There is a victory of sorts today, with the Turnbull Government shelving its planned company tax cuts for big business amid a hostile Senate. From The Australian:

The Turnbull government is preparing to split its $48.7 billion company tax reform bill in order to secure an immediate gain for small employers, forcing it to shelve almost all of its core economic policy in the face of certain defeat in the Senate.

Scott Morrison is putting his focus on tax relief for small businesses with revenue of up to $10 million a year…

The Business Council of Australia has urged the Coalition to stick to the entire tax plan…

Labor has identified the shift in the government’s message but is holding out against the $10m threshold, arguing that the lower rate should go to employers with turnover of only up to $2m.

The government hopes to secure an agreement with the Nick Xenophon Team and Pauline Hanson’s One Nation, the Greens and other crossbenchers to legislate the $10m threshold…

The cut in the company tax rate costs $2.7bn over the four years but the budget impact mounts steeply after that if the lower rate is passed on to bigger companies.

To pass a Bill through the Senate, the Coalition needs 39 votes, meaning that it is nine votes short. Hence, it is highly unlikely to gain the votes needed to pass its company tax cut plan in full.

Moreover, it is hardly surprising that the Business Council of Australia continues to lobby hard for the company tax cut, given it is big business that stands to gain the lion’s share of benefits from lower corporate taxes.

Local owners of unincorporated businesses are essentially taxed at their personal tax rate, because of Australia’s dividend imputation system. Hence, lowering the company tax rate from 30% to 25% will provide local owners and shareholders with minimal benefits, since any reduction in company taxes will be offset by a commensurate reduction in imputation credits.

By contrast, the major beneficiaries of a company tax cut are foreign owners/shareholders, since they cannot avail themselves of imputation credits. And since most big businesses have some degree of foreign ownership, it is they that reap the benefits from any company tax cut.

Former Treasurer and Prime Minister, Paul Keating, said it best when he wrote the following earlier this year:

Australia’s dividend imputation system works such that the company tax is, in effect, a withholding tax – a tax temporarily held by the Commonwealth which is returned to shareholders when their dividends are paid. So, whether the company tax is withheld by the Commonwealth at a rate of 30% or 25% is immaterial – the Commonwealth is going to return the money to shareholders anyway, regardless of the rate. But the shareholders who will receive a benefit are foreign shareholders.

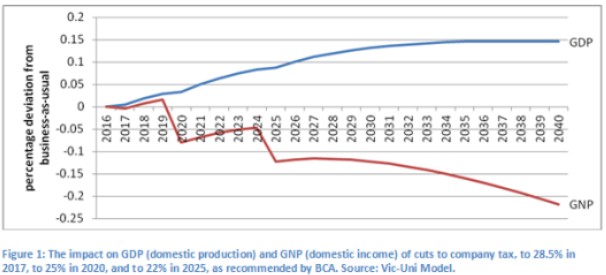

For this reason, modelling from Victoria University senior research fellow, Janine Dixon, found that cutting the company tax rate would actually lower national income (GNP) and living standards:

It is also why a conga-line of commentators have questioned the Coalition’s policy, including:

- The Grattan Institute

- The Australia Institute

- Goldman Sachs

- ABC’s investigative reporter Stephen Long

- Fairfax writers Peter Martin, Ross Gittins, Michael Pascoe, and Mark Kenny

- Former Liberal leader, John Hewson

- the University of Technology Sydney

- The Australian people

With the Federal Budget facing immense structural pressures and a “revenue problem” – as acknowledged by Treasurer Scott Morrison in his recent speech – there is no sense in gifting tens-of-billions of dollars to foreign owners/shareholders, and in the process worsening the Budget position and lowering national income.

The Turnbull Government is wise to backtrack.