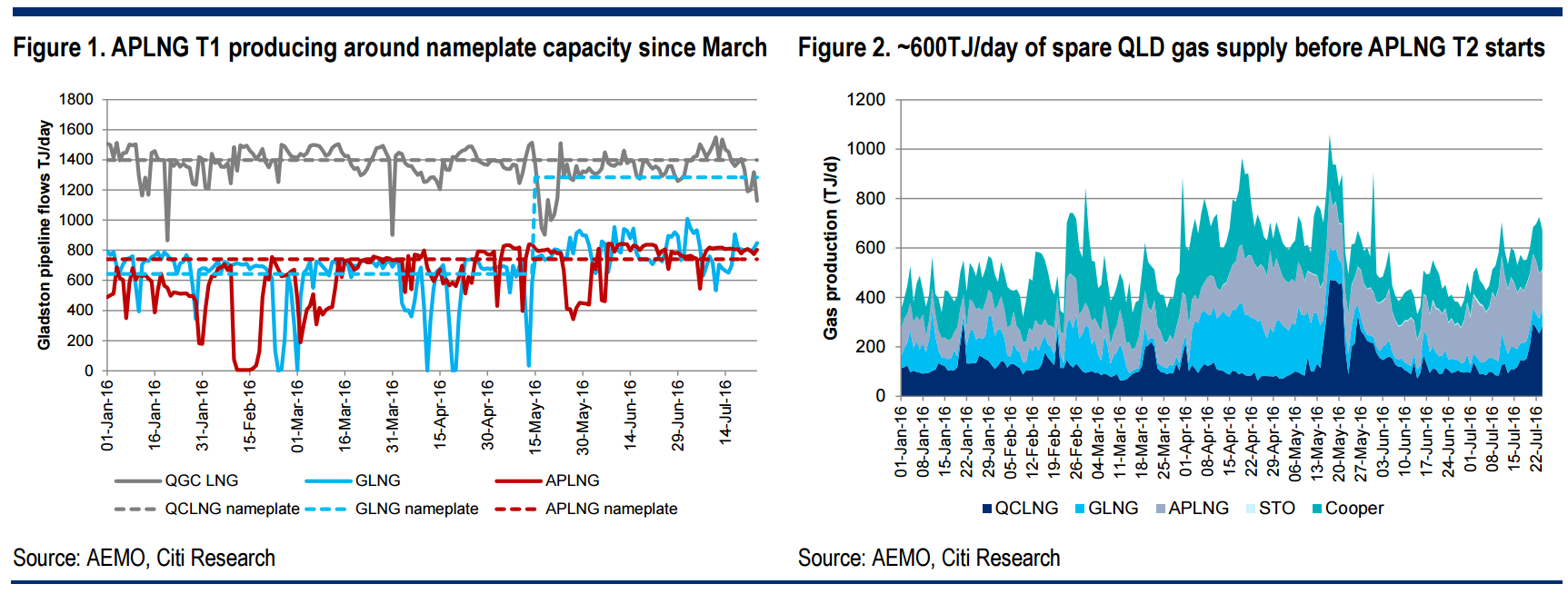

APLNG T1 in 120d test, T2 on track for October start-up — T1 averaged 95% of nameplate capacity in Q4 and has average 105% in July to date. ORG has guided to the first tranche of parental debt guarantees (~60% of the project financing) rolling off in Q2FY17. With all gas turbine generators now up and running we continue to expect first LNG in October. With >600TJ/day to potential production shut in behind well heads we expect APLNG T2 ramp up to not be limited by gas, and therefore a quick ramp up to full capacity (see Figure 2).

Sinopec LNG contract upheld so far — ORG has previously remained adamant that Sinopec would honor contractual obligations, although it would likely exercise the option to flex down contract levels by 10% for the first 4 years. Obviously taking initial cargoes is not definitive proof of honoring a 7.6mtpa 20yr contract, but it is a good start and we expect it to continue being honored, see LNG contract sanctity overhanging ORG. See Figure 3 for Chinese LNG cargo destinations to date.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.