Australia has, for some time, had a large external vulnerability.

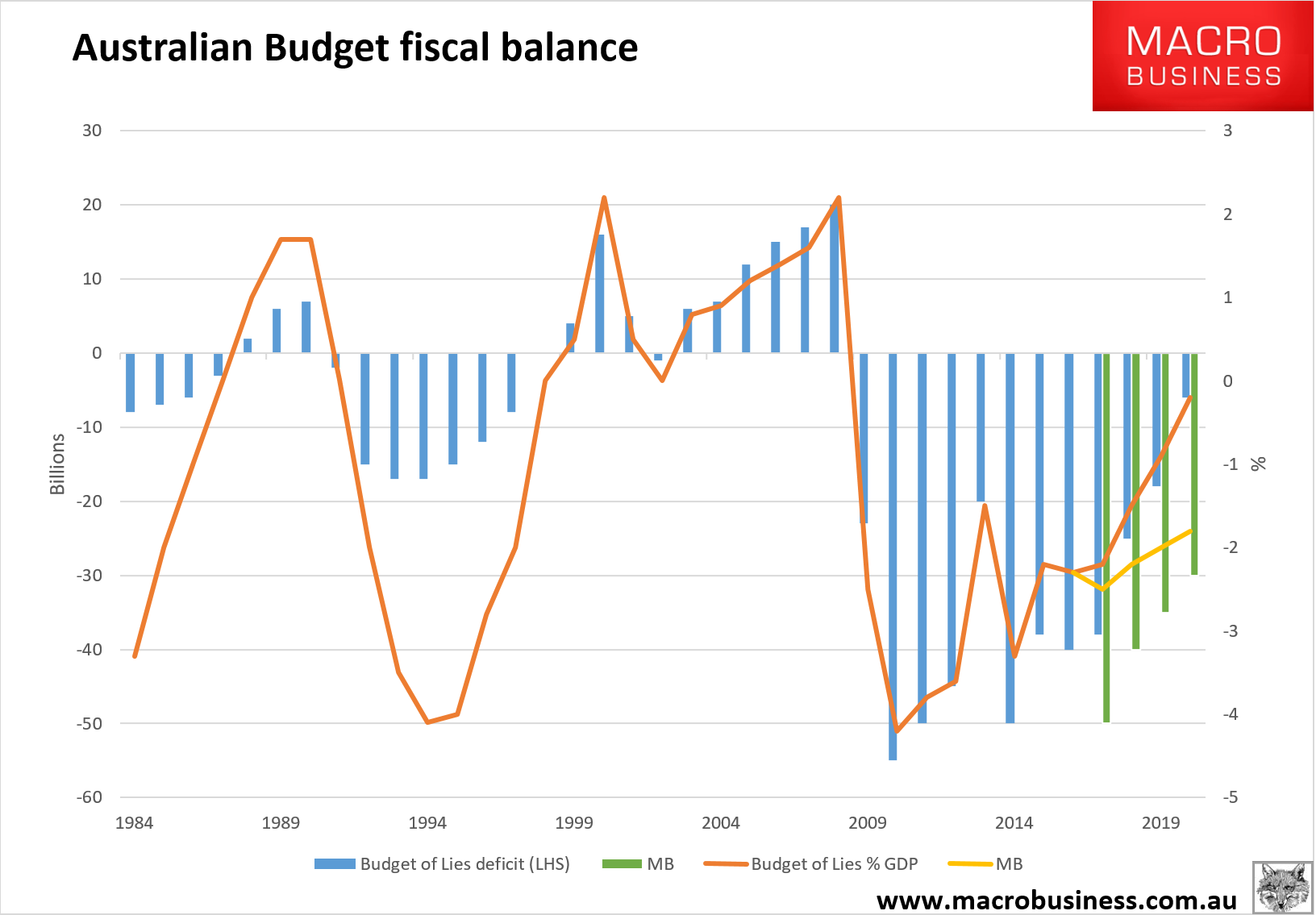

We believe without strong fiscal policy decisions the return to surplus will be slower and may push out to 2021.

Parliamentary gridlock, particularly in the senate has slowed the process and we don’t see that ending any time soon.

Some quotes from today’s S&P conference call. On the economic model:

On the fiscal deficit:

We’re looking at the government to stick to its current forecast for a return to budget surplus, which is around 2020-21.

There have been a number of years with fiscal slippage and it’s really time for the government to step up and deliver on what they’re saying.

On borrowing offshore for house price pumping:

Advertisement

Is increasing house prices the best use of … capital?.

There are better and more productive uses of capital in the economy.

On the impact on bank capital:

Around $7-$8 billion would need to be raised each to offset a downgrade, which we see as unlikely considering the banks are already well capitalised.

I’ve got some news for S&P. There is zero chance of Australia returning to a Budget surplus in 2021 once realistic commodity price forecasts are plugged in:

In fact, MB can confidently predict that Australia will never see a fiscal surplus again unless the nature of the budget is radically transformed from one that sucks in resources income, redistributes it via various tax giveaways, and amplifies the impact on growth by orienting that largess towards house price speculation and consumption. That model by definition requires more offshore debt to support incomes while commodity prices fall and will require yet more debt afterwards, both public and private.

The budget surgery required is not only daunting in terms of the shifting of revenue and spending quantities, it is outright radical in terms of spending qualities. Recent negative gearing reform debate is the tip of that iceberg:

- housing subsidies must get the chop and prices fall (in either real or nominal terms);

- the entire economy must be made competitive so that income generating tradable sectors rise and offshore debt borrowing sectors subside;

- productivity must be placed at the centre of everything.

When you look at the makeup of the propertocratic Parliament you get some idea of how laughably distant we are from any of these outcomes. And remember that the transformation itself will take years and years.

Many downgrades lie ahead.