Over the past few years, we have witnessed several parties call on the federal government to allow Australians to use their superannuation to purchase their home, including former Treasurer Joe Hockey, Senator Nick Xenophon, “high-rise” Harry Triguboff, and even the Committee for Economic Development Australia (CEDA).

In late September, News.com.au published an “exclusive” whereby it claimed that the Australian Taxation Office (ATO) had loosened rules to allow parents to use their superannuation savings to invest in a home to house their children, with the hope that the ATO would soon extend it to allow first home buyers (FHBs) to tap their super to purchase a home of their own:

According to advice provided by the ATO to DomaCom, a fractional property investment firm which allows people to buy units in a property in the same way as shares, SMSFs would not be in breach of the rules as long as the fund owned less than 50 per cent of the property.

“Basically what it means is that for the first time, a parent can use their super fund to invest in a property with their son or daughter, and the son or daughter can then rent it,” DomaCom chief executive Arthur Naoumidis said.

Mr Naoumidis says it’s the “first step” towards DomaCom’s ultimate goal of allowing young people to tap into their super to buy their first home..

Unlike the Canadian model, for example, where money is released from the pension to help people acquire their first property, “this Australian innovation keeps the asset within the superannuation environment”, he said.

Robert Coyte, chief executive of financial planning firm Shartru Wealth, said the ATO ruling would effectively allow parents to use their super balances to “put their foot on a property” for their kids without parting with a huge chunk of cash upfront.

In the wake of this article, the ATO has released a clarifying statement strongly rebuking suggestions that it has loosened super rules to allow the purchase of property to live in, nor does it intend to:

“The ATO does not condone and will take serious action with respect to any promotion of SMSF investments as a means for providing present day benefits for members, their relatives or other related parties. This includes the provision of residential accommodation to related parties such as children of SMSF members.

“Contrary to statements made in the media, the ATO is not considering allowing broader use of SMSF assets beyond the sole purpose of providing retirement benefits for members or benefits for their dependants upon death,” says Ms Macfarlane.

“Ensuring SMSFs are established and maintained for the sole purpose of providing retirement benefits for members and benefits to their dependants on death, as well as ensuring compliance with the regulatory requirements and restrictions that apply to SMSFs, is paramount to the ATO’s role as the regulator of SMSFs.

“The use of SMSF property investments as a means of providing residential accommodation to SMSF members’ children and other related parties contravenes the requirement that an SMSF be established and maintained for the sole purpose of providing retirement benefits for members or benefits for their dependants upon death.

“The use of any SMSF investment as a means for providing a present day benefit for members also directly contravenes other superannuation regulatory rules and restrictions that apply to SMSF investments.”

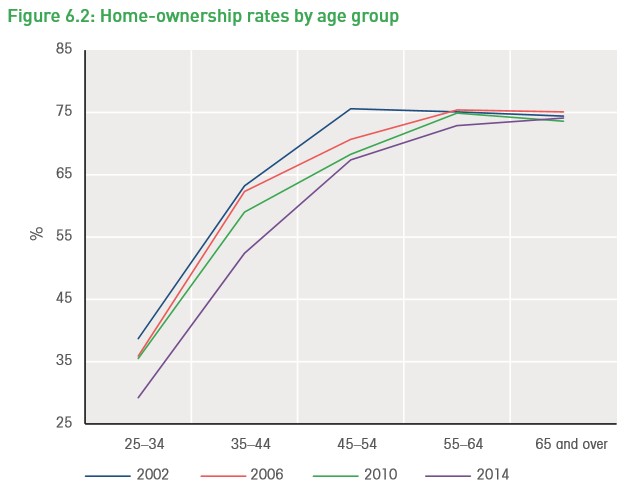

Past experience has shown us unequivocally that demand-side measures aimed at promoting “housing affordability” and home ownership do not work. Despite the massive decline in interest rates and the myriad of subsidies provided to home buyers over the years, the home ownership rate has decreased, particularly for younger Australians (see next chart).

Allowing buyers to access super savings for housing would simply increase their capacity to pay and would soon be capitalised into higher home prices. At the same time, Australian’s retirement savings would be compromised for little additional benefit, potentially placing further strain on the Aged Pension.

Canada’s Garth Turner, who oversaw the introduction of a housing-super system in Canada in the 1990s, has admitted that it was a massive mistake, placing further upward pressure on Canadian house prices and putting at risk retirement savings.

The problem of unaffordable housing requires a combination of policy measures that tackles: tax lurks (including both negative gearing and the CGT discount); supply-side constraints; infrastructure bottlenecks; money laundering into, and foreign buying of, established dwellings; loose capital rules; over-investment by super funds; and excessive levels of immigration.