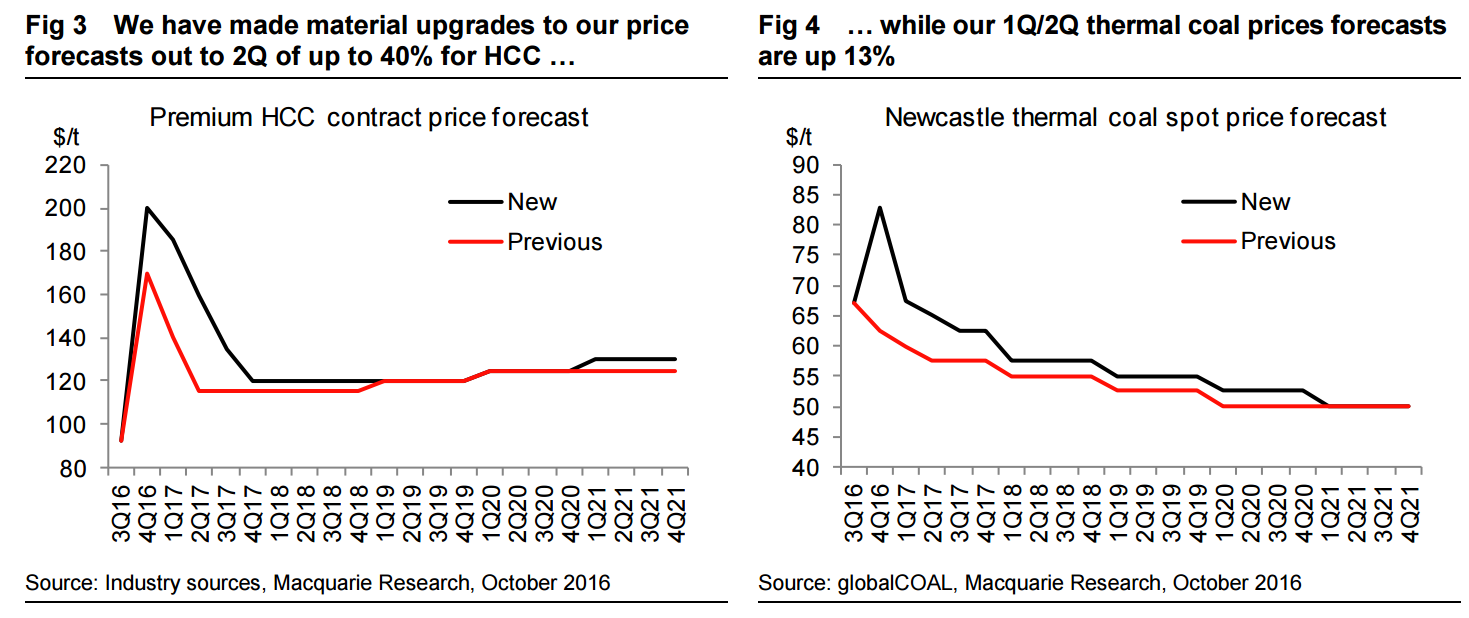

Macquarie has upgraded its estimated for coal today:

Since China’s NDRC announced a relaxation of coal production controls at almost 800 mines at the end of September, theoretically increasing effective production capacity by ~300mtpa and, hence, 4Q production by ~75mt, coal prices have accelerated higher. Spot Newcastle thermal coal is up more than $20/t, and spot Australian hard coking coal (HCC) is up $42/t.

As counterintuitive as that price move may seem, there is clear scepticism from market participants that production is increasing (there is no data yet to illustrate it), inventories remain at low levels and, even if that production increase did materialise, it does not fill the entire supply gap. As a result we have made material upgrades to our HCC and thermal price forecasts for the next two to three quarters but maintain a bearish trajectory, expecting a supply response to eventually materialise and start putting prices under pressure from 1Q.

When looking at both the met and thermal coal markets, it all comes down to China, where the domestic market is 2.5x the size of the whole seaborne market. As we illustrate in Fig 8, a 10– 13% YTD fall in Chinese met and thermal coal production has left both markets substantially short of material, which has led to significant destocking, only some of which is visible in published data. Imports have increased only modestly, up 10–15% YoY, but not for a lack of demand. Seaborne supply flexibility is limited, particularly in met coal, and has led to panic buying of marginal tonnes at higher and higher prices. In the case of hard coking coal, it has led to an import arbitrage that is currently $50/t closed, although the thermal coal arbitrage is still just about holding. Closed import arbs are justifiable in the short term if domestic material is inaccessible.

The import numbers illustrated below actually flatter the met coal market. Seaborne met coal imports are up just 5% YTD (+1.7mt YoY), with the rest of the growth coming across land from Mongolia. We think future seaborne supply responsiveness in met coal is much more limited than thermal as well, so we continue to favour long met coal/short thermal coal exposure as a pair trade. We expect thermal coal demand to be relatively weaker as well.

But all this needs some context; in a best-case scenario we could see 30–35mtpa of seaborne met coal supply response on a 12- to 24-month view and perhaps 90–100mtpa of thermal coal supply response. This is not sufficient to fill the market deficits incurred in 8M16 alone, which look relatively mild considering production controls were not imposed until late-March. The deficits are much larger at current production run rates and when considered on a full-year basis. Relative to last year’s annual average production run rate, saleable coking coal output is currently running 90mtpa lower, while thermal coal is running 220mtpa lower, versus a largely flat demand base.

What this means is that for prices to normalise, the market has to see a Chinese supply response. Prices alone would incentivise this normally, but given that output is essentially government controlled, it will require government policy being implemented via SOE producers.

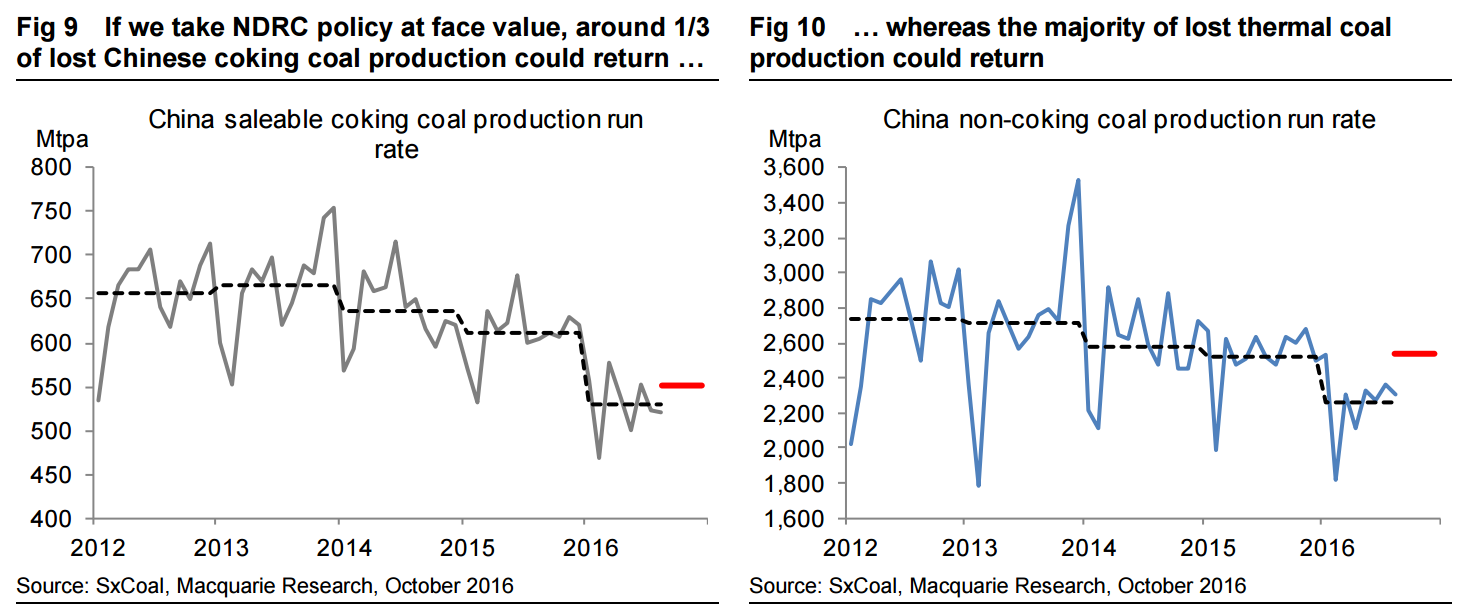

At the end of September, the NDRC announced a relaxation of coal production controls at almost 800 mines (increasing operating days from 276 back to the standard 330 days per annum), theoretically increasing effective production capacity by ~300mtpa and, hence, 4Q production by ~75mt on a raw coal basis. In terms of product breakdown, ~20% was coking coal capacity. The conclusion was that if all of this production came back online, the market would regain one-third of the lost coking coal production and the majority of the lost thermal coal production. This would surely then be price negative …

However, market participants have clearly dismissed this rhetoric over the past month, with prices continuing to rise. The reasons suggested are numerous:

Some of the mines outlined for production increase were already operating at more than the 276-day run rate.

The miners are choosing not to increase output, favouring better margins.

Both rail and road transport costs were increased, and trucking availability declined on regulation changes, increasing costs.

There are safety concerns around increasing output, and there was a recent safety incident in Shaanxi province.

Some of these explanations seem reasonable, others are tenuous. Either way it seems too early to conclude that production will not increase simply because production data does not already show that it has, considering production loosening was only first announced in early-September and the latest policy in late-September. We continue to believe that output will eventually rise, given clear signaling from the government that this is what it wants.

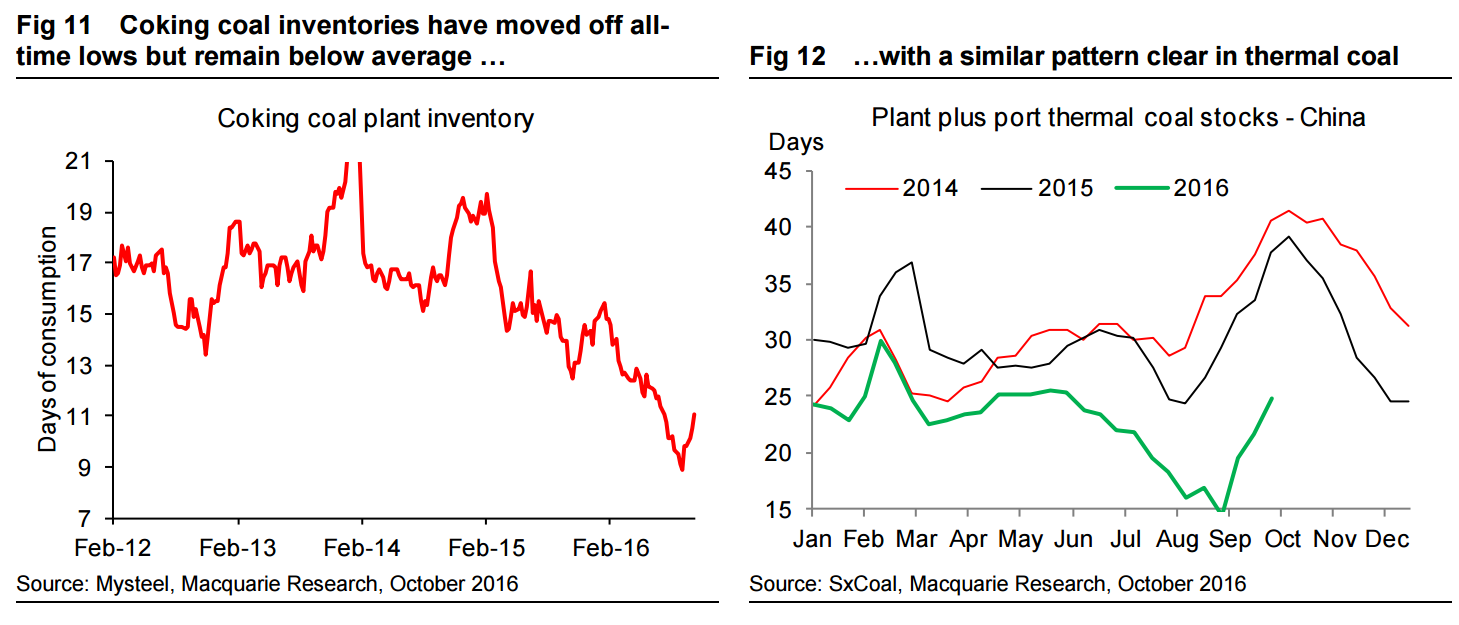

However, given inventories are below average and that we are heading towards seasonally stronger peak thermal coal demand and seasonally weaker production in the winter, market adjustment is likely to take time. Our revised assumption is that market tightness flows into 2017, before prices start to ease.

As a fair level for thermal coal, we continue to make reference to the NDRC’s earlier guidance that it wants thermal coal prices to fall back towards 450 RMB/t as a fair level during industry restructuring, which is a Newcastle price equivalent of $60–65/t.

For met coal we assume contract prices fall back towards a fair level of $120/t, which is around the top of the seaborne cost curve.

Both of these steady-state price levels are assumed to materialise in late-2017, although this time frame depends on how the Chinese government progresses in restructuring/consolidating the coal industry. Certainly risk appears skewed towards prices staying higher for longer, as restricting progress thus far has been very limited.

More than fair. Once the restock ends, prices will fall fast.

A more interesting question is can the higher prices keep the iron ore boomlet going as well? It should be the opposite but as we’ve seen the coal short squeeze has put a speculator bid into everything. It certainly looks possible for this quarter but I still expect iron ore to come off fast next year. The property slowdown will impact it more directly than coal and the supply deluge pours in again in Q1 ’17. With a backdrop of falling coal from Q1 it’ll get lots of downside momentum.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.