Salt: You don’t have a house ’cause you are lazy

KPMG’s Bernard Salt has continued the war on youth, posting a diatribe today claiming that young Australians cannot buy homes because they are lazy. From The Australian:

Fairy tales too are extraordinarily popular with some…

This is the idea that the reason you don’t have a house isn’t because of a lack of effort on your part. It’s not even because of the way the system is structured…

The reason why you don’t have a house, my lovely, is because a greedy ogre has gobbled up all the housing and has left nothing for you. We call this ogre “baby boomer”.

What is required of course is a transfer of sorts from the greedy-ogre baby boomer to the sublime-innocents who follow.

Even I like the creative ingenuity of this fairy tale.

It explains why I don’t have a house; it asks no question about effort, application and sacrifice on my part; and it promises personal enrichment.

Why would the sublime innocents ever question this logic; it is not in their interests to do so. And it feeds into another intrinsic human demand for consumerism and hedonism.

“If greedy baby boomers have gobbled up all the housing, then I am entitled to travel overseas and have a great time”.

…baby boomers will continue to suffer in silence the jibes of those who to them seem unwilling to make the sacrifices that they made to buy a house… baby boomers are too frightened to speak their mind about the sacrifices required for home ownership.

This is the typical baby boomer view of housing: the myth that they “sacrificed” for home ownership but the current younger generations are unwilling to do so.

Of course there’s no mention of the fact that it is so much harder and more expensive to purchase and pay-off a home than yesteryear. This was spelled-out in no uncertain terms by the 2016 Household, Income and Labour Dynamics in Australia (HILDA) survey, released last week.

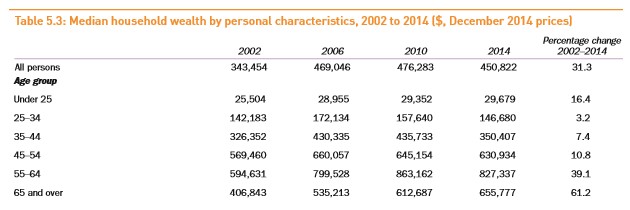

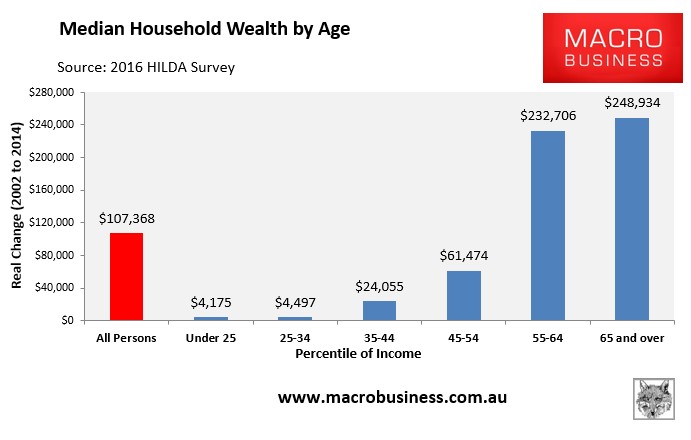

The HILDA survey revealed a rapidly growing wealth divide, whereby median wealth over the period 2002 to 2014 increased by 61% for those aged 65 and over, and by 39% for those aged between 55-64, but rose by just 3.2% for those aged between 25-34 and by only 7.4% for those aged between 35-44 (see below table).

In dollar terms, the oldest two age cohorts – 65 and over and 55-64 – experienced a massive increase in real wealth of $249,000 and $233,000 respectively over period 2002 to 2014, whereas under 25s experienced an increase in real wealth of just $4,175 and those aged 25-34 years old just $4,497 over the same period:

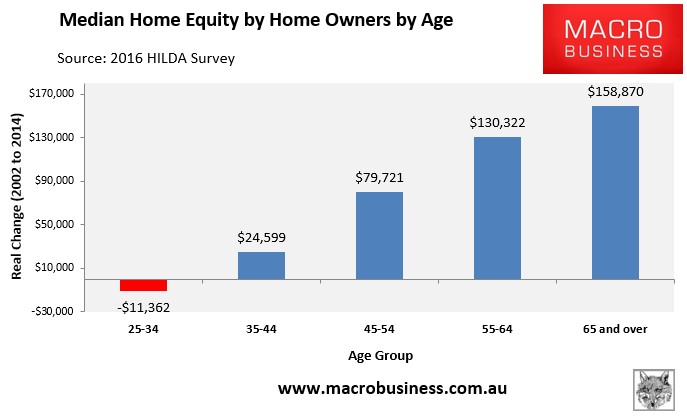

Of course, the fundamental driver of the gulf in wealth between the generations is rising home values. As shown in the next chart, the older age cohorts experienced huge increases in home equity, whereas 25-34 year old’s home equity actually went backwards over the period 2002 to 2014, due in no small part to the huge rise in mortgage debt:

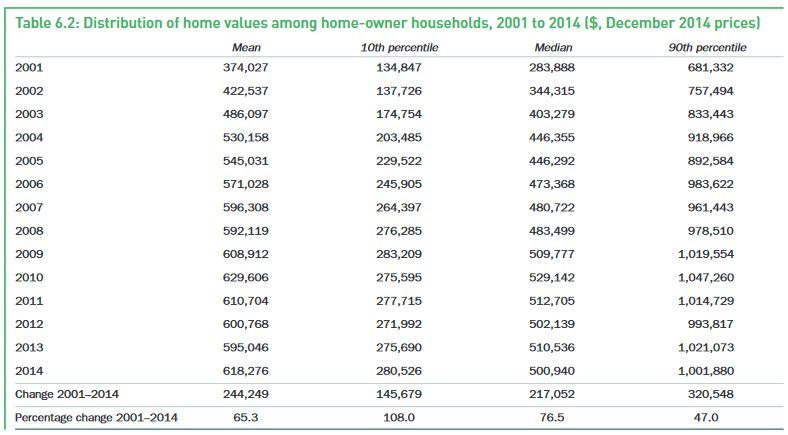

Meanwhile, entry level homes skyrocketed in value between 2002 and 2014, making home ownership far more difficult for younger Australians. As shown in the below table, the 10th percentile of homes – i.e. the cheapest homes on the market – grew in value by 108% between 2001 and 2014, compared to 47% growth for 90th percentile properties at the top of the market:

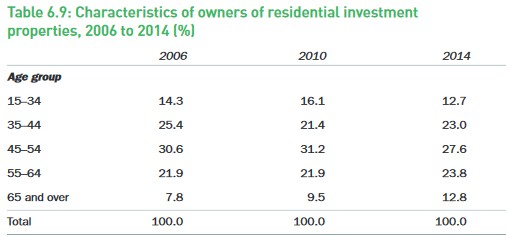

Further, the older cohorts – the baby boomers – increased their share of investment properties, thus helping to shut-out younger Australians from home ownership:

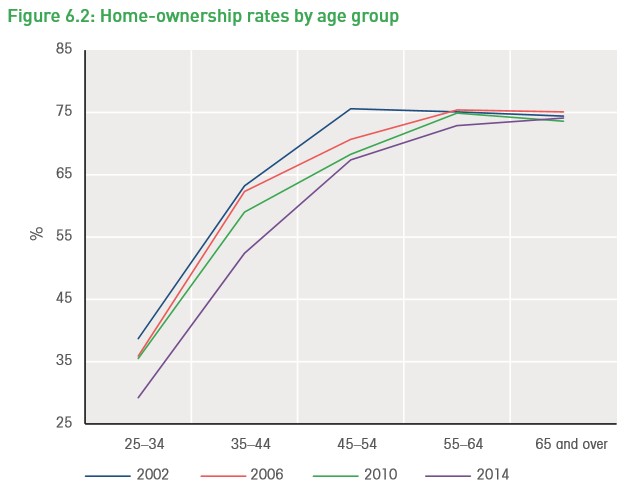

The net result is that home ownership has crashed amongst the younger generations, whereas the baby boomers have held firm:

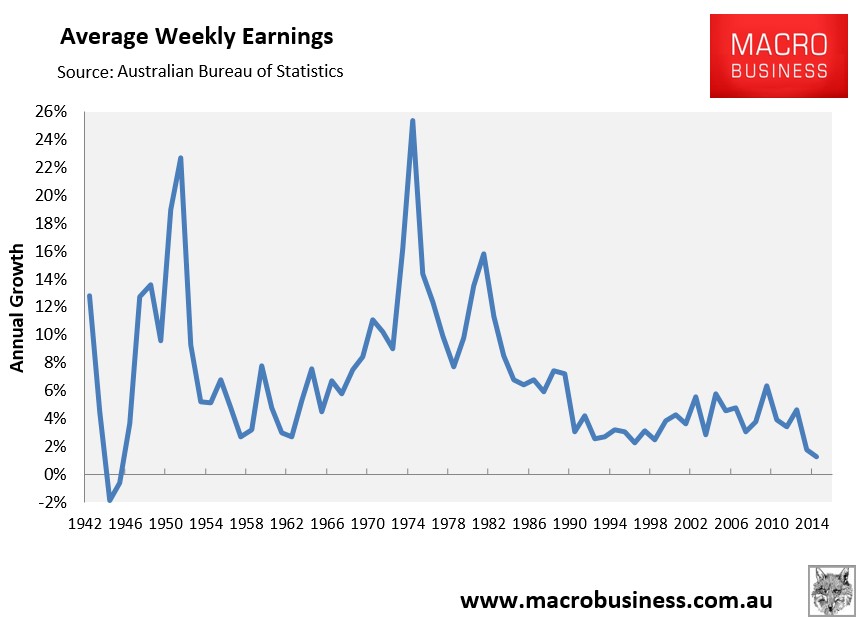

The classic retort is that nominal mortgage rates are so much lower these days. This may be true, but average earnings growth is also tracking at its lowest level since World War 2:

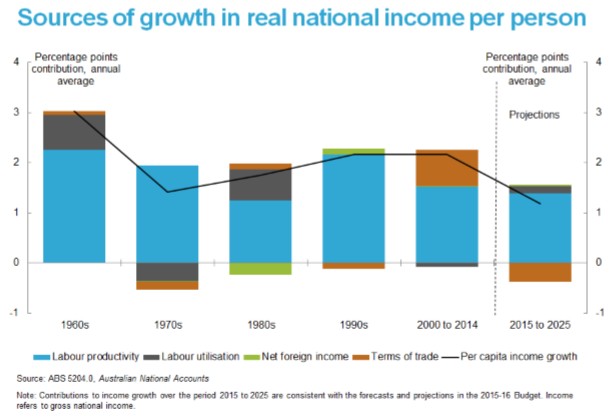

And average income growth is expected to be the weakest in at least 60 years over the coming decade, according to the Australian Treasury:

The net result is that it is not only very difficult to purchase a home, but it is also going to be far more difficult for today’s mega-mortgage slaves to pay off their loans. A huge mortgage today will remain a very big mortgage in a decade’s time thanks to anaemic inflation and wages growth.

In short, the collapse in home ownership has nothing to do with younger Australians being “lazy” and unwilling to make “sacrifices”, but that it has become structurally much harder to both purchase and pay-off a home.

The data lays this out clearly for all to see, if only baby boomer commentators like Salt would dare to look.

unconventionaleconomist@hotmail.com