Despite dozens of trade cases being in play, China’s steel exports continue to expand, crowding out other sources worldwide. Who wins? Those that deliver China’s steel raw materials.

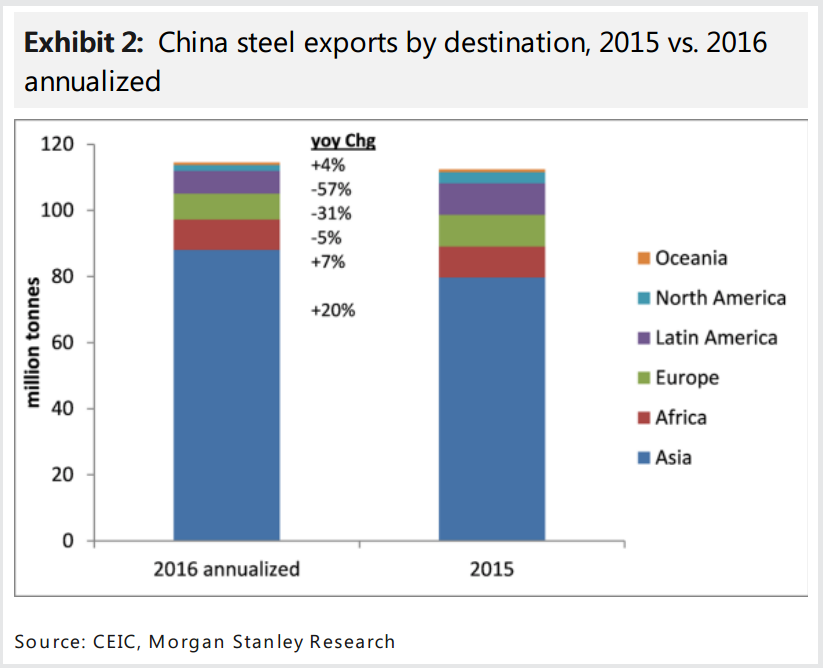

Effective switching: China’s steel exports expanded by 4.9Mtyoy (+9%) in 1H16, now annualizing at 115Mt (vs. 2015’s 112Mt), seemingly shrugging off a ballooning set of tradecases worldwide. Yes, China’s steel exports to Europe, Latin America and North America (home of most of thetradelitigators) have fallen in 2016 (by 3Mt in 1H16; -30% yoy). But alternative markets were quickly identified, mostly in Asia – Vietnam,Thailand and the Philippines – lifting exports to the region by 7.5Mt (+20% yoy).

Poorly built barriers: Early 2016, the global steel trade hoped that the widespread prosecution of China’s steel exports could cap its growth, helping rebalance markets ex-China. However, our review of the cases in play revealed that only a small proportion of China’s exports was at risk. Why? Most cases were brought by countries that import only tiny volumes from China, and most cases only target very specific products – missing the bulk of the flow.

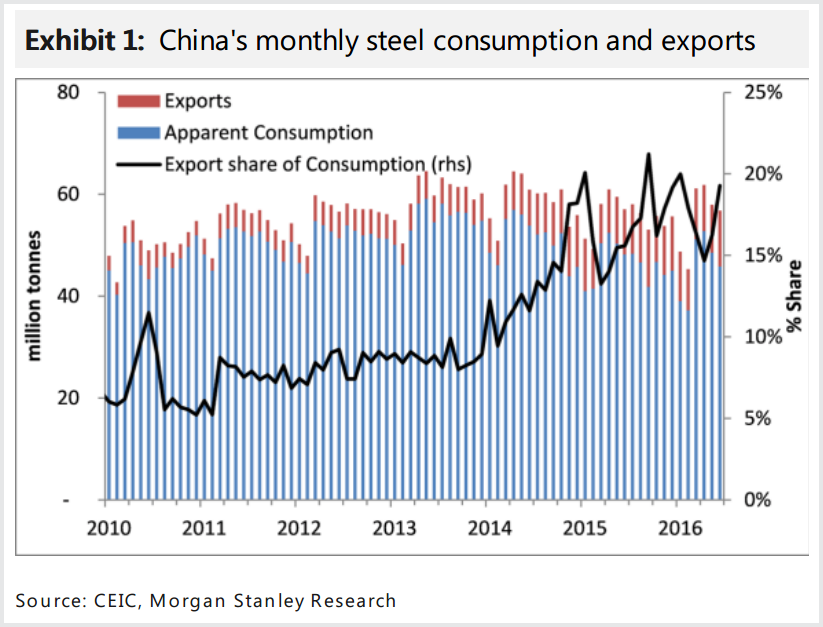

Innocuous capacity cuts: Given the relative stability in China’s domestic finished steel demand (MS 2016e 679Mt, +1%yoy), it was widely expected that the central government-led industry reform program this year (>40Mtpa cut; down to 1,030Mtpa) would effectively deliver a cap (or cut) to exports. But despite 107Mt of capacity cuts since the start of 2015, exports remain a large portion of the industry’s total output (14% in 2015-16 vs. 11.5% in 2014), competing with steel producers worldwide.

Who actually wins here? Seaborne-linked iron ore and met-coal traders certainly do. The emerging upside risk to our 2016 China steel production rate (790Mt) potentially alters our forecast demand and prices for steel’s raw materials. In March, we forecast 771Mt of crude steel production in 2016 for China, and a corresponding 60Mt surplus for the seaborne ore trade. Four months later, China’s 1H16 crude steel output’s annualizing at 802Mt ( 30Mt-‘delta’ requires 45-48M textra imported ore, halving our forecast trade surplus); China’s met coal imports are annualizing at 54Mt, +35% vs. our March 2016 outlook – such is the step-change in expectations for China’s 2016 steel production rate.

Yes, steel exports are holding up better than I expected too, though many more protectionist actions are in the pipeline. On the question of who wins, in the end the answer is not so positive: nobody does.

Subsidised Chinese steel dominates global markets crashing the price (which despite the bounce is today at 2003 levels) and drives down the cost curve for iron ore as well. The last five months has been a little reprieve in the bear market for both not a trend change.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.