EVN reported strong underlying earnings for FY16, in line with our expectation.

Strong underlying earnings. EVN reported strong underlying earnings with Ebitda of $607.5m and Ebit of $272.1m, within 3% of our forecasts. Underlying Npat of $226.8m was 7% lower than our expectation of $243m. After one-off transaction costs and the previously flagged impairment of the Pajingo mine, the company reported a statutory Npat loss of $24.3m. The company declared a full-year dividend of 2cps unfranked.

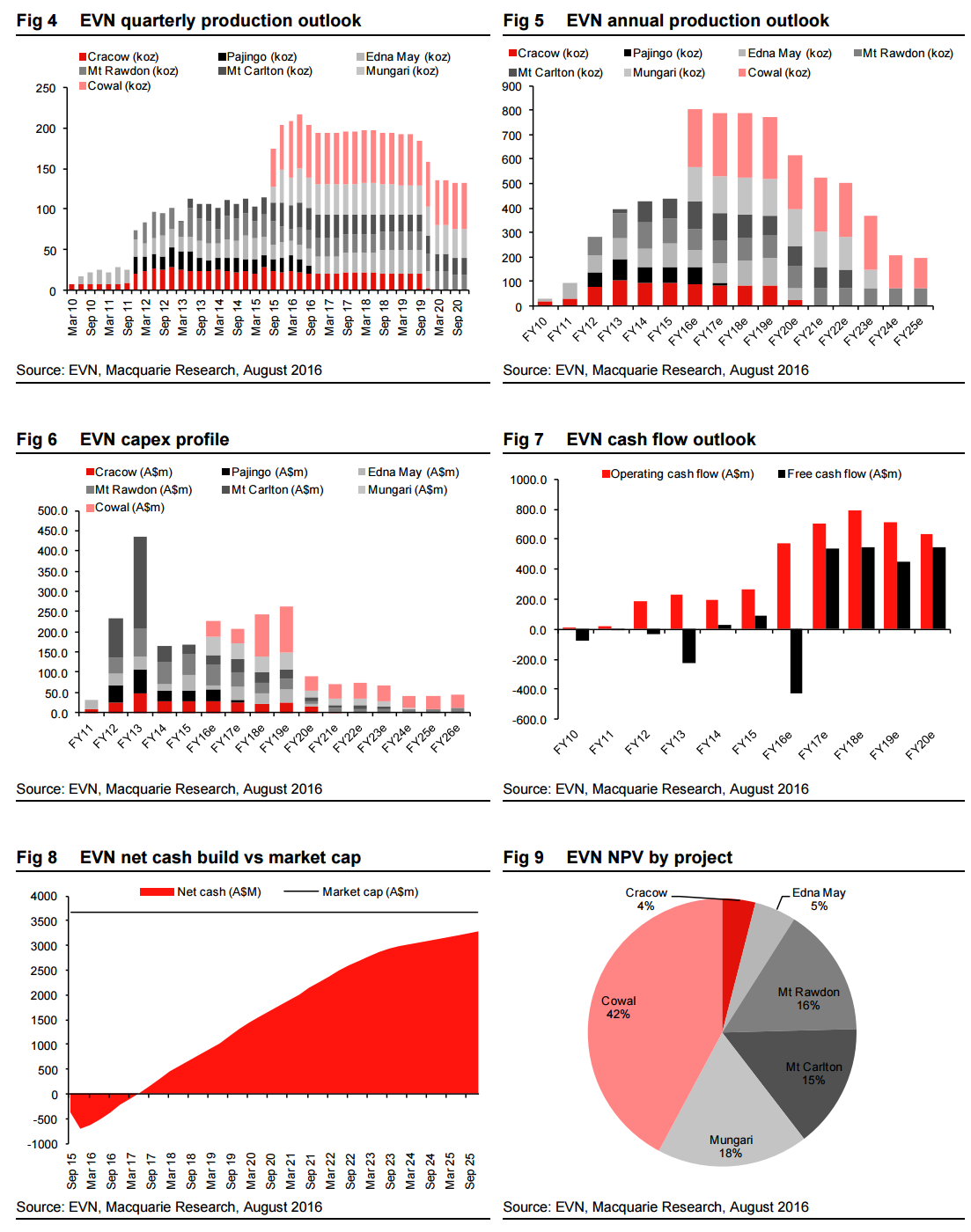

Accelerated debt repayments to continue. The strong cash flows in FY16 allowed EVN to accelerate the repayment of its debt facilities with $332m of the $700m Revolving and Term facility repaid. EVN expects to continue accelerated repayment in FY17 and FY18. Current commentary for the company indicates that all ‘excess cash’ will be directed to debt repayment. We currently assume that the remaining $95m of the Revolving facility will also be repaid by early FY18. We note though that EVN has also indicated that it is comfortable with its current 15% gearing.

Pajingo sale, more streamlining contemplated. As previously flagged, EVN has applied a $77.3m impairment to the carrying value of the Pajingo mine. As announced earlier this week, Minjar Gold has agreed to purchase the mine for an upfront cash payment of $42m and a $10m NSR. The cash from the sale will be applied to debt. EVN contemplated additional asset sales in conjunction with the divestment of Pajingo, including both Cracow and Edna May. However, the good results coming from Coronation and the commencement of the Edna May underground were deemed as higher-value options. Optimisation of the company’s portfolio, be that via acquisition or divestment, remains a core strategy. Earnings and target price revision The removal of Pajingo from the production profile has a limited impact on our earnings forecasts, with our FY17E to FY19E reducing 7% to 5%. Price catalyst

12-month price target: A$3.00 based on a Blend of 50% 1.4x NAV and 50% 6x CFPS methodology.

Catalyst: Delivering further upside at the Edna May underground would be a positive. We already factor in the Stage H cutback at Cowal but believe recent drilling results suggest there is likely to be incremental upside in higher grades and better strip ratio. Action and recommendation Upgrade to Outperform. FY16 marked a transformational year for EVN, integrating two new core assets. The sale of Pajingo demonstrates the company’s commitment to its strategy of portfolio optimisation. Whilst we wouldn’t discount further acquisitions or divestments, we believe the company will focus on asset optimisation in FY17.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.