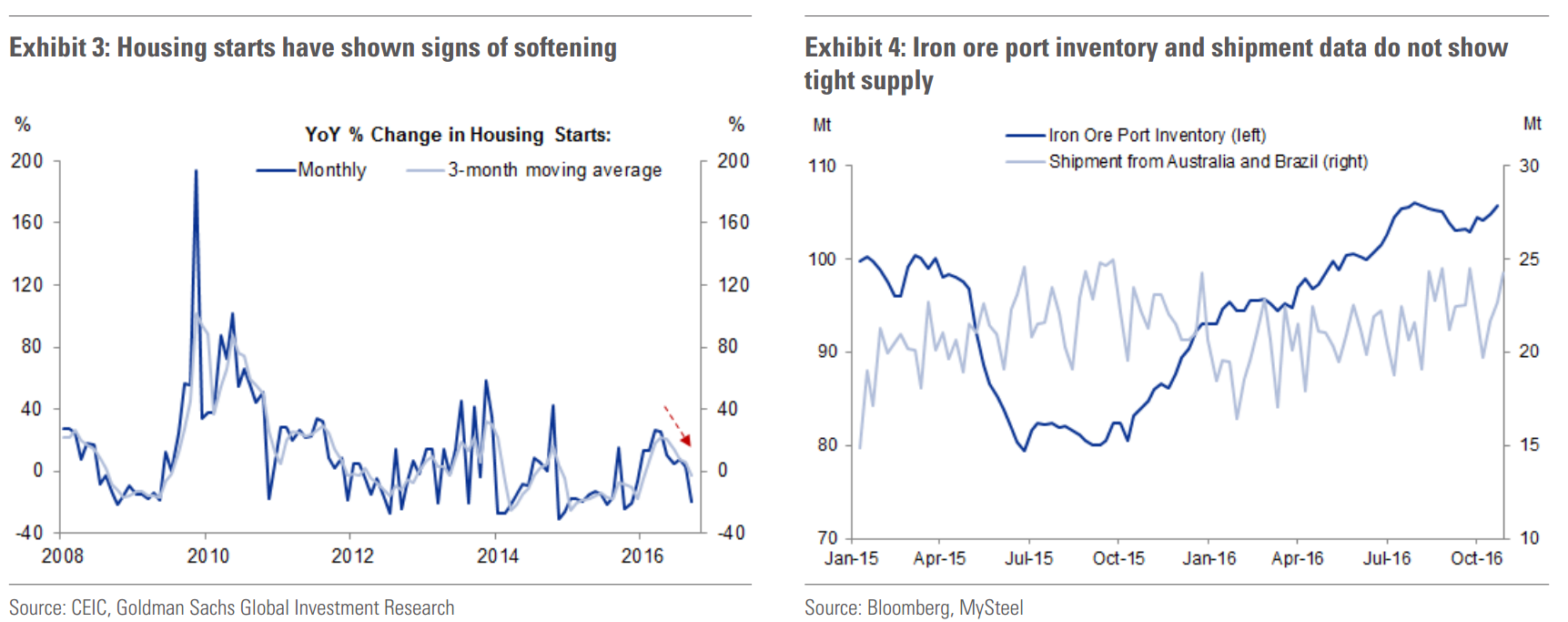

Iron ore and steel demand is highly sensitive to infrastructure and property investments in China. One of the key reasons why iron ore prices rallied significantly earlier this year was the credit injection unleashed in late 2015 and early 2016, which boosted infrastructure and property investments. But credit growth is not accelerating and the steel intensity of fixed-asset investment in China has been trending down. Although the September total social financing (TSF) data beat market expectations and the infrastructure pipeline suggests solid steel demand in the near term, we see the demand picture as stable with downside risk from the property market in the medium term (Exhibit 3). On the supply side, iron ore port inventory continued to build in October. Shipment data suggest that iron ore exports out of Australia and Brazil have been rising (Exhibit 4). Taken together, we do not think the October ferrous rally can be explained by an optimistic outlook on steel demand or by supply tightness in the iron ore market.

Is it high coal prices? Not for iron ore

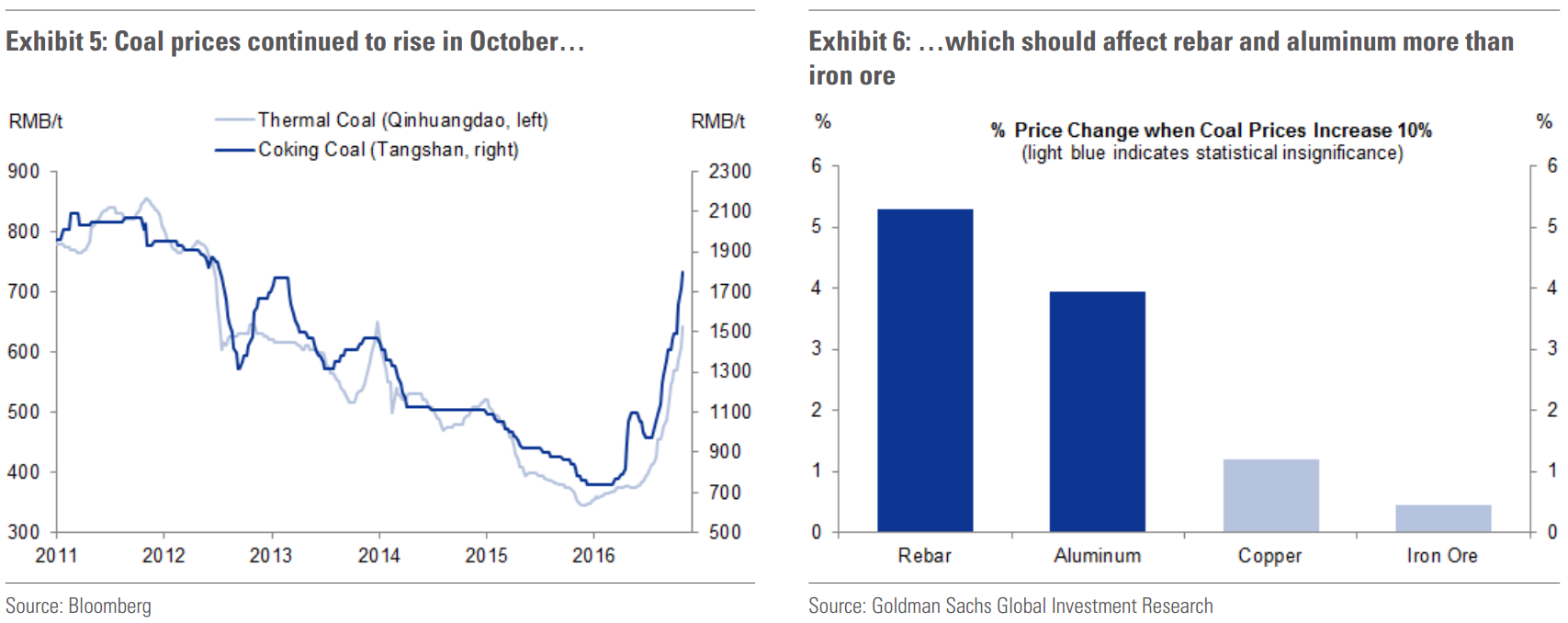

The coal price increase in 2016 has been striking (Exhibit 5). Year-to-date, thermal coal prices have risen 80% and met coal prices have jumped 140% in the Chinese onshore market. With the winter coming and coal prices climbing, the Chinese government has partially reversed earlier policies to cut production. However, the effect on coal prices from this policy reversal is likely to take some time to play out.

Because coal is an input for the metals industry, higher coal prices can be passed onto end-users via higher metal prices. To test if this is the main driver of the October ferrous rally, we look at the historical relationship between movements in coal prices and movements in the prices of iron ore, rebar, copper and aluminum. Our estimates show that the effect of coal prices is the largest for rebar and aluminum, but small and insignificant for copper and iron ore (Exhibit 6). This result makes intuitive sense since metallurgical coal is a key input for steel making and aluminum smelting relies on coal-fired power generation. From a fundamental perspective, more expensive steel, when driven by higher coal prices, should not boost the demand for iron ore. But in the short run, behavioral explanations such as the belief that iron ore prices should follow steel prices could affect the market.

One caveat is that expensive met coal encourages steel makers to use high-grade iron ore, since the higher Fe content of the iron ore, the less met coal is needed in making steel. Indeed, the price of 62% iron ore has increased more than the price of 58% iron ore has. But the fact that even the lower grade iron ore is experiencing notable price gains is at odds with the coal story. Taken together, we think higher coal prices help explain the recent rally in rebar and aluminum, but are not the main driver behind soaring iron ore prices.

Is it CNY? Most likely

$/CNY was one of the most important market drivers of 2H 2015. When China weakened its currency in August 2015, it sent shockwaves around the globe with the S&P 500 index falling 10%. In the third quarter of 2016, $/CNY stayed range-bound between 6.6 and 6.7. In October, however, the depreciation resumed and $/CNY is now approaching 6.8.

The recent CNY depreciation is different from previous rounds of $/CNY moving higher. It has not generated the same international spillover effects as it did back in 2015. This implies further room for the Chinese government to weaken its currency against the US Dollar without negatively affecting global demand for its exports. On the other hand, the link between $/CNY and capital outflows remains strong. Our China Economics team estimated that FX outflows from China rose to US$78 billion in September and are likely to be even higher in October (Exhibit 7). This implies that there is an underlying desire among onshore investors to move into dollar-linked assets. Such desire may become particularly strong whenever the pace of CNY depreciation picks up. In fact, onshore commodities prices increased across the board on October 25 after the $/CNY moved higher for three consecutive days.

There are reasons why iron ore may be the first in line to benefit from onshore investment flows into commodities amidst renewed CNY depreciation. For example, the iron ore futures curve is almost always backwardated, making long iron ore a positive-carry trade. To the extent that a higher $/CNY also leads to a weaker local currency on a trade-weighted basis, iron ore may benefit from potentially higher Chinese steel exports. Additionally, rebar and iron ore are the most traded commodities in the onshore futures exchanges. Exhibit 8 shows the positive correlation between iron ore futures trading volumes and the $/CNY in recent months. By our estimates, about 60% of the iron ore price rally in October can be explained by the CNY depreciation.

In summary, contrary to the market chatter and media report on higher coal prices driving higher iron ore prices, we think that $/CNY has played a more important role. Going forward, we see further room for CNY depreciation given the high likelihood of Fed hiking in December. With ample onshore money supply chasing a limited menu of accessible dollar-linked assets, continued CNY depreciation means that iron ore prices may stay above what the fundamental demand and supply suggest in coming months.

Fair enough though seems a bit elaborate. Iron ore has been going up because underlying demand is decent and speculators have been hoarding it. Coal has played a role in the sentiment spillovers to the latter group.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

Is it high coal prices? Not for iron ore