…We measure this drawdown for OECD inventories both in absolute terms, millions of barrels, as well as relative to demand, in days of OECD demand. We expect that the drawdown process will begin in Q2-17 and run through the end of 2018 at which point the surplus will be close to, but not completely, eliminated.

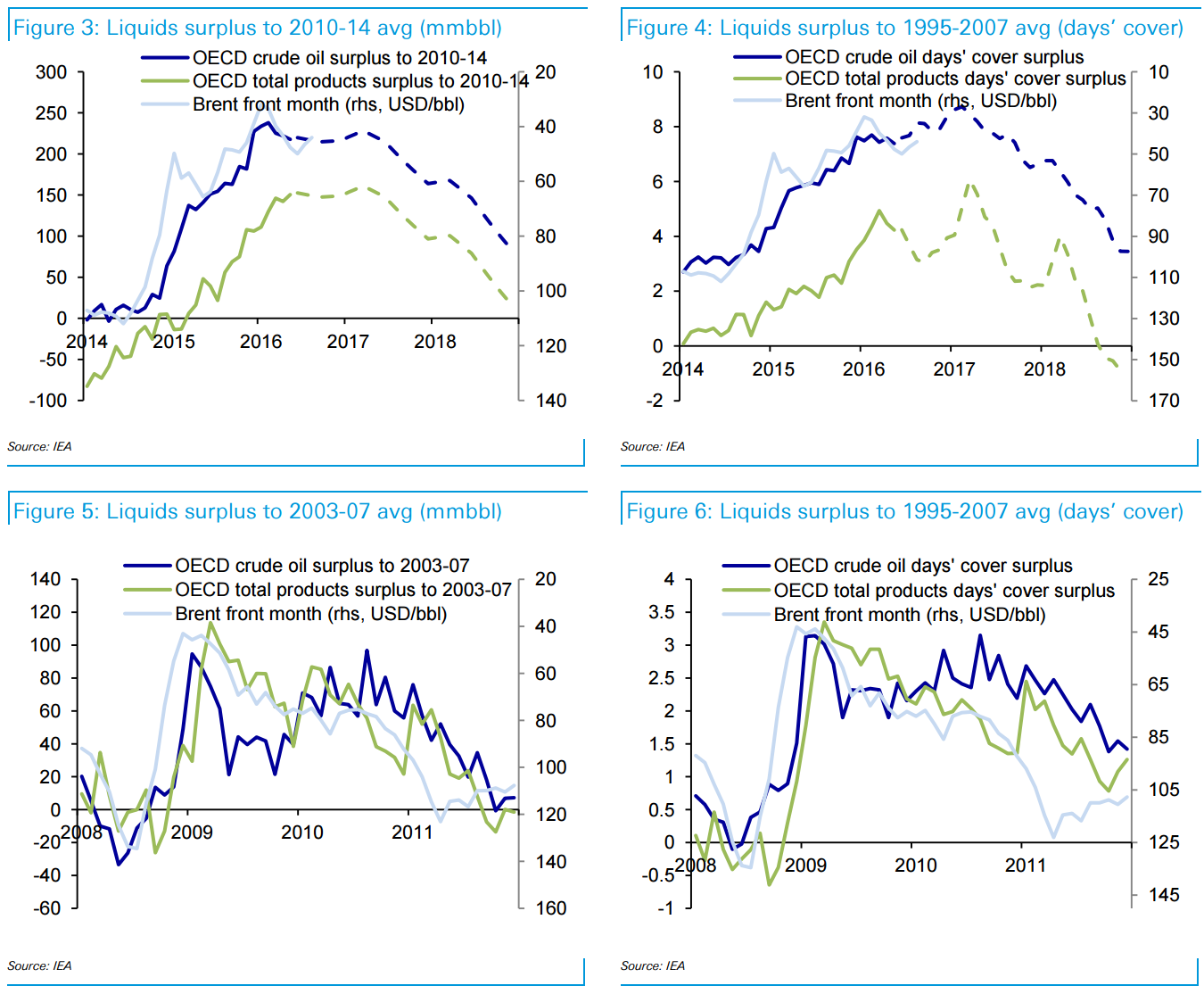

A useful comparison can be made to the 2008-09 surplus despite the fact that the previous episode was largely demand-led. We compare 2008-09 stocks versus the preceding five year period 2003 to 2007, and we compare current stocks versus the 2010 to 2014 period. The example suggests that our worries over a potentially lower equilibrium (incentive-cost) price, which will be driven by sustainable improvements in the upstream cost structure, may be beside the point. As product surpluses fell in late 2010, Brent front-month prices rose steadily, despite a seasonal rebuilding of surpluses in Q1-11. We note that prices rose above what would have probably been recognized as a marginal incentive cost even before inventories were completely normalized.

Compare this example to our forward expectations which are that Brent prices will average USD 55/bbl in 2017, helped by the first signs of reductions in the OECD inventory surplus towards the second half of the year. Although incentive costs may eventually prove to be lower than we estimate, the possibility of an overshoot to the upside may compensate to some degree for a potential overestimate of costs. We believe that our modeled inventory surplus drawing significantly closer to normal in 2018 is consistent with prices approaching the marginal (upper) end of the incentive cost curve of USD 70/bbl.

It is very much the case that falling oil and oil product inventories will be a major oil buy signal. My view is that the tipping point will be a little further out than the Deutsche reckons hence I see one more decent price drop (all things being equal) before oil can rally sustainably. Note that even on Deutsche’s more bullish outlook the tipping point for higher prices is still six months away.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.