An inconclusive Federal election result delays and compromises the prospect of a fiscal kick to an already flagging earnings cycle for the ASX 200. The potential for a minority or hung parliament leaves instability as another headwind to intentions and confidence.

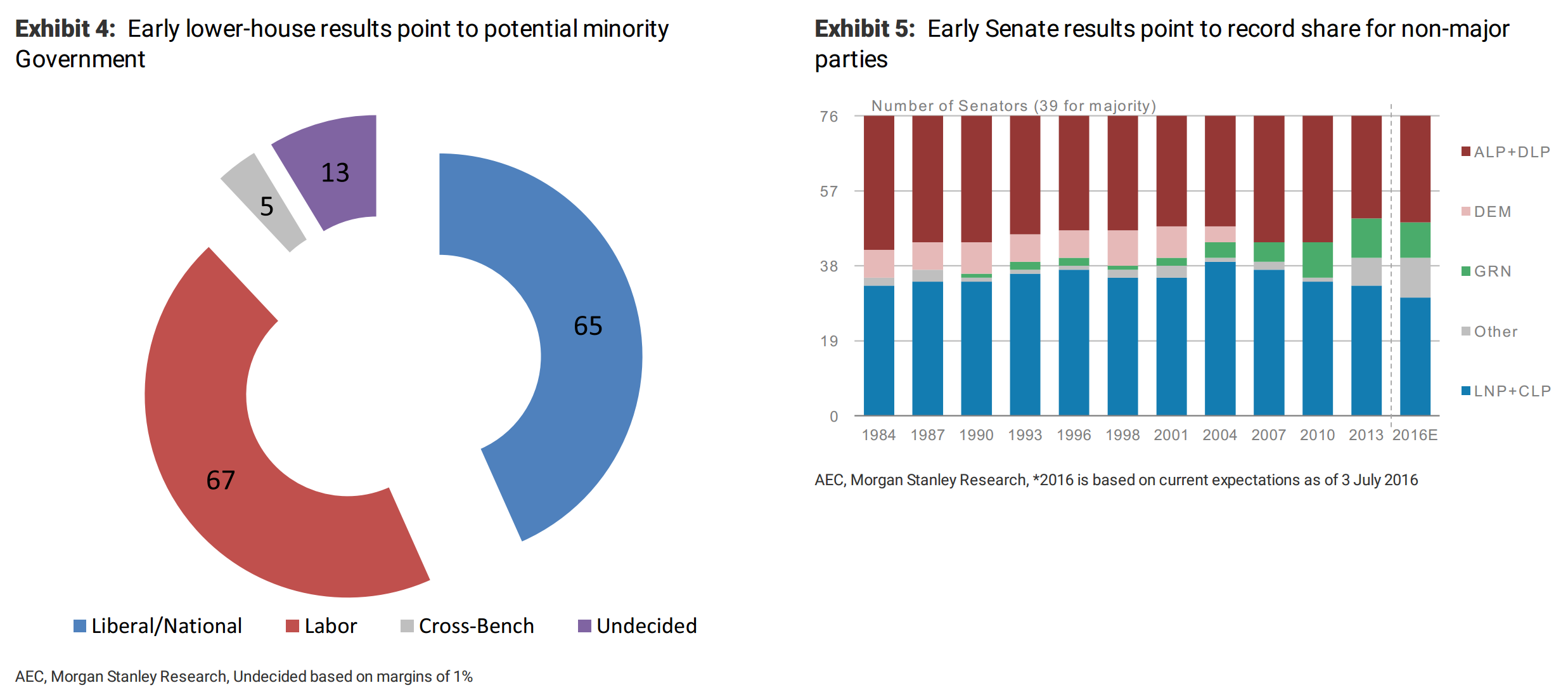

Election outcome not known: Saturday’s Federal election has failed to deliver a clear victory for either party,and the final composition of the lower house may not be known until postal votes are fully counted (Tuesday at the earliest, but potentially into the following week). Meanwhile,early Senate results suggest a makeup equally as unwieldy as the prior, that will leave whomever forms government to deal with multiple small parties and independents. We had flagged the need to prepare for an in conclusion, but we expect this result will come as a shock to the market because of the likely coalition.

Falling chips: Based on media reports (e.g., the ABC), we see three scenarios for government from here, in order of likelihood: 1)Liberal-National Coalition government,either in narrow majority or minority,2)Labor minority government with the support of a number of cross-benchers,and 3) Another election – in coming weeks if neither party can form government, or coming months if it proves unworkable with the new Senate. The result will depend on whether postal votes follow their historical pattern of breaking for the incumbent government, but if the Coalition fail to secure the 76 of 150 seats then both parties will rush to secure independents’ support, in the hope of being invited by the Governor General to form government.

More work for the RBA ahead: We believe the election outcome diminishes the prospect of a smooth legislative agenda, leaving fiscal policy options constrained. Uncertainty and instability associated with a more fragmented Senate will likely weigh on consumer sentiment and business confidence – potentially impacting hiring and investment plans. Along with the projected impact of the UK’s ‘leave’ decision on global growth, we believe the RBA Board has an even stronger case to adopt an easing bias on Tuesday and cut rates in August, with the potential they move directly to a cut.

Implications: We retain our cautious stance towards ASX 200 Index returns. Ultimately fundamentals around earnings and valuations will matter and these remain stretched. We think domestic cycle linked earnings are heavily reliant on a fiscal boost to broaden out activity levels as the resource unwind extends and the housing slowdown begins. Such a stimulus seems at best delayed and potentially permanently compromised should a fiscal impasse emerge as last seen in 2010 to 2013.

I will add that if the nation is forced to another election then Labor will surely win in a landslide.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.