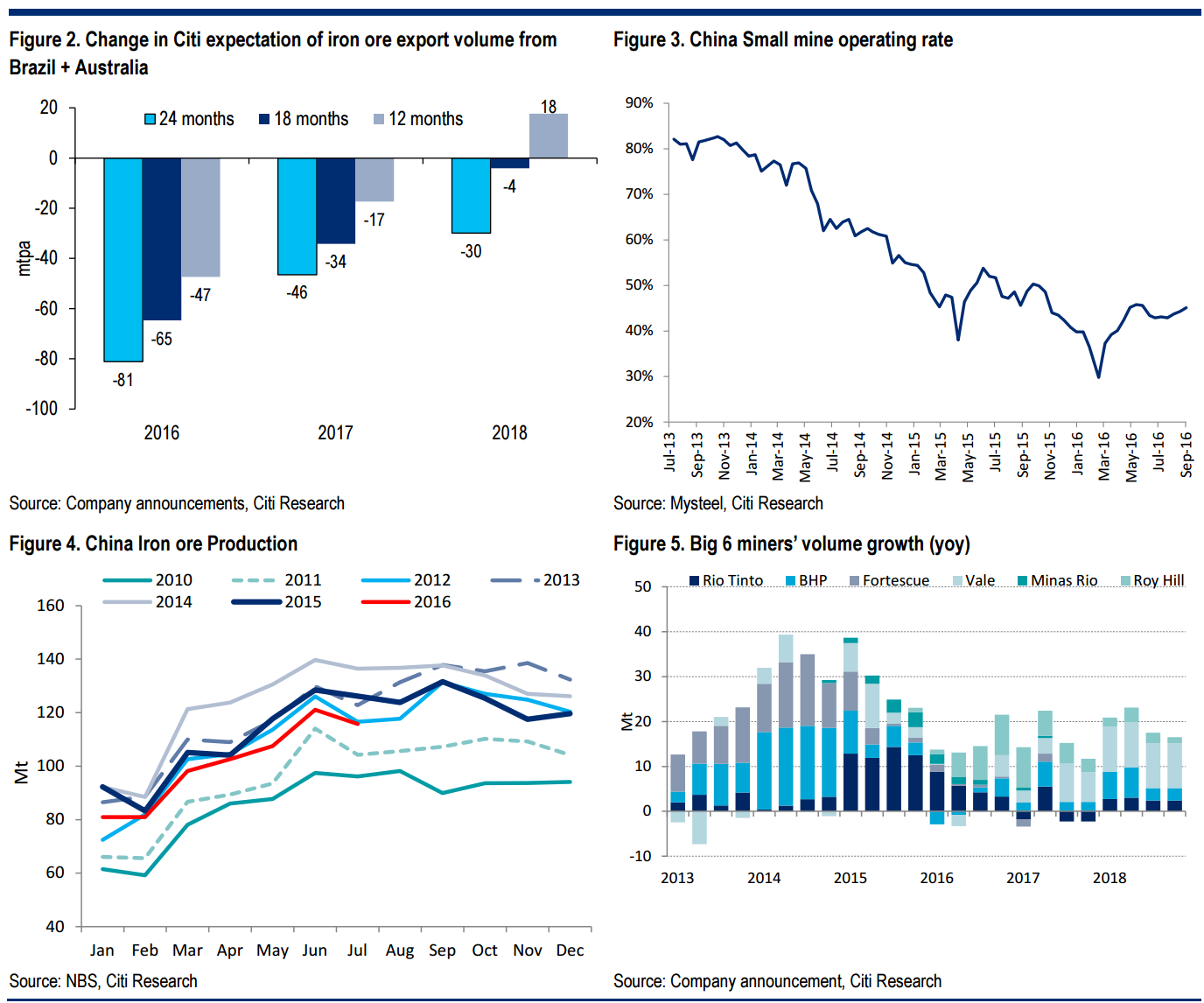

Supply growth slows due to delayed ramp up – Seaborne supply has lagged expectations due to logistical challenges and slower ramp ups. Comparing our seaborne volume growth expectations today versus 18 months ago we have reduced absolute supply by 65Mt in 2016 and 34 Mt in 2017. However, expected restart of Samarco and delayed ramp-ups have increased volume expectation for CY18 over the last 12 months by 18mt. (Figure 2). Rio Tinto’s expansion plans have been delayed due to ongoing issues with driverless train network. BHP has no immediate plan to add new projects in the seaborne market. Vale has toned town volume growth expectations with net capacity additions of 75mt to spread over 4 years (2016-20) instead of 3 years since our recent update. Outlook for restart of Samarco’s operations in 2017 continue to worsen. Volume ramp up from Roy Hill and Minas Rio remain largely on schedule. However, ramp up of Vale’s S11D project will help accelerate net supply growth from early 2017.

China domestic supply remain weak- Despite a strong rebound in spot prices, China’s domestic iron ore production has remained weak with crude ore output falling 2.2% yoy in 7M’16 according to NBS data (Figure 4). Capacity utilisations improved to late 2015 levels (Figure 3) but have limited upside due to marginally weaker demand for low-grade ore. Our back of the envelope calculation suggests that 150-200mt of low grade and high cost capacities have been eliminated. In addition, we do not foresee forced capping of domestic iron ore supply similar to what happened in coal industry, and support for loss making units could be minimal as China’s current supply control centers around steel rather than iron ore.

Supply from ‘others’ remain firm – Over the last 24 months seaborne volume expectations from Brazil and Australia have consistently declined (figure 2). A large part of it has come from exit of marginal capacities. However, the recent price spike has incentivized smaller miners in Africa, US and others to restart operations. Indian export volumes have hit monthly run rate of 2mt recently and restarted operations in Sierra Leone have hit annualized capacity of 5.5mt.

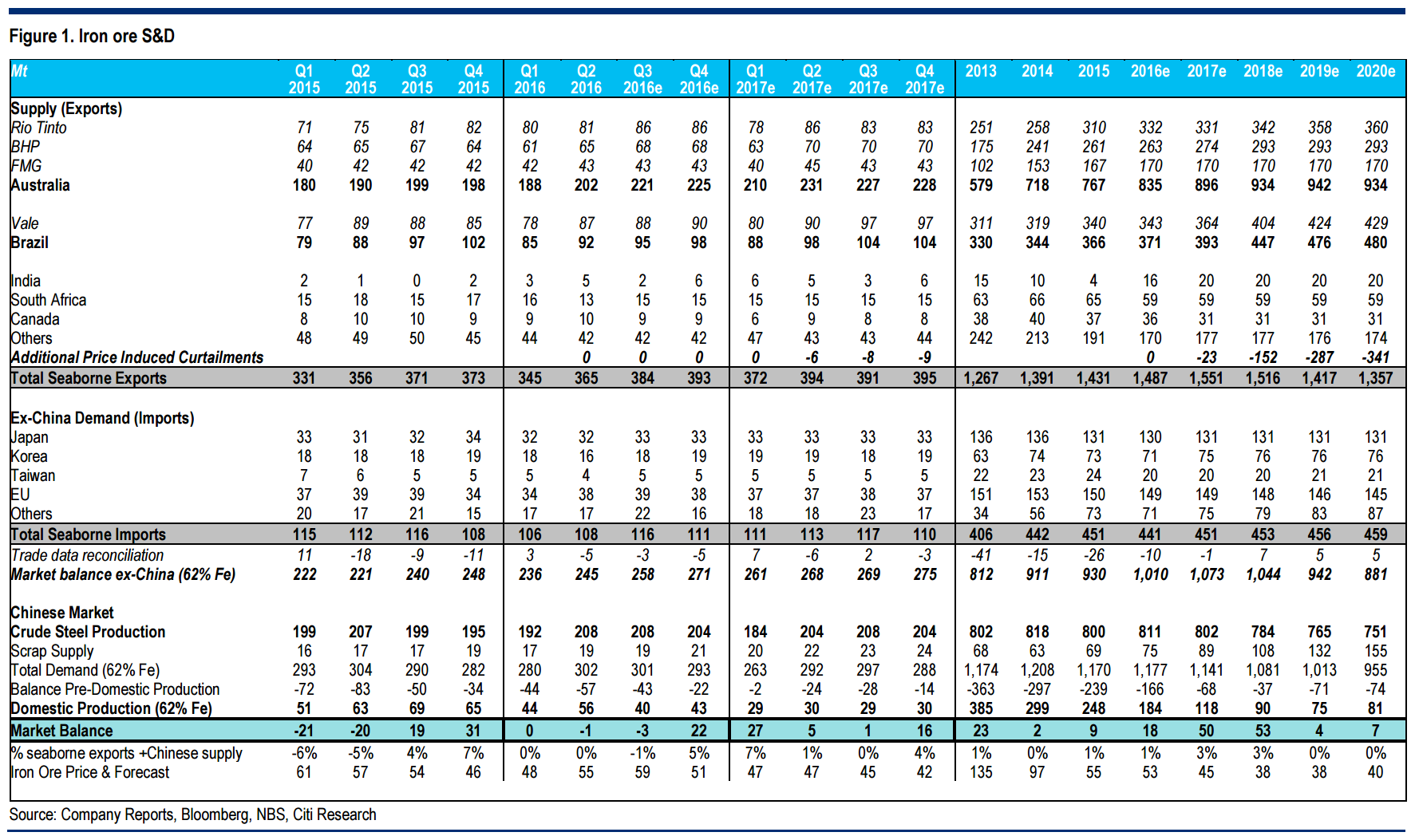

We still expect prices to fall below $40/t in the medium term – We estimate that Big 6 miners will be adding on an average 50-55mtpa of low cost capacity in the seaborne market over 2016-19. The structural balance will be achieved only when marginal and subscale suppliers to exit the market. Our experience over the last two years suggest that prices need to cut cost curve and remain below a certain period of time. We believe medium term prices need to go below $40/t to help accelerate the process.

Despite the Citi pullback they still see new tonnes at:

83mt next year

92mt in 2018

41mt in 2019

Roughly double my outlook! And they expect Chinese iron ore basically go almost entirely out of business to accommodate it.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.