ABC’s The Business aired an interesting segment examining calls for Australia to re-introdude an inheritance, which used to exist in Australia until late-1970s and early-1980s.

The segment features a number of experts including ‘rockstar’ French economist Thomas Piketty, Mark Carnegie, and Australian economist Frank Stilwell, who note the benefits in principle. However, they all concede that implementing an inheritance tax in Australia is next to impossible due to the political barriers.

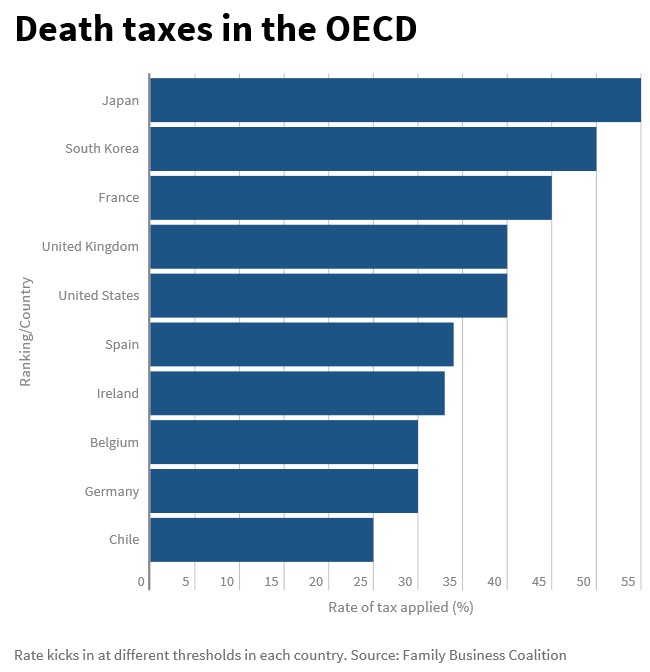

National inheritance taxes exist in many other developed countries, such as the UK, USA, Germany, Belgium, the Republic of Ireland, France, and Japan (see next chart via Fairfax).

Australia also used to have inheritance taxes. But in 1978, Queensland Premier Joh Bjelke-Petersen abolished the state’s inheritance tax, which was followed by the governments of other states. Prime Minister Malcolm Fraser then followed suit and eliminated the federal inheritance tax

The Henry Tax Review also gave in-principle support for an inheritance tax (called a “bequest tax” in the report), noting that it would be economically efficient and equitable. Still, it shied away from outright recommending re-introducing a bequest tax because of its controversial history:

A bequest tax would be a relatively efficient means of taxing savings. Decisions to save taken solely to fund consumption later in life would be unaffected. But decisions to save motivated by the desire to leave a bequest would be affected and this would impose some efficiency costs. In aggregate, though, bequest taxes are not likely to introduce large biases into donor behaviour. A bequest tax could increase labour supply and savings by recipients and prospective recipients, though the effects would be limited.

Such a tax could also be a progressive element of the tax and transfer system. Because the distribution of wealth in Australia is so uneven, most of the revenue available from a bequest tax could be raised from the top 10 per cent of households by wealth.

A tax on bequests would fit well with Australia’s demographic circumstances over the coming decades. Over the next 20 years, the proportion of all household wealth held by older Australians is projected to increase substantially. Large asset accumulations will be passed on to a relatively small number of recipients. On the other hand, a bequest tax would be complex. There would be a need for anti-avoidance provisions, including a tax on gifts. There would, inevitably, be significant administration and compliance costs.

A tax on bequests should not be levied at very high rates. People should not be unduly deterred from saving to leave bequests. A substantial tax-free threshold combined with a low flat rate beyond that point would be an appropriate structure for a bequest tax. Bequests to spouses should be concessionally treated.

Another design issue is whether to tax the whole of the donor’s estate or the inheritances received by individual recipients. There are arguments on either side, but on balance, they probably favour taxing each estate as a whole. A large number of other design issues would need to be considered. The more concessions and exemptions in the bequest tax, the greater its complexity and the greater the risk to efficiency and equity goals.

The Review has not sought to recommend the introduction of a bequest tax at this time, but believes that there should be full community discussion and consultation on the options.

Given the extreme pressures on the Budget as the population ages, along with the growing tax burden being placed on the diminishing pool of workers, it would seem appropriate to at least place an inheritance tax on the Budget reform agenda.

OECD countries raise on average 0.41% of total taxation revenue from inheritance taxes. Even if this low rate was replicated in Australia, it could raise around $1.6 billion of additional Budget revenue each year.

But again, the political barriers are formidable. This leaves closing Australia’s inequitable and fast growing tax expenditures (concessions), as well as adequate taxation of land and resources, as worthwhile alternatives to help broaden the tax base and remove the burden from productive effort – especially labour income – to raise Australia’s growth potential.

unconventionaleconomist@hotmail.com