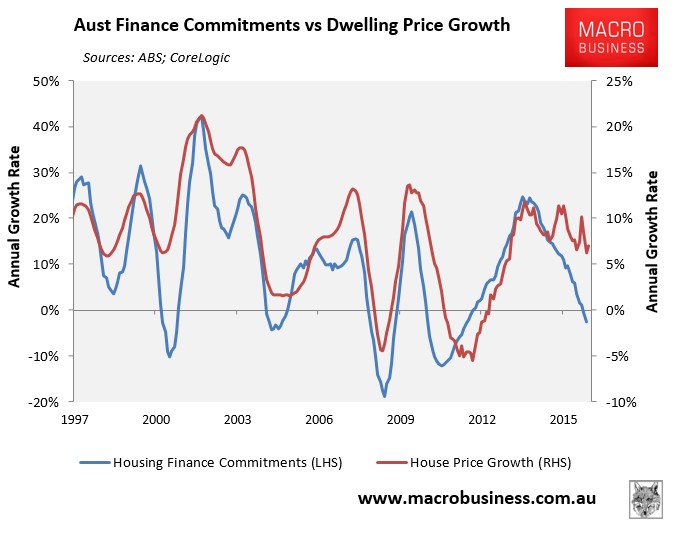

With the release yesterday of the state investor finance data for July, it is an opportune time to once again plot the total value of housing finance commitments (excluding refinancings) as measured by the ABS against dwelling values as measured by CoreLogic.

First, below is the national picture, which shows finance approvals highly correlated to price growth:

However, over the past year, dwelling prices have held firm despite a sharp fall in the value of housing finance commitments. This may be partly because CoreLogic changes its methodology in April, which has raised question marks over the efficacy of the index (see here).

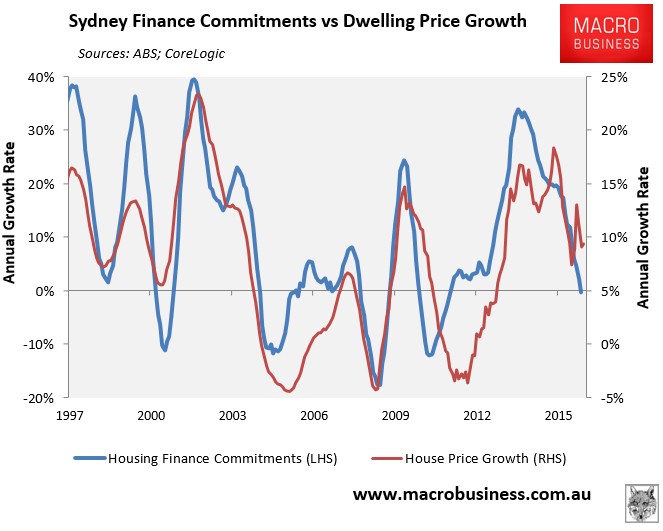

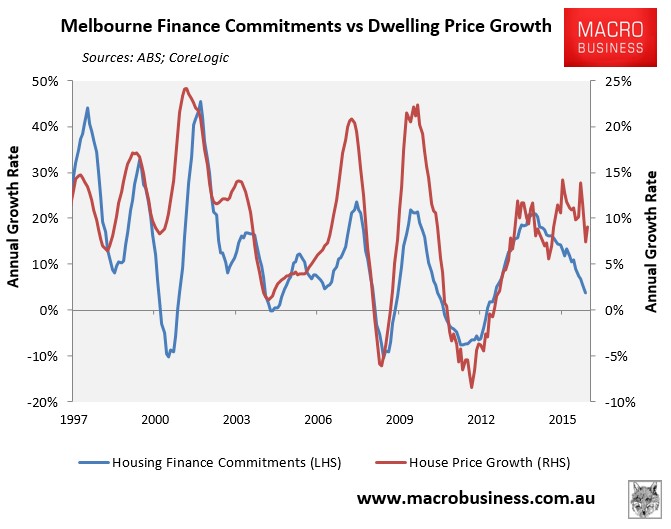

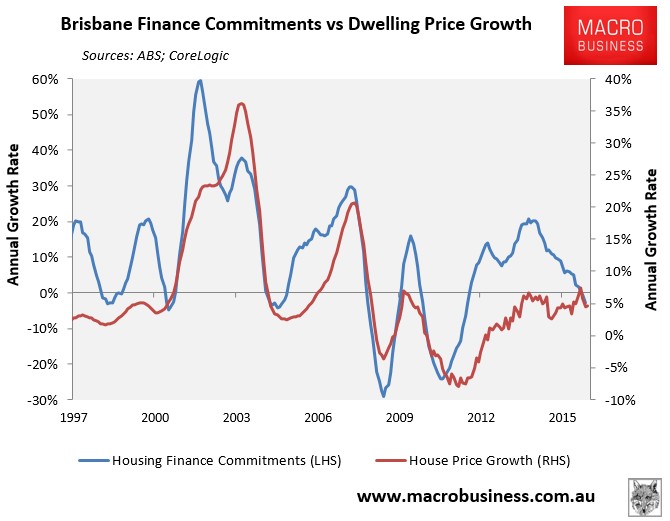

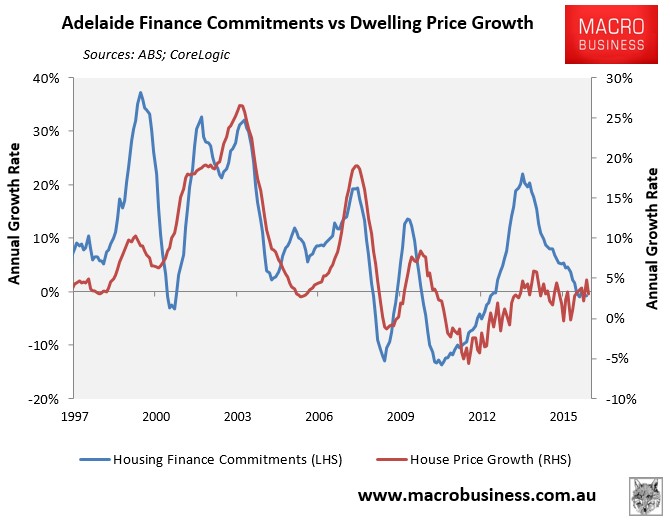

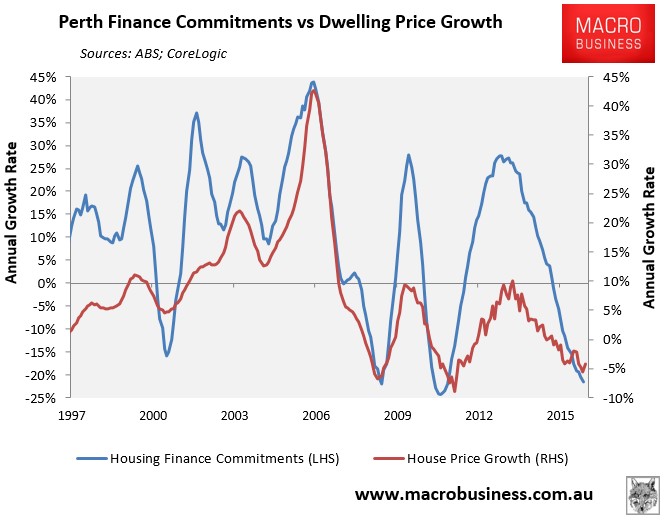

Across the five major capitals, there has also been a strong correlation between finance commitments and dwelling price growth; albeit with different lead/lag times:

Logically, with housing finance growth well past its peak in all major markets, it should also mean that price growth is also past its peak in each respective market.

However, prices have ‘bucked-the-trend’ since the start of the year across each major market except Perth, strengthening despite the weakening housing finance commitments.

As noted last time, there are several possible explanations for the divergence of housing finance commitments and dwelling price growth.

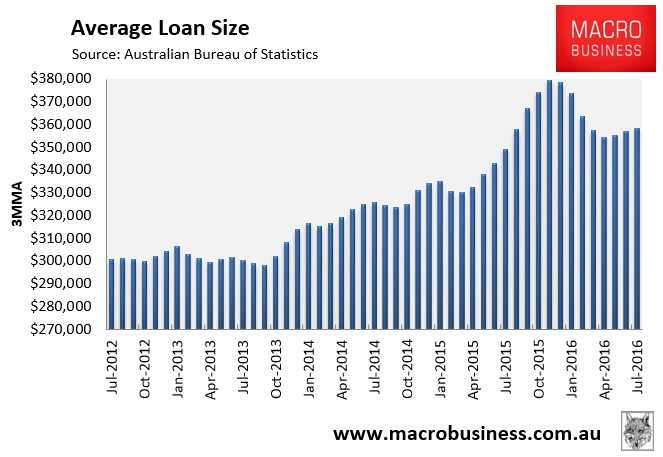

First, transaction volumes may have fallen even more sharply than the value of finance commitments (i.e. fewer loans chasing even fewer properties), which could explain recent rises in the CoreLogic index. However, this explanation is complicated by the fact that the average loan size has also fallen sharply since the start of the year, which would usually correlate with falling dwelling values:

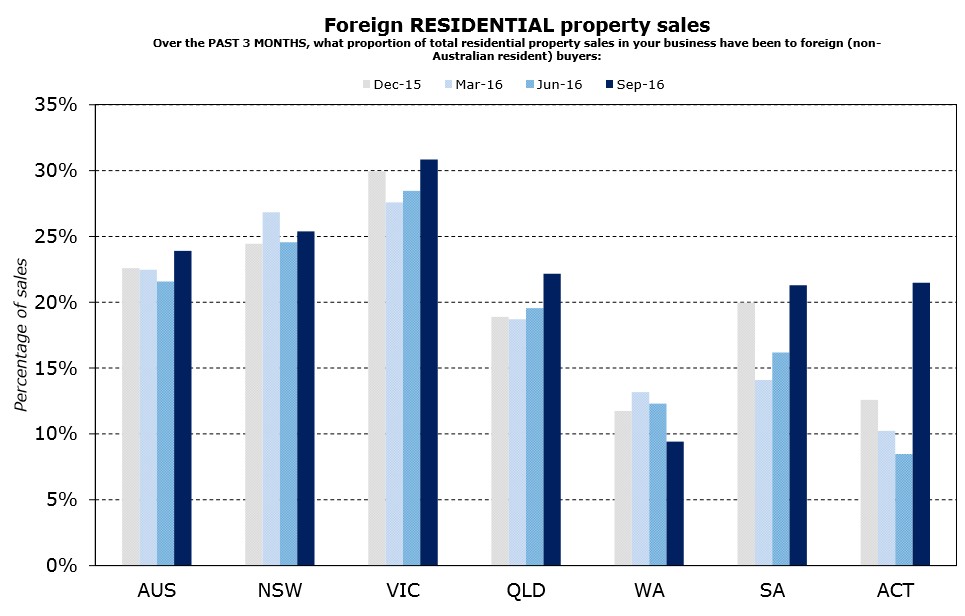

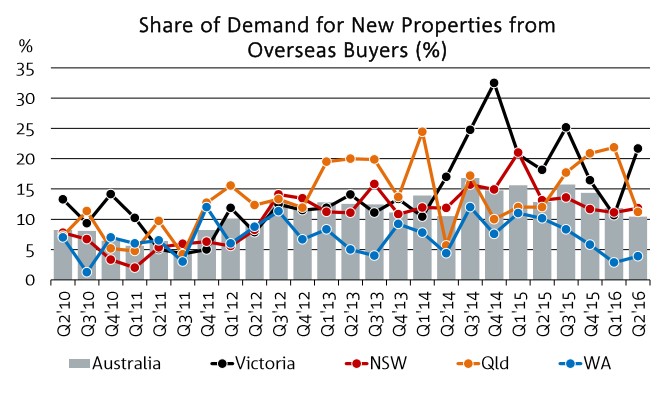

Second is the potential for cash buyers, such as buyers from overseas, whom are not captured in the housing finance statistics.

The most recent ANZ Property Council Survey of 1,600 industry participants suggested that home sales to foreigners have strengthened almost across board, with particularly strong demand present in VIC and NSW:

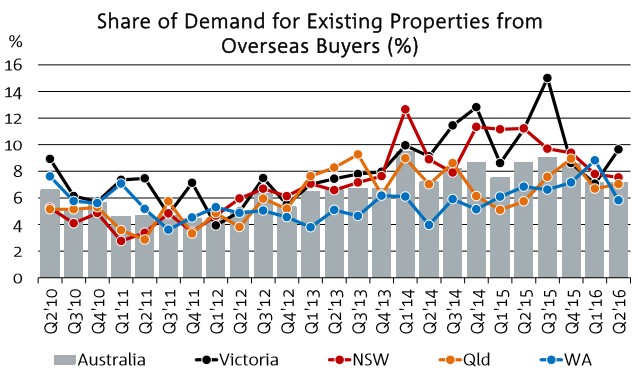

The most recent NAB residential property survey similarly revealed particularly strong demand from foreigners in VIC:

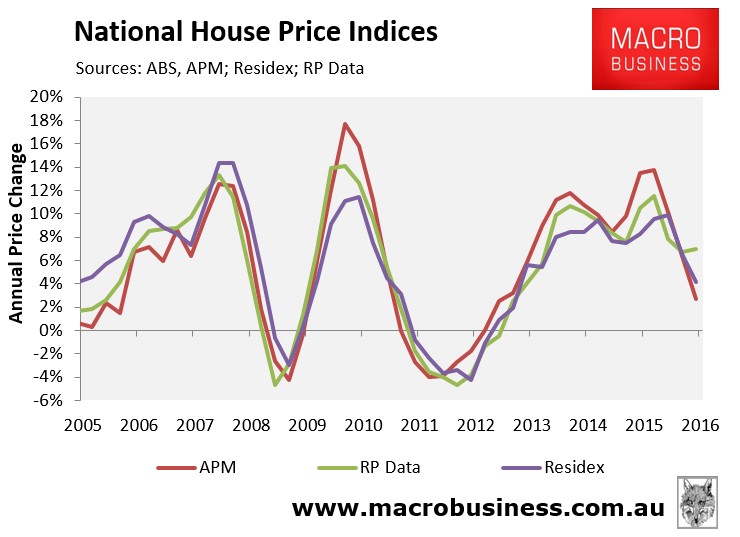

Third, the CoreLogic index could be displaying significant ‘numberwang’. As noted previously, it has diverged significantly from the other private indices:

The total value of housing finance (excluding refinancings) has historically been the single best indicator of price growth that I can think of. And the fact that it is pointing down for each major market should eventually mean falling price growth.