ME has released its 10th biannual Household Financial Comfort Report, which provides insight into the financial situation of Australians based on a survey of 1,500 households.

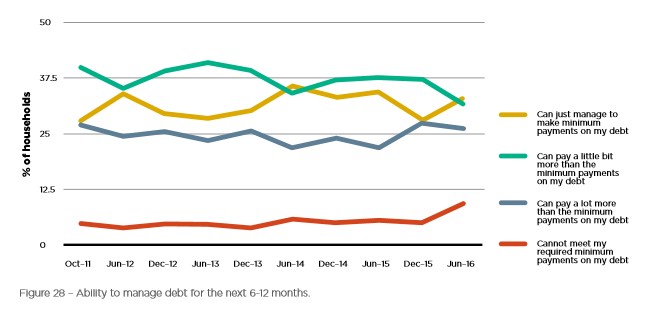

This latest report reveals a marked deterioration in Australian households’ confidence in their ‘ability to manage debt over the next six to 12 months’, doubling from about 5% over the past few years to 10% as at June 2016 (see next chart).

Consistent with an expected rise in debt stress, more households ‘paying off or owning a home’ reported to be drawing on their home equity to ‘pay off debt’ (up 4 points to 11%) and ‘to make ends meet’ (also up 4 points to 10%) during the first half of 2016.

‘Single parents’ reported the highest levels of concern in their ‘ability to meet minimum debt repayments over the next six to 12 months’ (19%), followed by ‘couples with young children’ (15%) and ‘young singles/couples’ (12%).

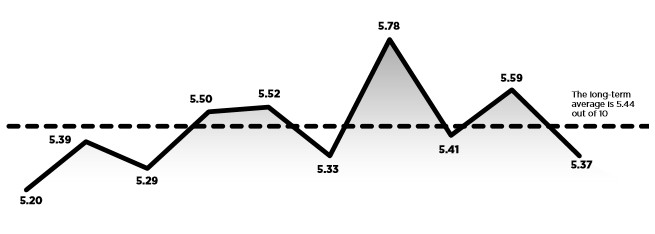

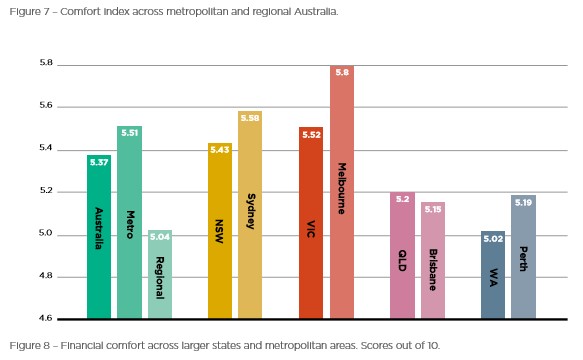

As for the overall finding, ME’s overall Household Financial Comfort Index – a measure of households’ perceptions of their financial comfort − dropped significantly by 4% to 5.37 out of 10 in the six months to June 2016. This result means about 90% of Australian households reported low-to-mid financial comfort, with only 10% reporting high comfort.

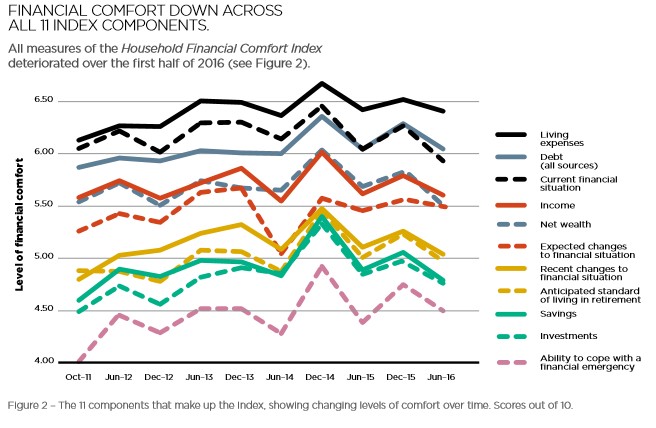

All 11 index components deteriorated, with the largest falls seen in ‘net wealth’, ‘income’, ‘cash savings’ and ‘investments’ as well as households’ ‘ability to handle short-term income loss’ and ‘anticipated standard of living in retirement’:

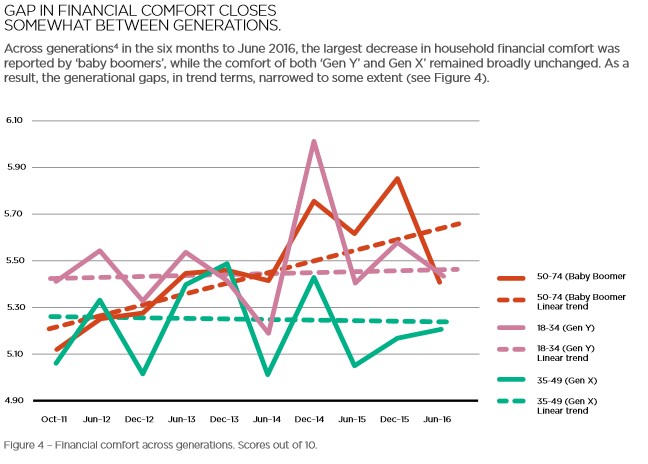

In terms of generations, the comfort of ‘baby boomers’ fell the most of any generation (down 7%) to the lowest level reported for that age cohort in the past couple of years (5.42 out of 10) – lower than ‘Gen Y’ (down only 2% to 5.46), but still above ‘Gen X’ (steady at 5.18):

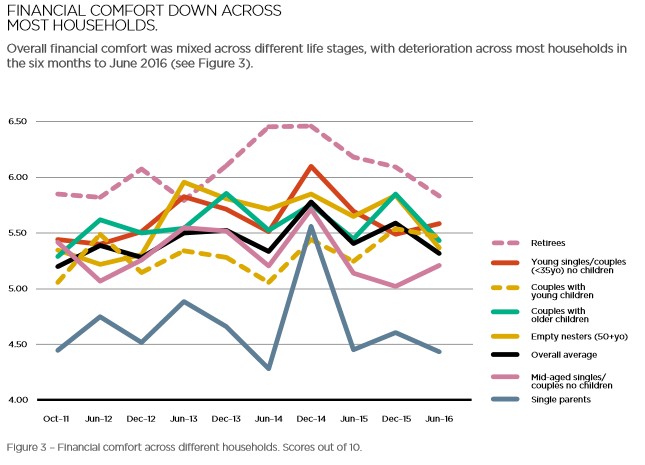

‘Retirees’ reported their lowest levels of comfort since the survey began, although they’re still the most financially comfortable of any household life stage:

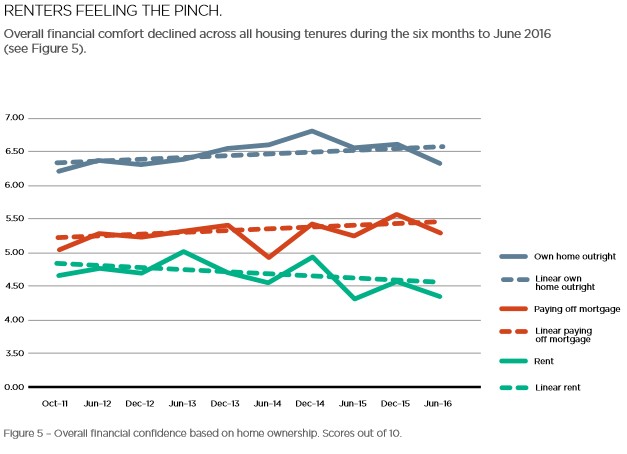

The comfort of ‘renters’ is significantly lower than the comfort of both households ‘paying off their mortgage’ and to a greater extent ‘homeowners’ (those that own their home outright) and the divergence is widening:

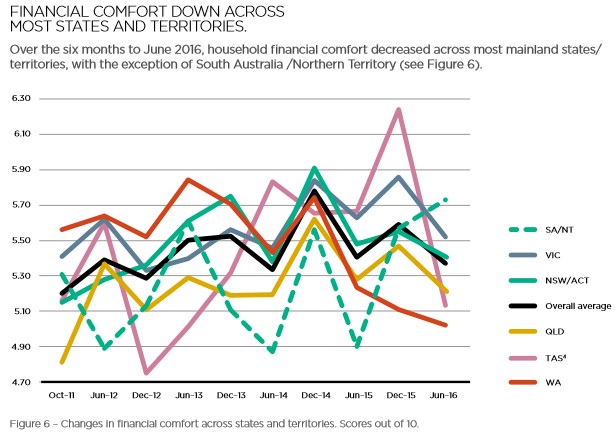

Bizarrely, financial comfort fell in all states and territories except SA/NT. Financial comfort is also highest in SA/NT, which given recent job losses seems to be a weird result:

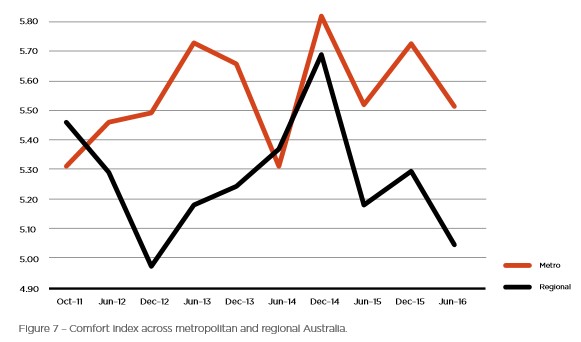

Metro regions are generally far more comfortable financially than the regions:

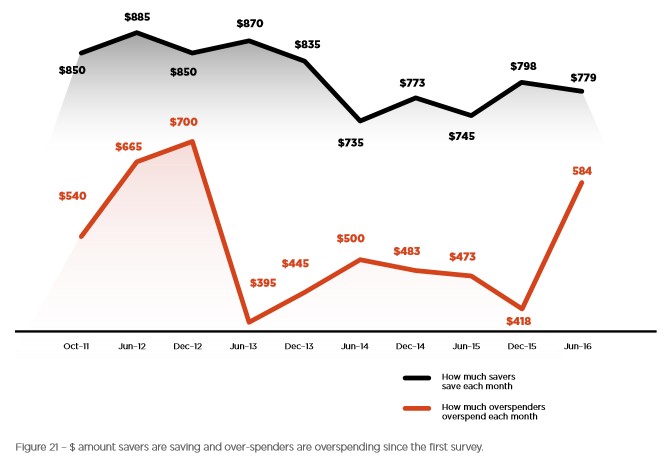

There has also been a marked increase in the amount of households overspending, while the amount of savings remained relatively unchanged: