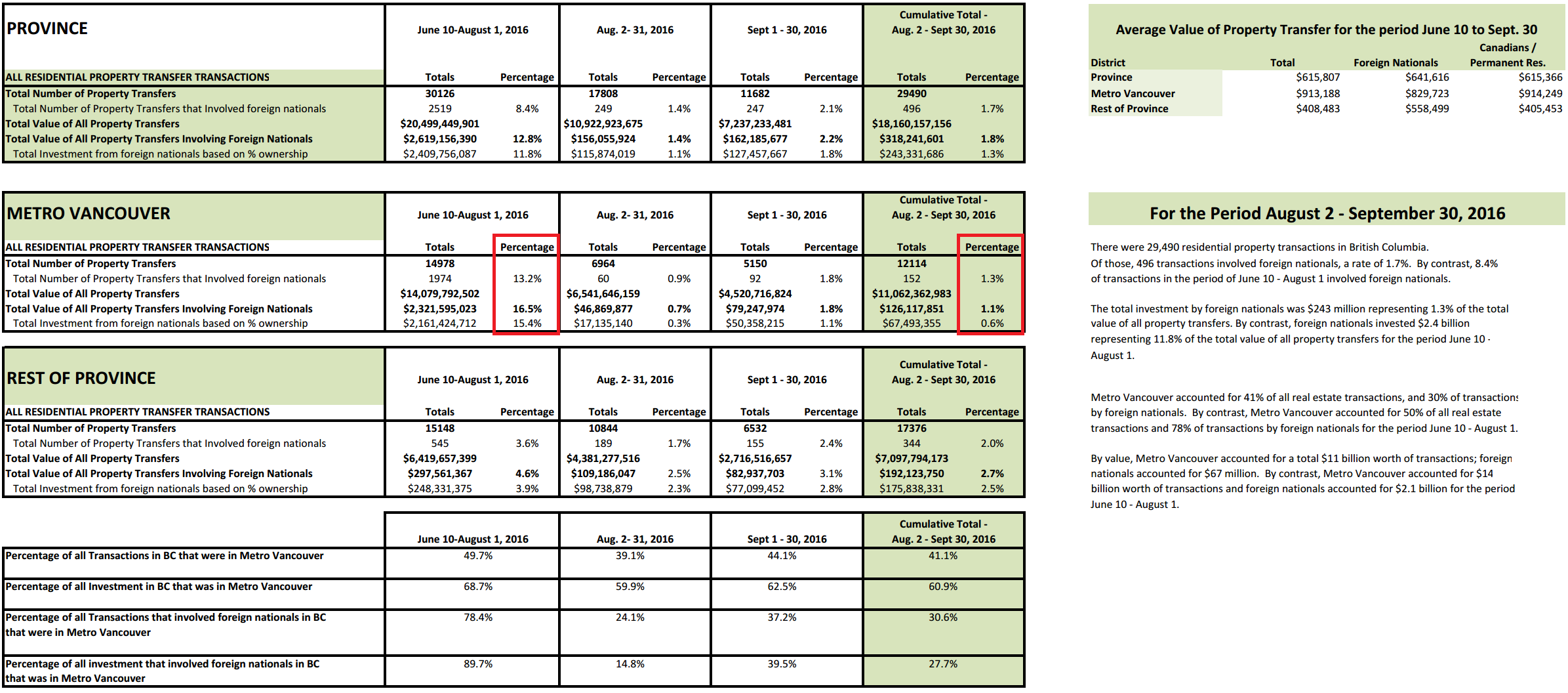

Foreign purchasers were involved in 1.8% of the 5,150 residential property transfers in Metro Vancouver in September, accounting for 1.8% of the total value of properties transferred in that period, according to the latest real estate transaction data released by the Province today.

Since the additional property transfer tax was introduced Aug. 2, 2016, the rate of foreign investment in residential real estate in Metro Vancouver was 1.3% of the total 12,114 transactions – a rate more consistent with the provincial average during that period of 1.7%.

Provincewide, there were 29,000 residential real estate transfers worth $18 billion from Aug. 2 to Sept. 30, the period after the additional property transfer tax was introduced. The total value of transfers involving foreign buyers was $318 million, or 1.8%. A number of cases involve foreign buyers purchasing a percentage of a property and a Canadian citizen or permanent resident purchasing the other portion of the property. The value of property purchased by foreign buyers based on percentage ownership was $243 million.

From June 10 to Aug. 1, the period before the additional tax took effect, foreign purchasers were involved in 13.2% of residential property transfers in Metro Vancouver, compared to 3.6% in the rest of the province. However, it is unclear how many transactions that would have occurred in August or September were completed in July, prior to the tax taking effect. Data from the coming months will provide a more accurate picture of how the market is changing with the additional property transfer tax in place.

Since the additional tax was introduced, government received 166 additional property transfer tax returns, totalling $10.1 million in additional property transfer tax paid. As part of the review and compliance process, auditors have sent 150 letters requesting more information from transferees who indicated they are Canadian citizens or permanent residents, to verify their citizenship or permanent residency status. Of the 150 letters, 85 audit files have been opened to investigate if the additional tax should have been paid.

In the Capital Regional District, foreign buyers represented 3.5% of the residential real estate market from Aug. 2 to Sept. 30. In the period prior to the tax`s introduction (June 10-Aug. 1), foreign buyers accounted for 3.9% of all transactions. More detailed information on Vancouver, Richmond, Burnaby and Surrey is also available. Other communities have not been detailed at this time.

The Province continues to take significant action on housing affordability to ensure that British Columbia families can afford to purchase a home in their community, or rent if they are in a position to do so. Measures announced to date include:

Newly built homes exemption, which has helped more than 6,300 families save an average of $7,500 in property transfer tax on their newly built homes.

Commitment of $500 million to fund an additional 2,900 affordable rental units, building on the Budget 2016 commitment of $355 million to create 2,000 additional new units of affordable rental housing throughout British Columbia.

New luxury tax on properties that sell for more than $2 million.

Strengthened consumer protection in B.C.’s real estate market by replacing the Real Estate Council of British Columbia with government appointed, public-interest members.

Significantly expanded the authority of the Superintendent of Real Estate.

Enabled the City of Vancouver to implement a vacancy tax.

Further measures that support the Premier’s six principles of housing affordability will be announced in the coming weeks. The six principles are:

Ensuring the dream of home ownership remains within reach of the middle class

Increasing housing supply

Transit expansion

Supporting first-time home buyers

Ensuring consumer protection

Increasing rental supply

The two red boxes are before and after the implementation of the foreign buyers tax. Congratulations Vancouver.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.