Australia’s big business lobby group – the Business Council of Australia (BCA) – has lashed out at Treasurer Scott Morrison for abandoning company tax cuts for large businesses, claiming that Parliament had effectively “given up on Australia’s global competitiveness”. From The AFR:

[BCA President Catherine] Livingstone said the BCA was lobbying members of Parliament to ensure all of business won the tax cuts, regardless of company size.

“What other lever are we going to pull to make Australia more attractive for business investment, which is currently falling at a rate not seen since the 1990s recession,” she said.

“The reality is that the prosperity of all Australians can only be underpinned by strong and competitive businesses of all sizes investing, growing and employing into the future.”

Let’s be clear, the BCA is a lobby group for the CEOs of the Australia’s 100 largest companies. And it is the owners of these large corporations that would benefit from cutting company taxes, while the rest of us would pay the price.

To understand why, one needs to understand Australia’s dividend imputation system.

Local owners of unincorporated businesses are essentially taxed at their personal tax rate, because of dividend imputation. Hence, lowering the company tax rate from 30% to 25% would provide local owners and shareholders with minimal benefits, since any reduction in company taxes would be offset by a commensurate reduction in imputation credits.

By contrast, foreign owners/shareholders are major beneficiaries of a company tax cut because they cannot avail themselves of imputation credits. Since most of the BCA’s big business members have some degree of foreign ownership, it is they that reap the lion’s share of benefits from any company tax cut.

Former Treasurer and Prime Minister, Paul Keating, explained it best when he penned the following earlier this year:

“Australia’s dividend imputation system works such that the company tax is, in effect, a withholding tax – a tax temporarily held by the Commonwealth which is returned to shareholders when their dividends are paid. So, whether the company tax is withheld by the Commonwealth at a rate of 30% or 25% is immaterial – the Commonwealth is going to return the money to shareholders anyway, regardless of the rate. But the shareholders who will receive a benefit are foreign shareholders”.

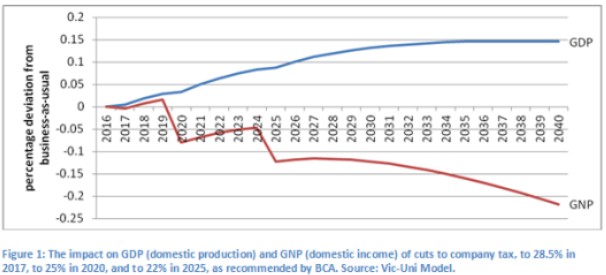

For this reason, modelling from Victoria University senior research fellow, Janine Dixon, found that cutting the company tax rate would actually lower national income (GNP) and living standards because of the benefits flowing offshore:

We should also acknowledge that the modelling used by the BCA to support the company tax cut is highly spurious (read here for a good summary).

One of the biggest howlers is that the modelling heroically assumed that multinationals would cease shifting their profits offshore if the company tax rate was cut from 30% to 25%, thus making the cut largely self-funding. Obviously, if this revenue gain does not come to fruition (a near possibility), then it would need to be made up by raising taxes elsewhere or cutting public services.

Even ignoring these revenue furphies, the modelling also showed minimal benefit to employment or growth from the proposed $48 billion company tax cut, as noted by Peter Martin:

The Independent Economics modelling finds that after several decades the $8 billion per year would lift living standards by between $5 billion and $9 billion. That’s not an increase of $5 billion to $9 billion per year, its an eventual increase that would be maintained. As a proportion of gross national income it is somewhere between 0.5 and 0.7 per cent. As an increase per year it is less than 0.1 per cent. Rounded to one decimal place it is 0.0 per cent.

And the boost to jobs would be even smaller. Independent Economics says employment would eventually climb by 0.17 per cent if the tax cut was funded by a tax on households, or by as little as 0.02 if it was funded by cutting government spending. That’s an eventual increase of between 2400 and 20,400 jobs. By way of comparison employment has climbed by an average of 24,400 per month each over the past year. It means that after 20 to 30 years the $8 billion per year holds out the prospect of delivering an extra month’s worth of employment growth.

It’s not many jobs and not much growth…

With the Federal Budget facing immense structural pressures and a “revenue problem” – as acknowledged by Treasurer Scott Morrison in his recent speech – where is the sense in gifting tens-of-billions of dollars to foreign owners/shareholders, and in the process worsening the Budget position and lowering national income?

The bottom line is that the Coalition’s company tax cut was always an expensive dud that should never have been proposed in the first place.

The BCA is merely talking its own book.