He suggested that July’s example of northern gas going south could become more common, despite the extra cost for transportation, given regulatory impediments such as Victoria’s ban on onshore gas.

A range of stories today on the east coast gas cartel shows nicely the Banana Republic at work. First off, the IEEFA defends itself at Renew Economy following last week’s extraordinary attack upon it at the AFR:

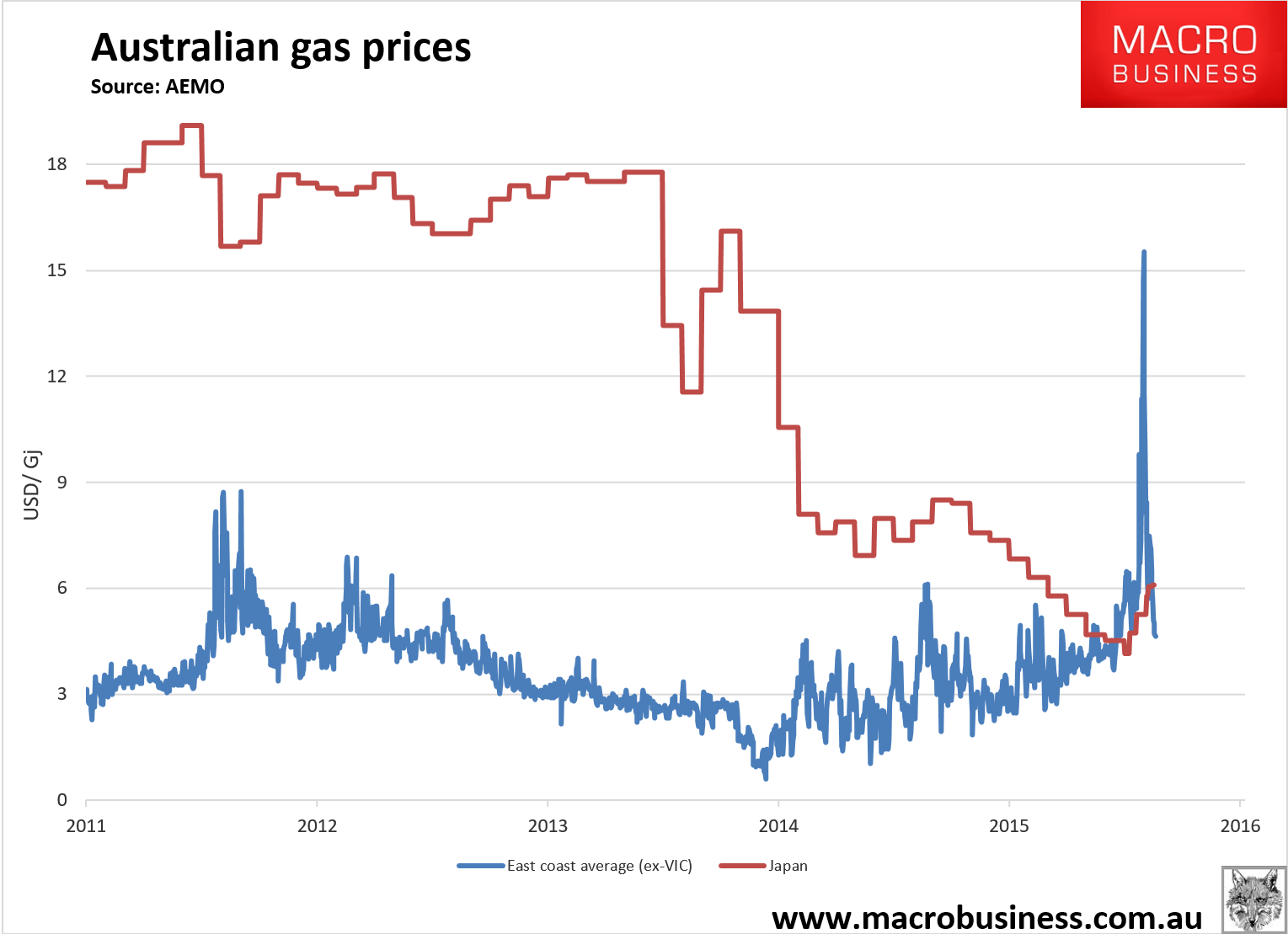

Debate rages after an IEEFA spot-price analysis showing Australians consumers paying more for Australian natural gas than their Japanese counterparts who import it as a liquefied product.

It’s hard to overstate the bizarre nature of the gas market in Australia.

Only recently, gas was cheaper in Australia than in the U.S. But the development of three new LNG terminals on the Australian east coast has driven up prices by linking domestic supplies to the most expensive gas market in the world, the north Asian market.

Perhaps the larger problem for Australian consumers is that the East Coast gas market is controlled by an opaque cabal of players that include Shell, Origin Energy, Santos and BHP/Exxon and that collectively control existing supply and that fail to disclose existing production capacity, reserves or resources on a consistent basis.

Basic information is almost impossible to come by. For contract prices, for instance, the most recent data available is from a survey conducted eight months ago for the Australian Competition and Consumer Commission (ACCC).

There are no official figures for contract prices in Australia today, a circumstance that would be unheard of in markets like the U.S.

Regulators are floundering and the situation has become so preposterous that proposals for South Australia to develop a regasification plant to import LNG from the U.S. are being seriously considered.

The revelations that Australians are paying more for Australian gas than their Japanese counterparts drew a predictable response from the gas industry: attack the messenger.

Industry analysts, led by consultants EnergyQuest, run by a long-time former Santos executive, Graeme Bethune, publicly questioned our findings, but not very effectively because it’s hard to argue with fact.

For the month of July, the Japanese Ministry of Economy, Trade and Industry (METI) had the spot market price (which in turn drives contract prices) at $8.42/GJ. In Australia for the same month, the Adelaide spot price—one of three short-term trading markets set up by the Australian Energy Market Operator (AEMO) with the express purpose of providing transparency—was $13.90/GJ.

Here is the chart in question:

Looks pretty straightforward to me. But not so at the AFR which prefers the propaganda of Shell:

Advertisement

Shell Australia has at times been holding back from running its Queensland LNG project flat out, opting instead to sell gas into the strong domestic market.

Country chairman Andrew Smith revealed the energy major sent gas from its Queensland coal seam gas operation to the southern states in July to ease supplies during a prolonged cold snap, which sent wholesale gas and power prices surging.

This year, the Queensland Curtis LNG venture has sold twice as much gas into the domestic market than it has purchased from third parties for its operation, Mr Smith said, rejecting suggestions that export customers are being favoured over the local market.

…Mr Smith’s comments signal that for the QCLNG project at least, little gas is being sold on the low-priced Asian spot LNG market, with production beyond higher-price contracted deliveries adjusted depending on prices in various markets.

Heroic of Mr Smith, no? Except for the small problem that this is called “profiteering”. For a brief time in Winter Aussie gas was so expensive here versus Japan that Shell made more money following the pricing signal and selling it locally.

Meanwhile, at The Guardian the great Curtis Island white elephant is revealed in all of its white elephantine mange:

Advertisement

Santos, one of the companies driving Queensland’s liquefied natural gas export boom, is relying on price projections so optimistic that they inflate the value of the company’s assets by billions of dollars, according to a leading analyst.

This month Santos announced a write-down of the value of its Gladstone gas export project, GLNG, of US$1.5bn. The value of the project dropped because the price it gets for the exported gas is tied to the price of crude oil, which has dropped.

But according to an analysis by the pro-renewables financial activist group Market Forces, that write-down of its assets relied on an optimistic prediction for how the oil price will change, with Santos’s projections significantly higher than those of competitors Woodside and Beach Energy, brokers such as Deutsche Bank and Goldman Sachs, as well as analysts at the World Bank.

According to Santos’s own explanation of how its asset’s value is tied to oil prices, if it had used Goldman Sachs’ projected oil prices rather than its own optimistic ones, the value of its assets would be US$3.5bn less in 2020.

Well blow me down with a feather! Recapping:

- the east coast gas cartel withholds gas from the local market to ship it as LNG;

- that has created a shortage at home which, when it turns acute, the cartel profiteers from by turning gas back south;

- an obtuse media celebrates them as heroes;

- but, the cartel shipments to Asia are profitless anyway on an all-in cost basis leading to massive write downs and zero profits;

- which aren’t recognised because there is no regulation, so the profitless, gouging, hollowing out dance can go on.

It’s Banana Republic economics 101.

Advertisement