The higher world interest forecasters are back on track and, even more importantly for Australia, BHP is back in favour among the institutions.

Traditionally, the Big Australian has been the corner stone of many share portfolios and the graph below should make Australian investors feel good.

But with the Putin oil plan on schedule and the Saudi’s ending their campaign to drive down the price, we are seeing a further lift in the price of oil.

…BHP has reduced drilling costs in its US onshore shale business by 40 per cent over two years. This means that more of its US shale oil can be produced economically at current prices, although it does plan to increase on shore production, BHP’s shale oil needs the oil price to rise to $US60-plus a barrel.

…It’s like the old days.

I wrote in August:

BHP’s result was clearly awful with the small sweetner of cost control overwhelmed by the fallout from bad investments, bad commodity prices and bad luck. The future also looked lousy with the outlooks for most products gloomy, the exception being oil in the longer run. I would not buy it with someone else’s money.

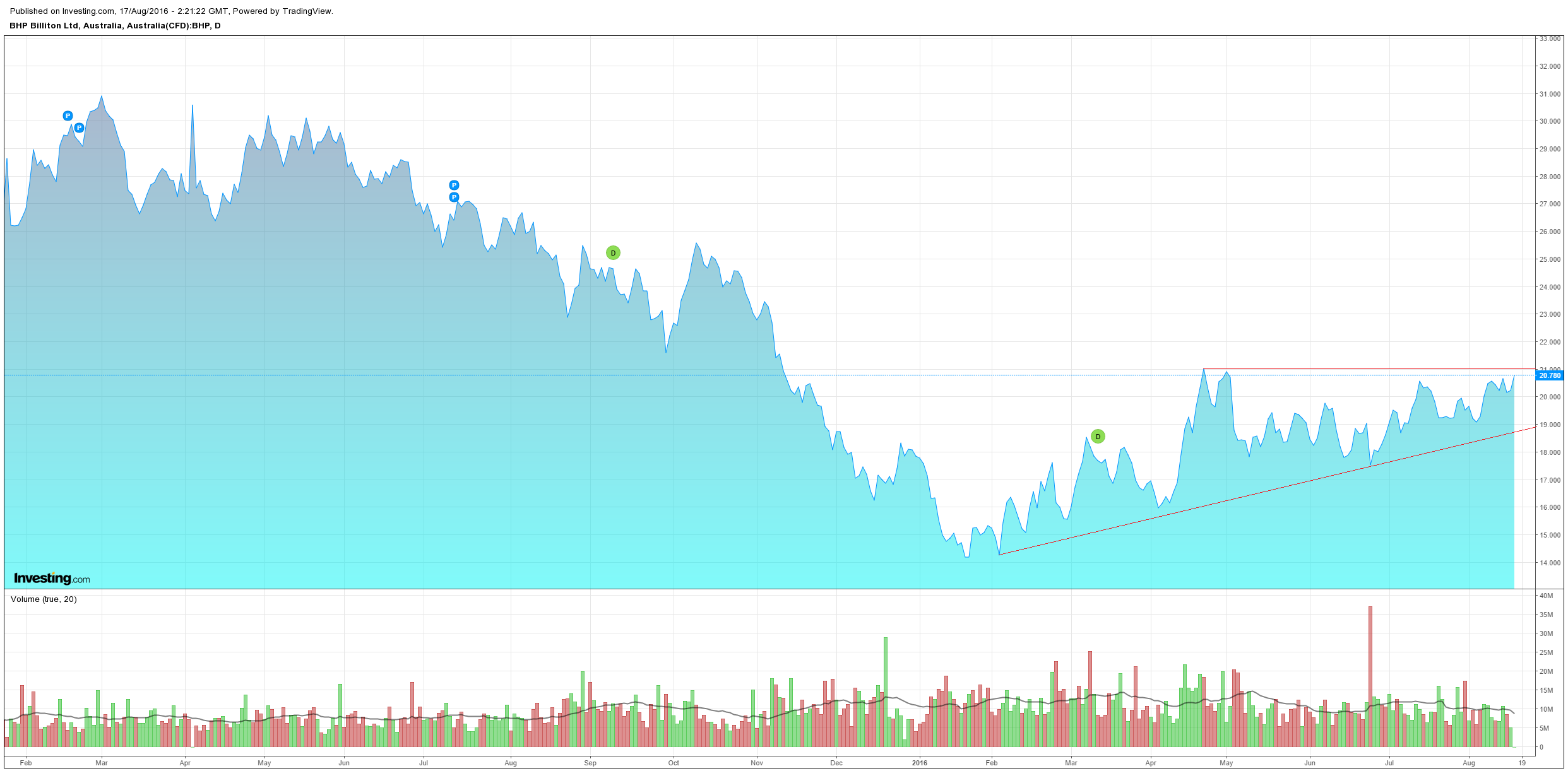

So, why do I say it’s on the verge of a positive re-rating? One reason is the chart which is threatening to break out of a bullish ascending triangle pattern:

The second reason is it’s exposure to coking coal and oil. The first of these is really on a tear and unlike iron ore looks like it has legs for another few quarters. I don’t rate the oil exposure but I’m more bearish than the market on black gold so that is also a positive for the instos.

The last reason is the most important. One must always recall that instos live and die on relative performance. By mandate they need to be deployed in equities and often their allocations are mandated by sector. If you are forced to buy miners at this juncture would you prefer BHP’s mix of iron ore, copper, oil and coking coal to the iron pure plays of RIO and FMG? Yes, you would. So, I expect we’ll see a raft of upgrades to the stock so that fundies can lose less than they would in other miners and take home their fat bonuses.

Stupid, yes, but there you have it.

Last week I noted that if BHP gets it on with the oil price then it will emerge as an interesting short. There are three reasons why. First, iron ore is in the gun:

Advertisement

China is tightening fast on property;

50mt of new supply is coming in H1 2017;

Chinese inventories of steel and iron ore are good;

seasonal weakness approaches then we’ll see a rebound before a poor 2017.

Second, coking coal is going to flame out:

China has moved to pop the coking coal bubble by releasing some blocked local supply;

US supply is rebounding into the price spike;

as iron ore demand fades so too will coking coal;

current pressures are all about Chinese restocking which should peak by Q1 ’17;

by mid-year I expect the price will have almost halved.

Third, there is no OPEC deal:

Advertisement

oil is charging for now on hot air;

but, if Libya, Nigeria and Iraq return with US shale stabilising, the OPEC deal cuts 0.2-0.7mmb/d while supply expands 2mmb/d;

the cut is still 50/50 whether it comes at all and Russia is not going to rush to join it unless it sees proof that OPEC members are sticking to it (which they probably won’t);

BHP production is not going to rebound at Eagle Ford until oil breaches $60;

oil has as much downside risk at $53 as it does upside.

Then there is the US dollar bull market weighing upon it all.

Whether BHP has further to run first I can’t say but with Gotti piling in that’s a decent contrarian indicator too. The key as usual is probably the Fed. If you think it is going to hike in December than BHP isn’t going to get far from today. If not then it has further room to run. There is also the issue of its (minority) coal contracts which will extend earnings upside for a little longer.

Having said that, if I were looking for shorts in the big miners today, I’d prefer FMG and RIO with their more pure play iron ore exposure.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.