Goldman doesn’t say so exactly but it sure does hint at it:

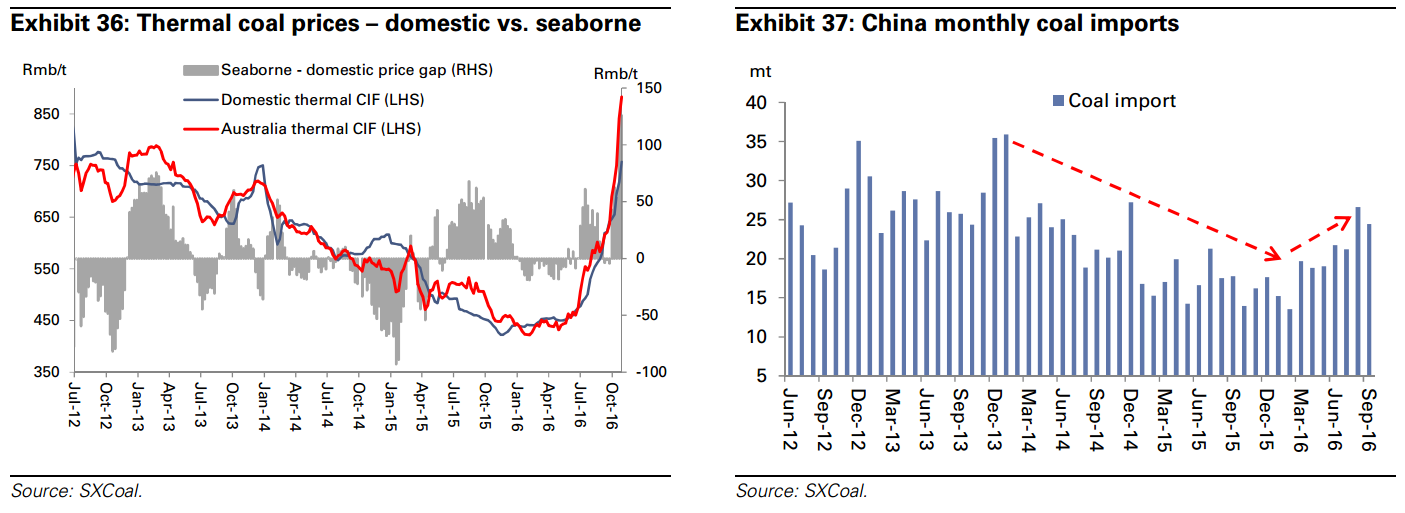

A perfect storm of supply interruptions, but rally too much too fast YTD thermal coal prices for both QHD and Newcastle posted significant rallies of 80% and 100%, respectively. These sharp rallies have been driven by a perfect storm of coal production and transportation interruptions as well as a demand pick up.

1. The most important driver of the rally in coal prices ytd has been supply-side reform being carried out faster and better than for downstream sectors including cement, steel and aluminum as evidenced by the diverging output growth. In 9M16, the output of coking coal, thermal coal and coke fell 14%, 10% and 3% yoy, respectively, while the output of steel, thermal power, aluminum and cement rose 0%, 1%, 2% and 3%, respectively. Such diverging output growth has led to significant outperformances of coal prices over other commodities.

2. The second key development driving the coal prices rally ytd is the ongoing crackdown on trucks overloading which has led to a sharp drop of coal transportation capacity and a spike of trucking charges, which now has even spilled over to rail as evidenced by the rising rail freight.

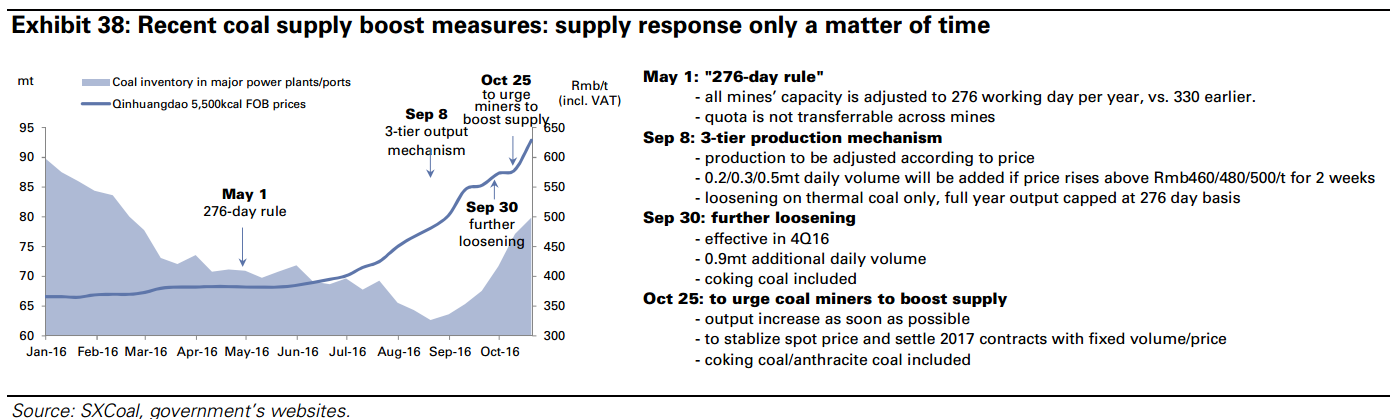

3. The coal production and transportation interruptions have caused short-term coal market tightness. Coal inventory at IPPs dropped to as low as 11 days as of September 10.

4. The domestic coal market tightness and the subsequent coal prices rally have incentivized more imports, pushing up seaborne coal prices. In 9M16, China’s coal imports were up 14% yoy off an already very high base in 2015.

However, we view the coal prices rally as too much too fast, and we believe it is unlikely to be sustainable at current levels for the following three reasons:

1. With persistent overcapacity, the supply resumption is only a matter of time, either triggered by government policies or incentivized by improving profitability. Since late September, China’s central NDRC had begun to relax coal production control by allowing more advanced (safe and high efficiency) coal mines to increase output. Based on such criteria, there should be around 900 coal mines with a total of 1.8btpa in coal capacity producing on a 330-day per annum basis during October-December 2016. We estimate this would add 0.9mt daily volume (vs. 0.5mt earlier), including 20% raw coking coal (vs. nil previously).

On the back of all these supply boost measures, we expect China’s monthly coal output to gradually increase in the next few months, and we note the recent monthly coal output growth rebound of China Shenhua and China Coal.

2. We expect China’s long-term coal demand growth still on a structural downward trajectory as a combined result of: 1) economic growth transition; and 2) the ongoing environment cleanup efforts through the replacing of fossil energy with renewable energy.

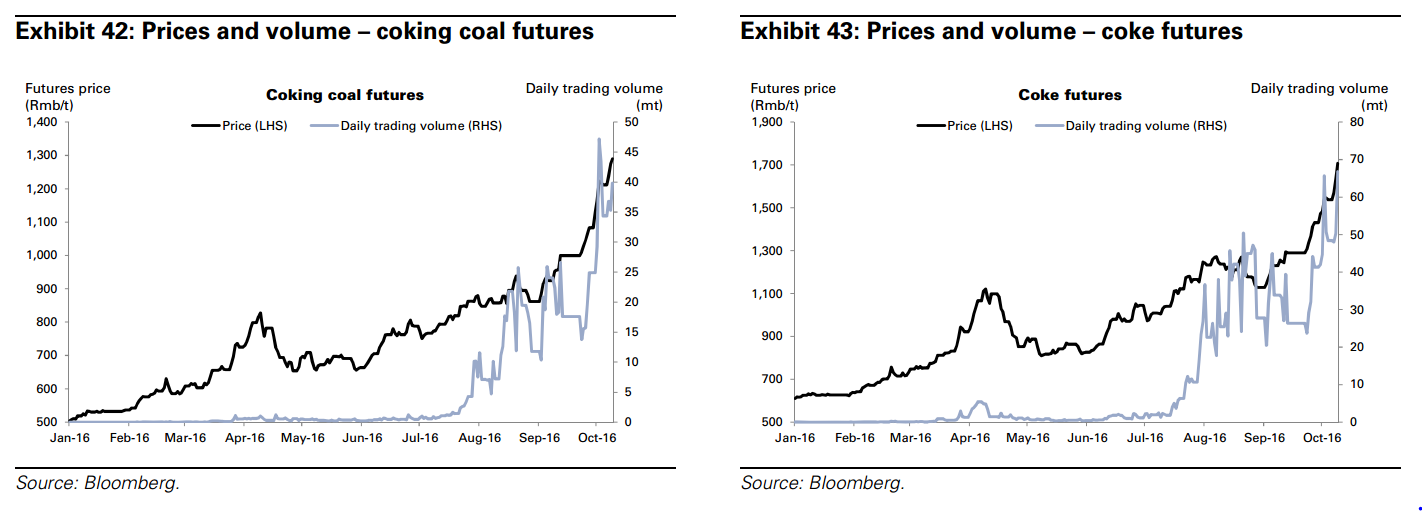

3. We believe the speculative investment forces contributing to the coal prices rally are unlikely to be sustainable either, especially for coking coal and coke. Such massive speculative investment took place in the iron ore and rebar futures market in March/April, and now in the coking coal and coke futures market. Once again this shows how excess liquidity chasing return in a persistently low yield environment is rotating among assets classes, and is therefore, hard to sustain. As shown in Exhibits 42-43, the daily trading volume of coking coal and coke futures has surged exponentially since late July by taking advantage of the supply-side reform policy announcement then. The current daily trading volume of coking coal/coke accounts for around 10%/30% of China’s annual demand.

I wouldn’t call it a bubble exactly, either. It’s a short term supply shock. Looks to be very nearly over in thermal. Will take a few quarters to resolve for coking.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.