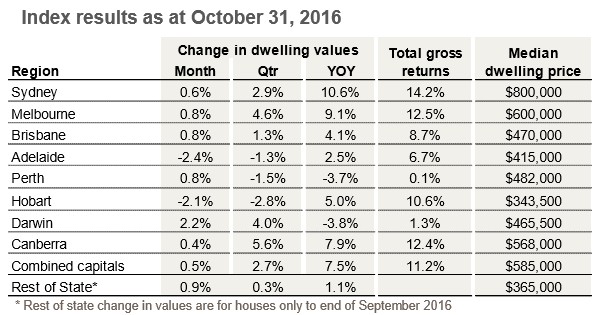

Following on from yesterday’s post on CoreLogic’s daily dwelling values index results for October, CoreLogic has released its full results, which also cover the smaller capitals and regional areas (see next table).

As shown above, the smaller capitals and the regions had a mostly positive month in October, with Darwin (+2.2%), Canberra (+0.4%) and Rest of State (+0.9%) recording value rises, but Hobart (-2.1%) recording a fall.

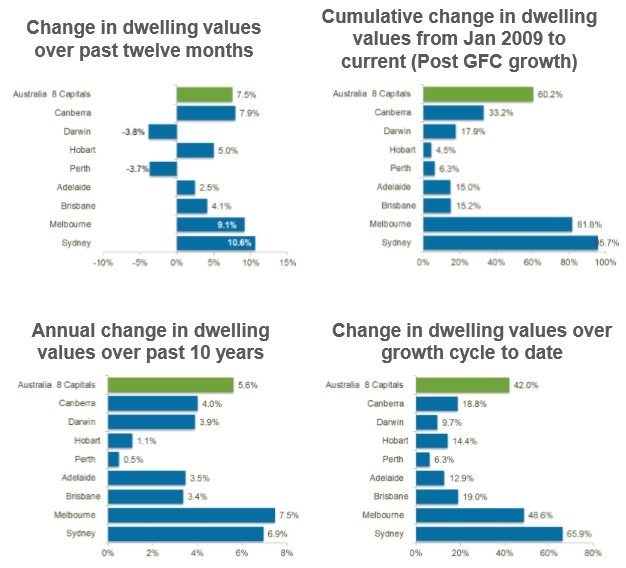

Below are the key charts summarising the situation across the markets, with Sydney and Melbourne dominating:

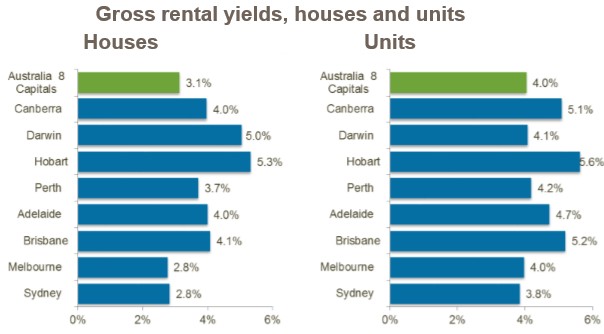

The combination of weak rents and capital appreciation continues to compress rental yields, which have fallen to record low levels:

According to CoreLogic:

“The typical Sydney and Melbourne house is now providing a gross rental return of just 2.8%. Taking into consideration holdings costs, expenses and vacancy, the net rental yield for houses is likely to be closer to 2% in these markets. Markets where value growth hasn’t been as strong are seeing healthier yield profiles, with Hobart demonstrating the highest gross rental yields of any capital city.

Mr Lawless said, “High values, low yields and a mature growth cycle haven’t been enough to deter investors from the market. Housing credit data released by the RBA earlier this week provides some insight into increased demand from the investor segment. Over March 2016, investor housing credit grew by just 0.29% and this has consistently increased to 0.62% over September”.

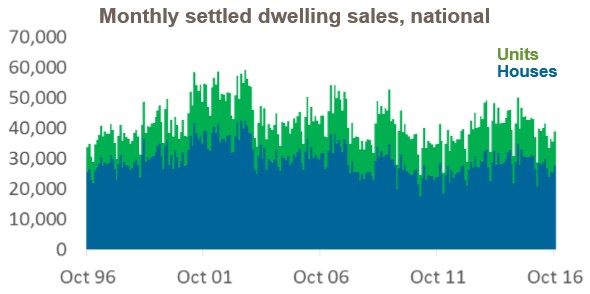

CoreLogic also reports that listings and transaction volumes are depressed:

The latest national listing estimates from CoreLogic show total listing numbers remain 2.6% lower than a year ago…

Mr Lawless said, “Low stock levels tend to create a higher level of urgency in the housing market as buyers compete with each other and vendors are less willing to negotiate on prices. This may be one reason why transaction numbers have reduced over the year. The CoreLogic turnover estimates have recently levelled after trending lower since April 2015, however settled dwelling sales over the three months ending October 31 remain 13.9% lower than the same three month period in 2015.

These estimates do not include off-the-plan sales, which, according to Mr Lawless, implies there is likely to be a level of upwards revision in the numbers as the record number of off the plan units move through to settlement.

He said, “Other factors that are likely to be dampening transactional activity include the high transactional costs such as stamp duty and selling fees, affordability constraints in markets where values have risen substantially and tighter lending policies being implemented by the banks.”