It’s official. The 50-year lease over the Port of Melbourne has been sold for a whopping $9.7 billion to a consortium of four pension funds, including Australia’s QIC and the Future Fund.

The sale was valued at a multiple of 25 times earnings (EBITA), which is the same multiple from the Port Botany privatisation.

Thanks to the Federal Government’s asset recycling program, the Victorian Government will rake in another $1.45 billion, taking the total proceeds to just over $11 billion – an enormous war chest that will be spent on infrastructure projects throughout the state of Victoria ($4.5 billion has already been committed for level crossing removals).

I have mixed feelings about this deal.

Victoria (Melbourne in particular) desperately needs massive infrastructure investment. Melbourne is already straining under 12 years of rampant immigration, which has increased the city’s population by nearly 1 million people. There are infrastructure bottlenecks everywhere and congestion is rife both on the city’s roads and on public transport.

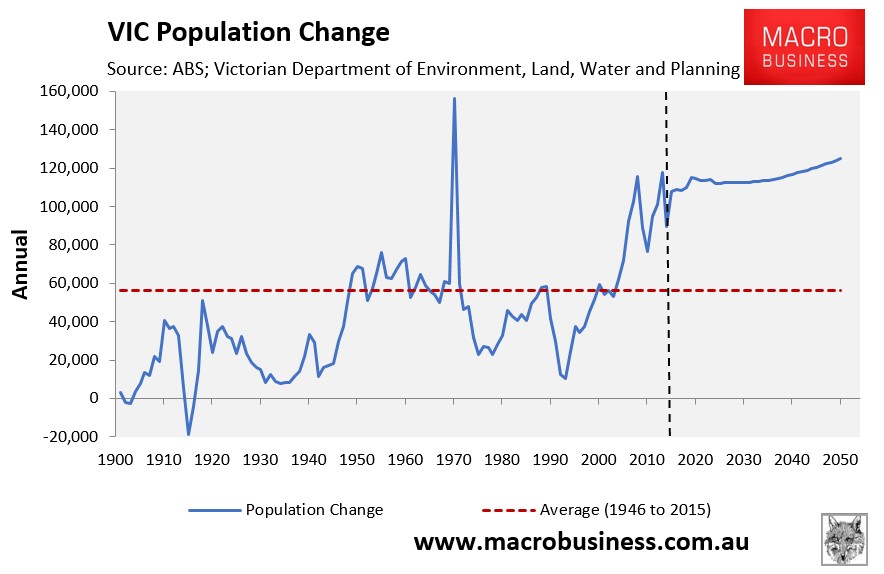

Worse, the Victorian Government’s own population projections have budgeted for an average of 115,000 new residents per year flowing into the state (mostly Melbourne) over the next 31 years, which is more than twice the post war average (see next chart).

Without massive infrastructure investment, Melbourne will grind to a halt, badly reducing productivity and diminishing the living standards of residents.

Therefore, if the proceeds from the Port of Melbourne’s sale can spur additional productive infrastructure investment, fantastic.

On the flip-side, the state is selling off a productive asset – effectively giving-up future cashflows for a lump sum – so there are long-term financial risks as well. If the new infrastructure investment is not productivity enhancing, Victorians will be made worse-off.

There are also genuine competition risks with the sale. It was the privatisation of key port assets – the Port of Newcastle and the Port of Melbourne – that recently caused ACCC head, Rod Sims, to turn against further asset sales. As reported in The AFR in June:

Price gouging by inadequately regulated monopolies before or after privatisation – all aimed at buffing the sale price for cash-strapped governments – is the common thread…

The Port of Melbourne hiked rents to stevedore DP World by about 750 per cent last year… The port is being readied for sale… and rents are not included in the proposed regulatory regime.

If the high sale price has come at the expense of the new private owners using their market power to force-up user costs and boost their profits, then the public could end up worse-off from the Port’s sale. We have seen this time and time again with the privatisation of other ports, airport parking, toll roads, and utilities (e.g. electricity, water and gas). In every case, the cost-of-living burden for users is the same as raising their taxes, albeit it in a less transparent manner since monopoly profits are easier to hide from public view.

As argued by professor Stephen King:

The government gets more today because we will all be paying more tomorrow…

Privatisation without competition risks turning a public monopoly into a private monopoly. The owners may change but the public will get ripped off just the same.

Therefore, the first rule of any asset privatisation should be that it boosts competition within the relevant market, or at a minimum does not lessen competition.

In the case of natural monopolies, a proper regulatory environment must first be put in place (which inevitable lowers the sale price), otherwise its sale will merely shift a public monopoly to a private monopoly, raising costs for end-users.

Unfortunately, the privatisation of the Port of Melbourne appears to have broken this golden rule, placing achieving a heavy sale price above the interests of users, in turn stifling competition and productivity.