BUSINESS CONFIDENCE HOLDS UP. CONDITIONS REMAIN ABOVE AVERAGE, BUT LOST MOMENTUM

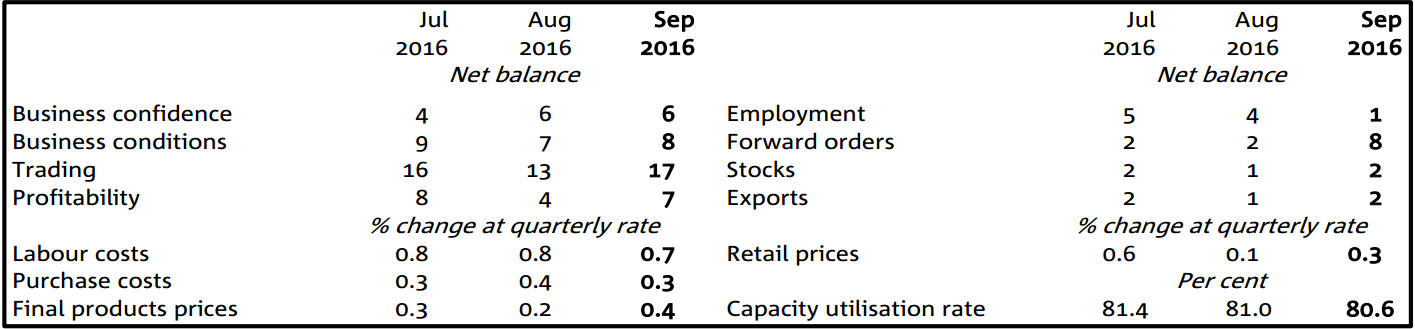

The September NAB Monthly Business Survey is still consistent with reasonable performance of the non-mining economy, although momentum has eased from earlier in the year. The business confidence index was steady at +6 index points in September. Meanwhile, business conditions (an aggregation of trading conditions (sales), profitability and employment) rose modestly in September, to +8 index points (from +7), although it has eased in trend terms.

According to Mr Oster, NAB’s Chief Economist, “there was no hint that the RBA’s interest rate cut in early August had any further material impact on confidence in September after seemingly providing some support in August, although the counterfactual is impossible to measure. Business confidence is in line with its long-run average and while we would like to see confidence at even higher levels as a precursor to stronger non-mining business investment, this is still a good outcome given numerous uncertainties facing business, especially from offshore.”

Business conditions picked up slightly in September, although have eased somewhat in trend terms. According to Mr Oster, “Business conditions have been consistently above their long-run average since early 2015, suggesting the recovery through the non-mining economy has become more entrenched. However, the strength in business conditions has once again become more heavily skewed towards major services industries after some promising signs of a broadbased recovery earlier in the year. We are also continuing to monitor negative trends in retail conditions, which deteriorated further in September – seemingly related to a jump in input costs.”

Within business conditions, trading conditions and profitability remain strong, while the employment index fell notably. “The re-weakening in employment conditions is disappointing, although employment conditions remain in marginally positive territory consistent with adequate employment growth”, said Mr Oster.

Meanwhile, the survey’s leading indicators continue to point to solid prospects in the very near-term. In particular, forward orders jumped notably and have been in positive territory for most of the year. However, NAB’s measure of capacity utilisation eased back below the long-run average in September. Mr Oster notes that “While survey indicators suggest a solid near-term economic outlook, we are watching the trend softening in capacity utilisation closely given our reservations about longer-term economic prospects. However, the softening in capacity utilisation is counter to the current strength in trading conditions and may possibly reflect elevated capital expenditure which could be adding to the level of capacity.” NAB’s capex indicator at +10 index points is more upbeat than other investment indicators.

“Overall, while we are somewhat cautious about the narrowing of the industry base underlying business conditions, results from the Survey remain reasonably consistent with our pre-existing views of the economy – as far as it relates to the near-term outlook”, said Mr Oster. “It suggests a multi-speed economy, but one where most key non-mining sectors are performing well in the near-term. However, weakening retail conditions are a significant risk to our outlook, especially considering that consumption accounts for more than 50% of Australian GDP. Beyond the near-term, we still expect the economy to slow into 2018 as momentum from commodity exports, housing construction and AUD depreciation is lost. Ongoing low inflation combined with a more subdued growth outlook is expected to jolt the RBA into action, cutting the cash rate by 25bp two more times in H2 2017.” NAB’s latest Australian economic forecasts will be available on Thursday.

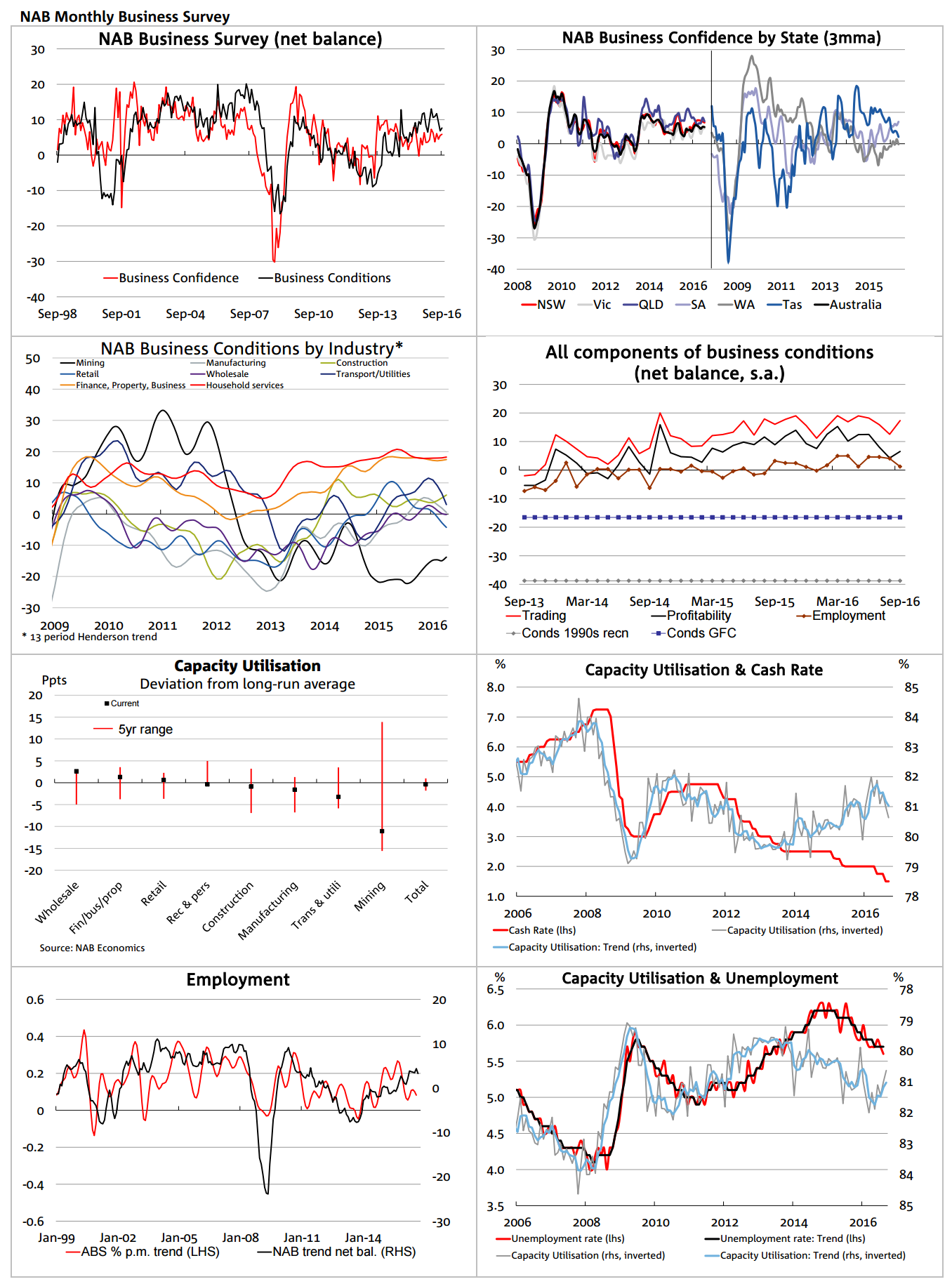

And the charts:

Note that those charts are trend so are not fully picking up the recent swoon in employment. The survey is bright in the lending, dwelling construction and services complex but like so many other indicators right now, hot and cold, shows a very unbalanced pattern of growth. It’s hard to characterise this economy but is sure ain’t strong.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.