Cross-posted from Gareth Aird, senior economist at the Commonwealth Bank.

Key Points

- The recent decline in the unemployment rate, driven by a fall in participation, has masked the slowdown in job creation.

- Two big monthly increases in jobs recorded in October and November 2015 are about to drop out of the annual calculations.

- We expect to see the annual rate of employment growth halve from 1.4% in September to 0.7% by November.

- We have the RBA resuming policy easing in H2 2017.

What do the numbers say?

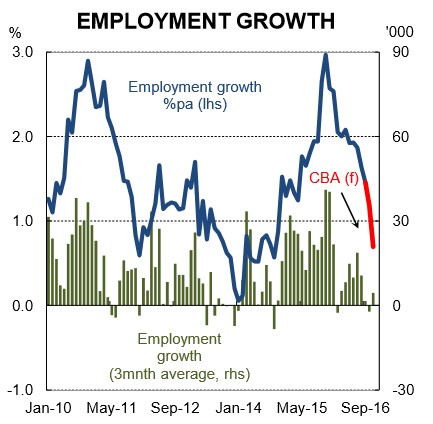

The annual rate of employment growth was reported to be running at a respectable 1.4% in September 2016. That rate had eased a little from 1.9% a few months earlier, but is still a decent pace of growth.

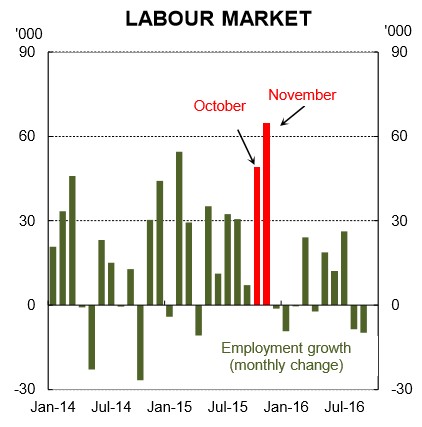

However, a closer examination of the monthly changes in employment shows that annual employment growth has been propped up by two very big increases in headcount in October and November 2015. According to the ABS, employment lifted by 49k in October and 65k in November. These incredibly large monthly changes were both two standard deviation events. And they threw up concerns at the time around the reliability of the data. Those concerns abated with the passage of time. But we are reminded of these data prints now that they are about to drop of the annual calculations.

Over 2016, monthly employment growth has averaged just 5.6k. And over the past three months it’s averaged just 2.6k jobs. These weak numbers have been disguised in the annual growth rates by the October and November prints last year. But that picture is going to change this month when we receive the October 2016 employment report. Only a big lift in employment of at least 50k jobs will stop annual employment growth from falling. Such a figure looks highly unlikely.

We expect the annual pace of employment growth to slow from 1.4% in September to just 0.7% in November. That figuring is based on a lift of 15k jobs in both October and November. That is where our near term forward looking indicators peg the pulse of jobs growth. Such an outcome should see analysts and policymakers alike focus a little more on the pace of jobs growth and what it is likely to mean for output, inflation and rates.

What does the RBA think?

Governor Lowe described the labour market indicators as being “somewhat mixed” in his Statement accompanying Tuesday’s decision to leave rates on hold. We beg to differ. In our view, a more accurate description of the labour market is “soft”.

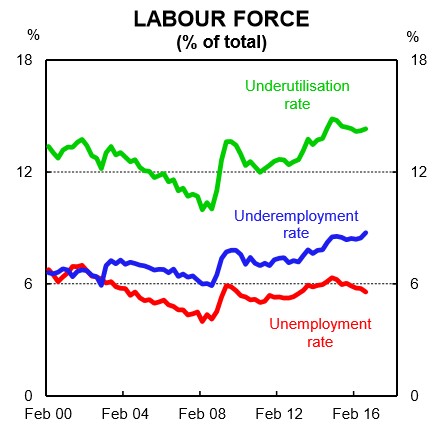

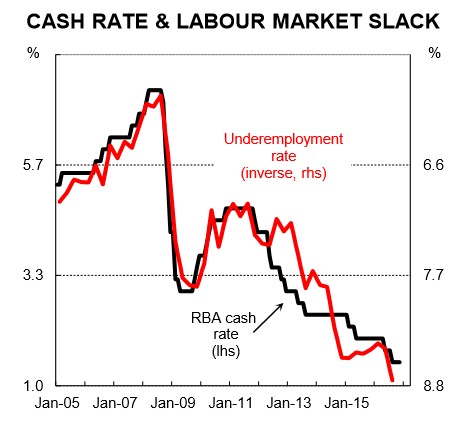

Employment growth has stalled and the annual pace of growth is set to slow sharply. Most of the jobs growth has been in the part-time space reflecting the casualisation of the labour market. And underutilisation, due to record high underemployment, is at its highest level since 1998. In addition, growth in total hours worked is weak and average hours worked is at its lowest level on record (31.9hrs). Throw in very weak wages growth and the only indicator left to sway a “soft” picture to a “mixed” one is the unemployment rate. But the driver more recently of the falling unemployment rate has been a declining participation rate. On an unchanged participation rate the unemployment rate would have lifted over 2016.

Where is policy heading?

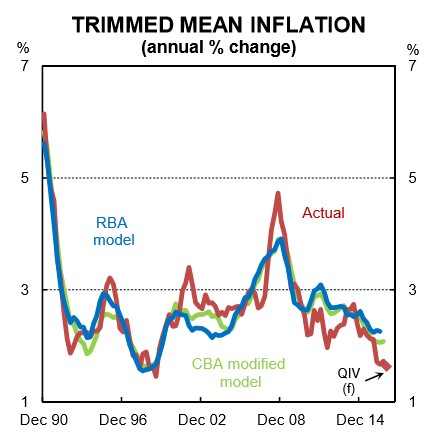

The near term focus for market participants will be Friday’s Statement on Monetary Policy (SMP). We don’t expect to see any material changes to the RBA’s inflation or growth forecasts. But we think that it’s too premature to call the end of the easing cycle. The inflation pulse is still incredibly weak at the moment. And our version of the RBA’s Philip’s curve (which runs on underutilisation rather than unemployment as the measure of labour market slack) points to inflation remaining around 1½%pa in QIV 2016 and well below target.

An uncomfortably high level of activity in the housing market and the bounce in commodity prices should fend off policy easing over the near term. But as conditions in the housing market cool, largely due to the combination of dwelling supply lifting and the stimulus of the May and August rate cuts fading, the hurdle to another rate cut will be lowered.

We don’t see enough strength in the labour market to push inflation higher. The unemployment rate may fall further, but other measures of spare capacity and labour demand suggest there will be little in the way of wage inflation to feed into consumer inflation. As such, we think 1½% won’t be the bottom of the cash rate cycle. And we think that current market pricing, which puts the terminal rate at 1.4%, is underestimating the chance of more policy easing.