Fresh from the AEMO’s investigation into the SA blackout:

Pre-event

The market was operating normally prior to the event. AEMO’s assessment concluded that, based on forecast conditions for Wednesday 28 September 2016, there was insufficient justification for reclassification for the loss of multiple transmission lines or generating units.

The forecast severe weather was assessed as increasing the risk to power system failure due to lightning, however, as there are no transmission lines in SA classified as ‘vulnerable’, this did not warrant a reclassification of transmission lines.

Wind speed forecasts were up to 120 km/h, which SA transmission assets are designed to withstand (1 Information provided to AEMO indicates that damaged transmission lines were subjected to actual wind speeds that were much higher than forecast.)

Event

It is now known that five system faults occurred within a period of 88 seconds on 28 September 2016. These system faults lead to six voltage disturbances.

The five synchronous thermal generators operating at the time of the event remained connected and operated up until the SA system disconnected from the rest of the National Electricity Market (NEM). The operation of these generators was not materially impacted by the system faults experienced during this event.

Investigations now show that there was a total sustained reduction of 445 MW of wind generation across nine wind farms, plus further transient reductions of 39 MW in each ride-through event. The transient reduction in output was spread across all wind farms online at the time, including those that did not suffer a sustained reduction in output. This information replaces the data (315 MW lost from six wind farms) in the Preliminary Report.

The sudden loss of 445 MW of generation increased flows on the Heywood Interconnector. The Heywood Interconnector’s automatic protection mechanism operated and disconnected to avoid damage to the interconnector and other transmission network infrastructure in both SA and Victoria.

The Murraylink interconnector remained connected up until the SA system disconnected, and its operation was not materially impacted by the six voltage disturbances experienced. The design and nature of this direct current link means that it does not respond to the generation shortfall nor provide frequency control or inertia into SA.

The instantaneous loss of 900 MW of supply across the Heywood Interconnector could not be met by the generators remaining online within SA. The sudden and large deficit of supply caused the system frequency to collapse more quickly than the Under-Frequency Load Shedding (UFLS) scheme was able to act, resulting in the SA region Black System.

Nine of the 13 wind farms online did not ride through the six voltage disturbances experienced during the event. In the days following, AEMO identified this issue and reclassified the simultaneous trip of these wind farms as a credible contingency.

AEMO then worked with each of the operators of these wind farms and determined that their ‘voltage ride-through’ settings were set to disconnect or reduce turbine output when between three and six ‘voltage ride-through’ events were detected within a given timeframe. Investigations to date indicate that information on the control system involved and its settings was not included in the models of wind turbine operation provided to AEMO during NEM registration processes prior to connection of the wind farms.

The wind farm operators and the turbine manufacturers are working to propose improved ‘voltage ride-through’ settings for consideration by AEMO. As they are re-configured, the wind farms are removed from the reclassification and returned to normal operation. At the time of this report, five of the wind farms that suffered sustained output reductions in the event have been removed from the reclassification.

In short, a bloody great storm exceeded wind turbine tolerances. Hardly cause for national bodice-ripping.

What is needed now is a calm debate about how to stabilise renewable base load power to secure against such rare outcomes. Professor Ross Garnaut (who is also chairman of Zen Energy) recently kicked it off:

High penetration of intermittent renewables introduces high variability in wholesale prices, and the potential for destabilising variation in systemic frequency and voltage. The maintenance of systemic stability requires countervailing variations in volumes of wholesale power supply, and new sources of frequency control and ancillary services (FCAS).

Let me focus at first on the wholesale power market.

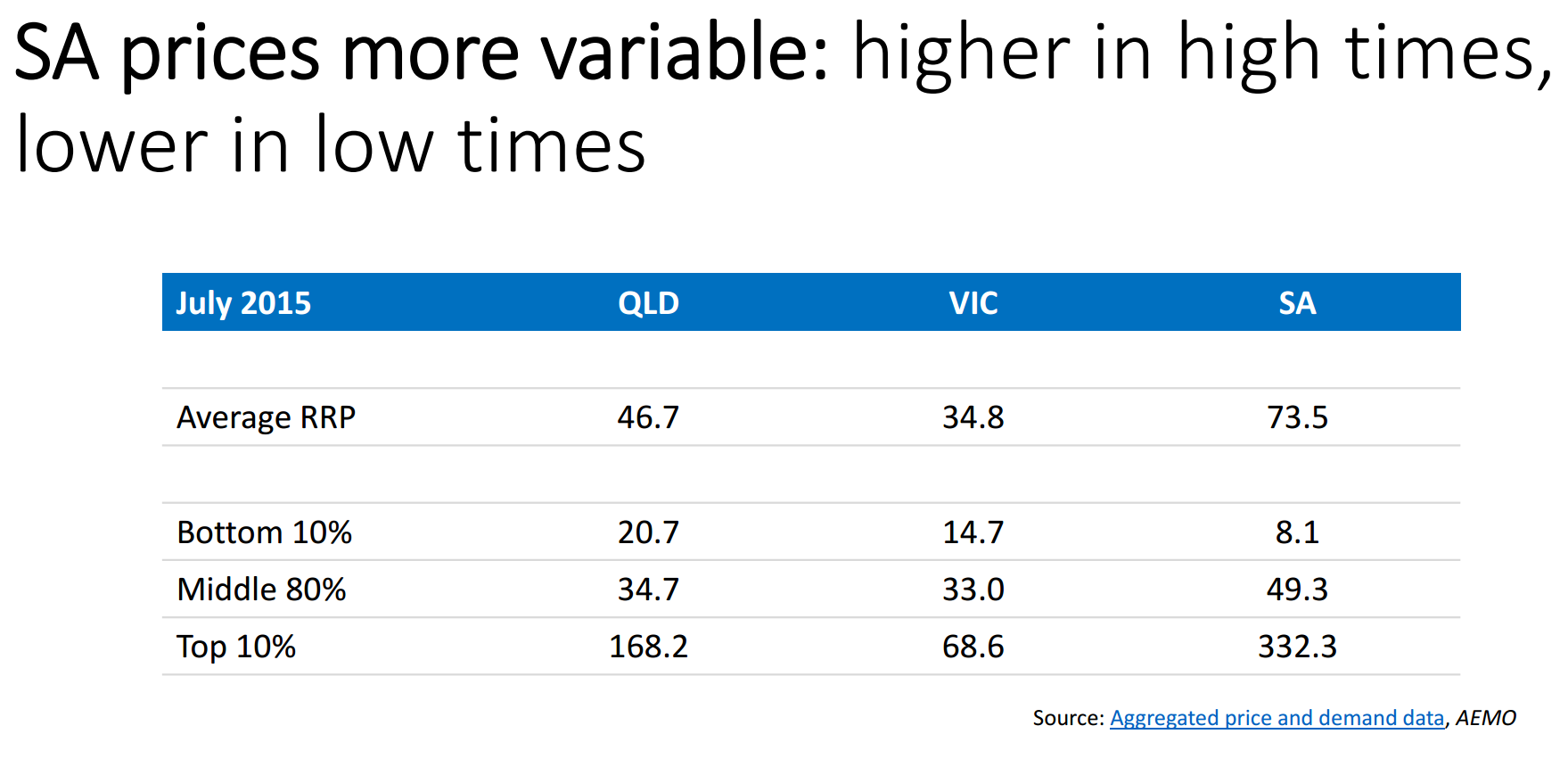

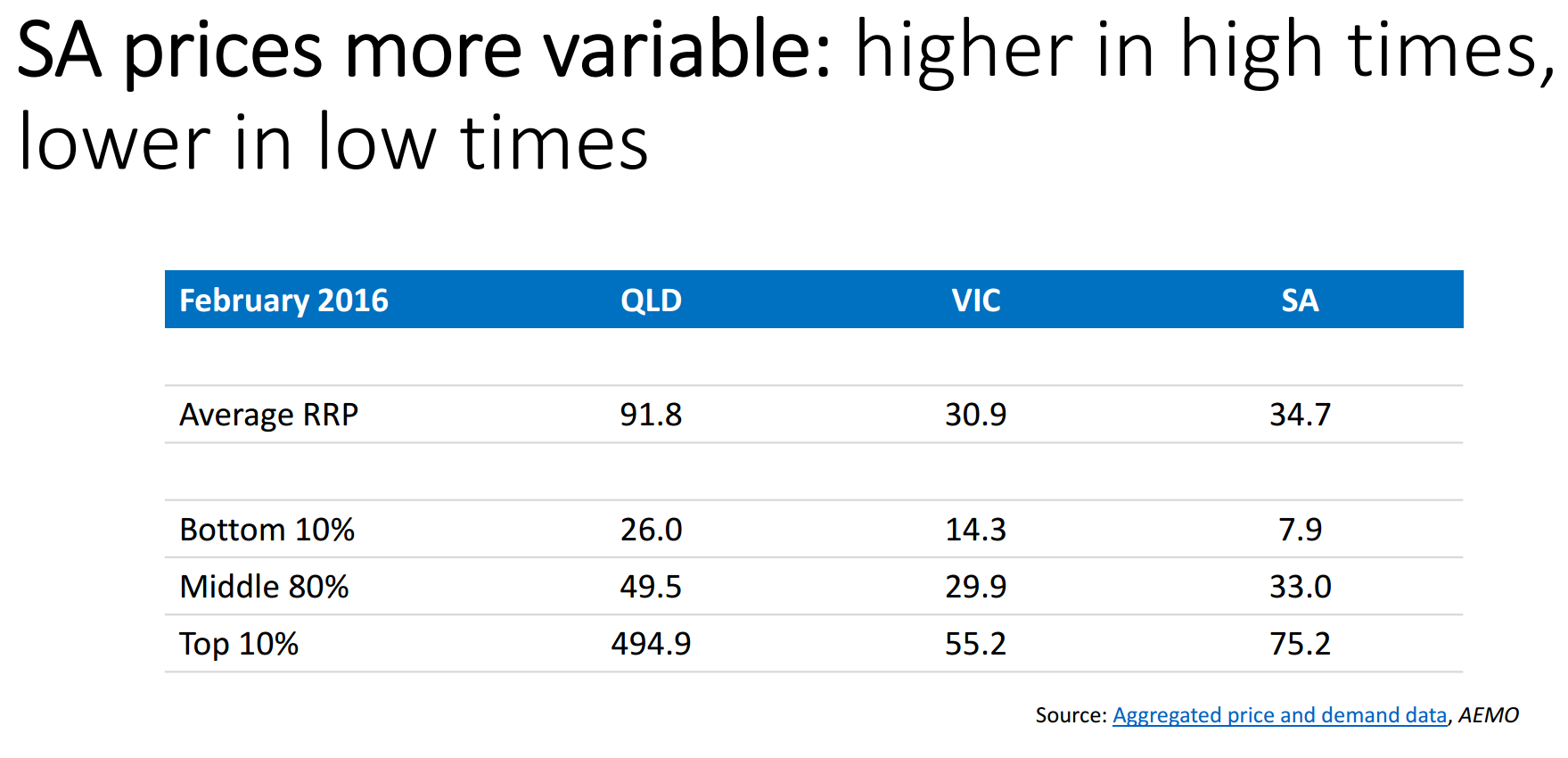

High penetration of renewables leads to low wholesale power prices at times when renewable energy is able to meet local demand, and high prices when the market has to be balanced by gas peaking power. Charts 4,5 and 6 illustrate the point with data from three months in last financial year—months for which I had taken out data for other purposes, and not selected deliberately for this presentation. In July, December and February of last financial year, the times of lowest wholesale prices each day—typically the early hours of the morning—revealed substantially lower wholesale prices in South Australia than in the two states with the lowest cost thermal coal resources—Victoria and Queensland. These were times when wind, supported by solar power in daytime hours, largely met requirements. The times of highest wholesale prices each day—typically the morning and evening peaks when gas provided the incremental supply to meet higher demand— prices were highest in South Australia. Queensland had even higher high prices in February 2016, as demand was lifted by commissioning of new LNG capacity. In the intermediate hours, prices tended to be a bit lower in Victoria than the other States, but not wildly different.

The expansion of intermittent energy supply in South Australia will tend to increase the number of hours each day with very low prices. The challenge is how to reduce prices at times when demand is strong and intermittent energy supply weak. Price volatility is not a problem in itself. Volatility provides the incentive to reduce demand, or to invest in new sources of electricity generation that produce power when prices are highest, or for investment in storage. Volatility provides the signal that increased transmission capacity may be warranted and should be considered alongside other means of balancing intermittency. Large users of power have opportunities to hedge against price uncertainty, and retailers can hedge to insulate their customers from variable prices.

The main sources of countervailing variation are demand management, storage, gas peaking generation, long‐distance transmission, and diversity in renewable energy supply. Each has its strengths and limitations. Each has an important role to play through the transition to a low carbon economy. Demand management, co‐generation from industrial processes, storage, long distance transmission and renewables diversity all have important roles in the zero carbon economy of the future. Whether or not gas peaking has a role after the transition depends on the availability of commercially viable sequestration of carbon dioxide wastes from gas combustion.

The challenge of policy is to allow and to facilitate good use of all means of balancing intermittent energy, and to ensure that reliance is placed on the most cost‐effective of them in particular circumstances. Exclusive emphasis on only one or two of them alone will greatly increase the cost of the balancing.

Efficiently operating markets embodying a carbon price in some form—perhaps the baseline and credit scheme favoured in the recent Climate Change Authority report—can sort out the economically efficient contributions of alternative forms of generation and storage in wholesale power supply.

The wholesale power market currently contains distortions that block efficient use of new storage technologies. The most damaging of these distortions is the averaging of settlement prices over 5 minute periods. Suppliers and users of wholesale power bid into the market each 5 minutes. However, contracts between buyers and sellers are settled by averaging prices over half hour periods. This dulls incentives to expand output in short periods of exceptionally low supply, and to reduce them in short periods of high supply. The importance of this distortion is demonstrated by experience through July 2016, when average South Australian prices were exceptionally high. A large part of the exceptionally high average prices came from less than 40 five minute periods when prices were at or close to the regulated maximum of $14,000 per MWH. Some of these high price episodes occurred within the same half hour as other 5 minute periods with negative prices down to the regulated limit of minus $1000. Battery systems, unlike thermal generators, respond fast enough to contribute to stabilisation by absorbing energy in one 5 minute period when prices are low and expanding wholesale supply in an adjacent 5 minute prices when prices are high. Averaging over 30 minute periods removes incentives for stabilising behaviour, and actually introduces incentives to destabilise the market.

ZEN Energy’s partner company in grid level battery storage and grid stabilisation, Greensmith, has installed more than one third of the large and rapidly growing battery storage capacity in the United States. This morning I asked its senior officers what contribution a battery storage system would have made to easing the recent power problems of South Australia. Greensmith’s assessment from reading public materials including the AEMO report is that the system‐wide problem is likely to have derived from variations in frequency, which batteries are particularly well placed to manage. It is not clear from the published material what caused the wind turbine trips. If later analysis suggests that the cause was systemic variation in frequency, then batteries would have provided the most cost‐ effective remedy. If the problems derived from local voltage issues, batteries located with wind farms could have avoided the problem. Once the system had tripped, and the challenge was to bring gas generators back into service as quickly as possible, a battery would have provided reliable and quick‐acting black start services. By contrast, both contracted black start providers failed to restart the South Australian system last week.

Other characteristics of Australian market regulation discourage use of decentralised battery storage that has the potential to contribute to evening out demand and supply of wholesale power, and also to reduce peak demand for network services.

While more efficient markets can help in the allocation of resources among types of power generation and storage, they cannot play this role in defining efficient allocation of resources between network expansion and new forms of generation and storage. Electricity distribution and transmission networks are natural monopolies that require planning decisions in the public interest. The Australian regulatory system is poorly designed for taking decisions on maintenance and expansion of the networks. Major reform is required. It is important to shift the initiative in putting forward proposals for investment in network maintenance and expansion in the hands of a public body charged with taking decisions in the national interest. That would remove the conflict of interest embedded in current arrangements. Such a body would be charged with assessments of whether investment in network maintenance and expansion is likely to yield higher returns than investment in decentralised generation and storage. To do its important job well, the energy planning agency would need to have deep professional capacities, and insulation from the day to day vicissitudes of partisan politics. The Australian Energy Market Operator could be strengthened to perform this planning role.

It is impossibly unlikely that such a planning process would have led to the $85 billion of investment in expansion of transmission and distribution capacity that Australia has seen over the past decade of mostly declining total demand for wholesale power through the network. At the same time, it may have led to greater investment in some forms of long distance transmission. Australia has made massive investment in its power networks over the past decade, which has been added with high margins to the bills of power users. Recent experience suggests that this massive expenditure has not purchased energy security.

Rational network design in contemporary circumstances would see evolution towards greater use of decentralised power, supported by a central transmission network designed to play a large role in balancing intermittent energy from different sources. It might not necessarily lead to reduced power flows through the grid. An efficient electricity system may see the electrification of transport gathering pace in the years ahead. An efficient system is more likely to see Australia’s advantages as a low‐cost producer of renewable energy reflected in expansion of energy‐intensive industries as the whole world shifts to greater reliance on renewable energy. These developments would mean an expansion of total power demand as the proportion of supply through the networks declined.

The new technology and economics of energy suggest that judicious application of local renewable energy supply technologies such as solar and battery storage can greatly reduce peak demand for power through the networks and therefore the costs of providing network services. At the same time, it can reduce vulnerability to disruption of networks from extreme weather events. The lights that stayed on in South Australia through last week’s blackout were in homes and businesses which had invested in local battery storage, and on Kangaroo Island where the anticipation of failure of the submarine cable had led to provision for decentralised back‐up generation.

Judicious investment in solar and wind generation, co‐generation from industrial processes supplemented by gas generation where adjacent pipelines make this feasible, demand management and battery storage, supported by efficient integration into established networks, can reduce power costs for users outside Adelaide below what is available from reliance on the grid alone. Decentralised provision of power also provides security against future disruption from extreme weather events.

There are gaps in current markets for Frequency Control Ancillary Services that have become more important and costly with the expansion of intermittent energy supply. Fast response stabilisation services are required. These are much more likely to be made available at low cost if thier supply is secured through introduction of new competitive markets, designed so that the new technologies can compete on a level playing field with incumbent thermal generators.

The costs and technological capability of battery storage has fallen to the point where it can contribute substantially to price stabilisation and grid stability alongside high and rising penetration of renewable energy. It can be introduced quickly. United States experience suggests the possibility of full deployment of grid level batteries within six months from commercial decisions to invest in them.

Pumped hydro‐electric facilities have longer lead times. Recent commercial research and development suggests that this form of storage will be able to play a major role in low‐cost balancing of intermittent electricity supply as eastern Australia moves towards much higher penetration of intermittent renewables.

Increased interconnection between South Australia and other States would not remove the requirement for investment in storage to stabilise wholesale prices and the grid. Long distance trade in renewable energy will reduce price volatility to some extent. However, the national expansion of renewable energy supply will make the balancing of intermittency as important to Australia as a whole as it is to South Australia now.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.