S&P Global Ratings today said that it has revised its outlooks on the long-term ratings on 25 financial institutions operating in Australia to negative from stable. At the same time, we have revised our outlooks on three financial institutions to developing from positive (see ratings list below).

The rating actions reflect S&P Global Ratings’ view that the trend in economic risks facing financial institutions operating in Australia has become negative (see our BICRA snapshot, below). Strong growth in private sector debt (to about 139% of GDP in June 2016 from 118% in 2012, or an annual average increase of 5.2 percentage points) coupled with an increase in property prices nationally (average inflation-adjusted increase for the past four years was 5.3% nationally) are driving the potential increase in imbalances in the economy, in our view. Consequently, we believe the risks of a sharp correction in property prices could increase and if that were to occur, credit losses incurred by all financial institutions operating in Australia are likely to be significantly greater; with about two-thirds of banks’ lending assets secured by residential home loans–the impact of such a scenario on financial institutions would be amplified by the Australian economy’s external weaknesses, in particular its persistent current account deficits and high level of external debt.

Notwithstanding the growing imbalances in recent years, in our base case we consider that the growth in private sector debt and property prices will moderate and remain relatively low in the next two years. We believe that

increasing apartment supply in Sydney and Melbourne, regulatory pressures on lending practices and capital, and recent trends (including declining sales volumes in the secondary market) should help moderate the growth in property prices and household debt. Nevertheless, in our alternative case, we consider that there is a one-in-three chance that the strong growth trend will resume within the next year, because in our view several other important factors that have supported the past trend are likely to persist, including low interest rates, a relatively benign economic outlook, and an imbalance between housing demand and supply; in addition, Australian banks could possibly target higher lending volumes to offset pressures on their earnings growth. We would see a resumption or continuation of this trend as indicative of a continued buildup of economic imbalances, posing greater risks to all financial institutions operating in Australia.

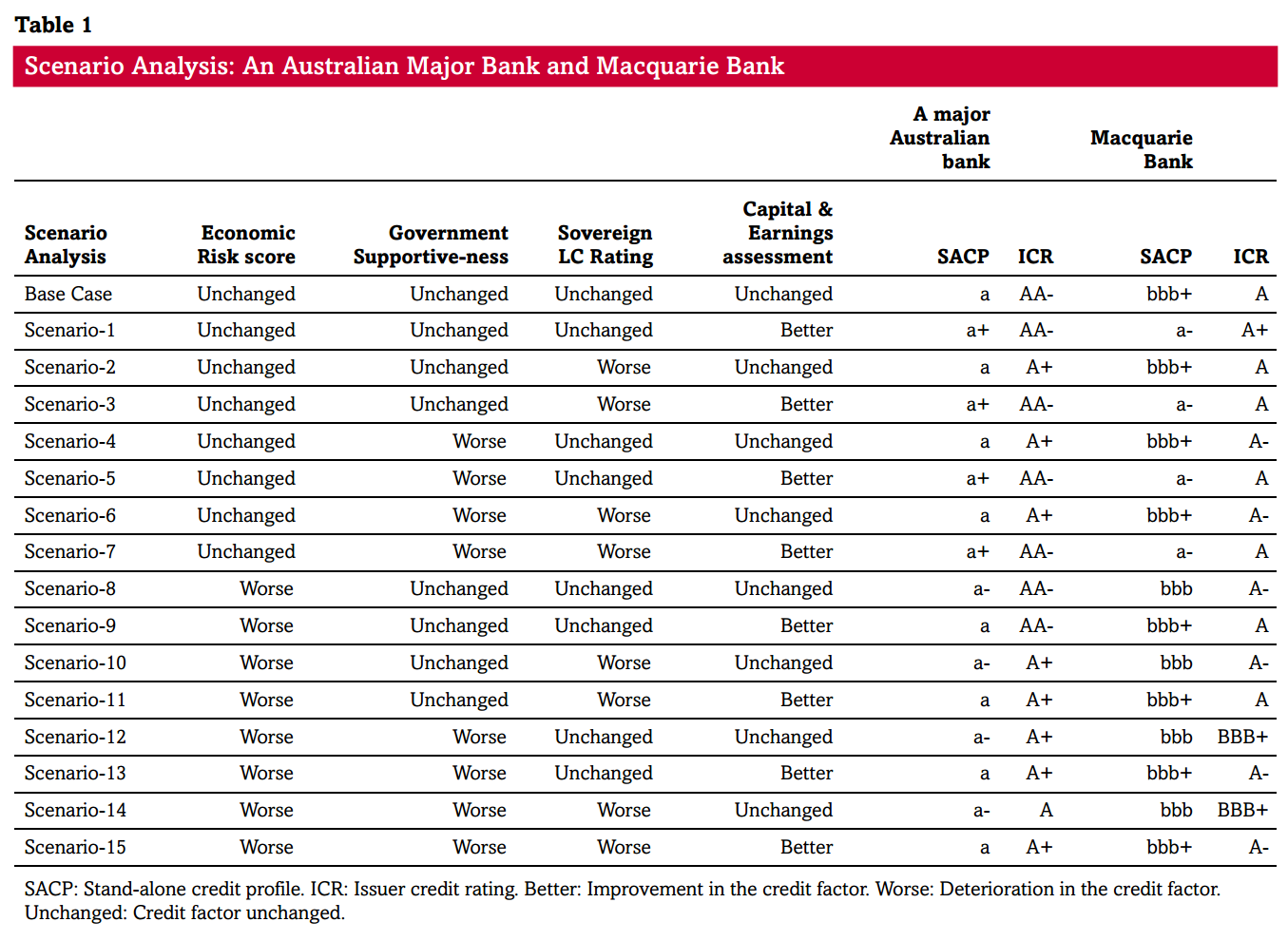

Consequently, should our alterative scenario materialize (that is, if imbalances continue to build), we would expect to lower our stand-alone credit profiles (SACPs) and ratings on most of the financial institutions that have

ratings on negative outlooks. Lower SACPs would also generally lead to lower ratings on hybrids and nondeferrable subordinated debt instruments issued by these banks.

Notwithstanding the rising economic imbalances, we believe that Australia remains among the lower risk banking systems globally. We consider that the financial institutions operating in the country benefit from a resilient economy, relatively benign economic outlook by global standards, conservative risk appetite and governance, and conservative prudential regulation. Partly offsetting these strengths are the Australian banking system’s material reliance on offshore borrowing, high and rising economic imbalances, and increasing private sector indebtedness.

Is S&P Global Ratings predicting a crash in property prices in Australia?

We consider that a sharp fall in property prices remains unlikely in the next two years, and such a scenario is only a stress-case scenario, in our opinion. In addition, notwithstanding our view of a trend of rising economic imbalances in Australia, in our base case we consider these imbalances will unwind in an orderly manner, as has generally been the case over past property cycles. In line with recent trends, we expect that the growth in private sector debt and property prices will moderate and remain at a relatively low level in the next two years. We believe that increasing apartment supply in Sydney and Melbourne, regulatory pressures on lending practices and capital, and recent trends–including declining sales volumes in the secondary market–should help moderate the growth in property prices and household debt. Nevertheless, in our alternative case, we consider that there is a one-in-three chance that the strong growth trend will resume. In our opinion, the likely low interest rate environment, continued demand supply gap for housing in Melbourne and Sydney, a relatively benign economic outlook, and Australian banks possibly targeting higher lending volumes (to offset pressures on their earnings growth) could stimulate a continued buildup of the imbalances in the economy.

How would a continued buildup of imbalances affect the creditworthiness of Australian financial institutions?

We consider that other things being equal, a rapid rise in property prices or strong growth in private sector debt generally signals a higher risk that a sharp correction in property prices could occur. In that event, credit losses incurred by all financial institutions operating in Australia would be significantly greater. We believe that in a scenario of rapidly falling house prices, all the Australian financial institutions would be exposed to a drop in operating earnings and a rise in credit losses significantly beyond a level factored in our current ratings. A sharp decline in house prices in any country is generally accompanied by a weakening of other key macroeconomic factors, such as unemployment, household expenditure, corporate investments, and total economic activity.

In Australia’s case, its external weaknesses could amplify the impact. We expect that the cost of external borrowings would rise, domestic credit conditions would tighten, the currency may depreciate sharply (damaging confidence and potentially limiting monetary policy flexibility), and economic growth would slow. This would ultimately result in lower income levels. In such a scenario, financial stresses would be widespread across the country, including the corporate, small-to-midsize enterprises, and household sectors. We believe that this would significantly increase defaults by borrowers and losses on such defaults. In addition, there would be substantially fewer opportunities for profitable lending by financial institutions.

How would the increased risks in your alternative scenario (of continued strong growth in private debt and property prices) affect your assessment of ratings on financial institution?

In our opinion, other things being equal, increased risks in a country are generally likely to pressure all banks and similar financial institutions in that country that take deposits, extend credit, or engage in both activities. These institutions include mortgage lenders, credit unions, building societies, and finance companies. If a buildup of economic imbalances were to continue–fueled by strong growth in property prices and private sector credit–we expect to lower the stand-alone credit profiles (SACPs) of all the Australian financial institutions by at least one notch. Our SACPs on some financial institutions may come under additional pressure because of their potentially weaker capital under such a scenario. This is because to reflect greater economic risks, we would increase the risk weights in our capital analysis that would be applicable for the financial institutions’ credit exposures. Consequently, other things being equal, we would expect forecast capital ratios (under our Bank Capital Methodology) would drop for a financial institution if it is facing higher economic risks.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.