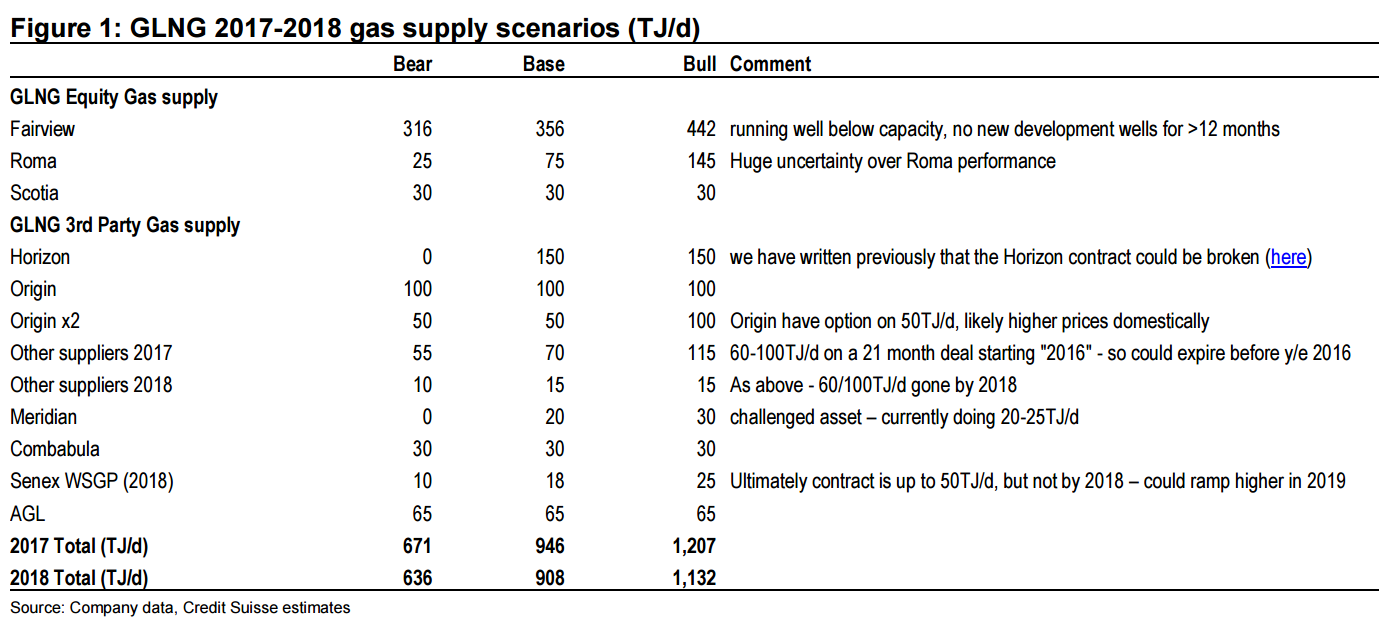

Life as an E&P analyst is supposed to get a bit easier, from a modelling perspective at least, once an LNG project hits first gas. For a conventional project 90-95% of the capex is spent to get to first gas, contracts are 100% reserve covered and opex is relatively low and visible. Our undoubted panache for getting the oil price wrong should be the greatest error in our models. As we continue to learn by the day, the same cannot be said about CSM-LNG projects. Sadly, nowhere is this more true than at GLNG. With Fairview running at ~80% of compression capacity (and with no development wells drilled for >12 months one has to ask how long these levels will be maintained without materially more capital invested), Roma issues now well publicised by Santos at Raslie (not to mention data showing Roma doing little more than 25TJ/d for most of this year), variability on some of the third-party supply volumes and our long held published view (here) that the Horizon contract is unsustainable long term from both an economic and reserve perspective, it is impossible to have any true certainty in GLNG modelling.

To that extent, we have introduced a risk weighted scenario of what we see as bear, base and bull scenarios for the volumes that GLNG is able to run through the plant. With no guidance from Santos at this stage, and the fact that the contracts are 100% take or pay (our modelled financials actually still assume the plant runs above contracted volumes longer-term at 7.5mtpa) we believe it would be impossible for anyone to confidently model a more definitive scenario. So whilst we are implicitly suggesting there is material downside risk to our financials, with no firmer guidance (be it in terms of future cost to try and run at 7.2mtpa or more or on reduced LNG offtake volumes), there can be no science behind any numbers claimed to be defendable.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.