As we all know, there is no reason for the Chinese yuan to fall and it isn’t except in its rampant devaluation against everyone. Soc Gen today asks just how low this non-fall is going to go:

A New Normal for the RMB

We revise our peak forecast for USD-CNY to 7.10 from 6.80. Similar to immediately following the August devaluation, consensus is too complacent on the ability and willingness of policymakers to arrest the nearly three-year-old depreciation trend.

The new normal in recent months is gradual RMB depreciation that doesn’t create a negative feedback loop to other currencies or broader market sentiment. This could embolden policymakers to keep pushing the limits of depreciation, especially if speculative positioning stays subdued. Implied volatility, risk reversal, forward points, and the forward curve have all been unresponsive to the recent RMB weakness. This is partly due to the reluctance of speculative investors to add exposure after being burned by the RMB depreciation trade in January, but also because intervention remains ongoing despite not showing up in headline reserves or the forward book.

The best solution remains for policymakers to let the RMB find its market clearing price. This is not an exact science and we can only guesstimate what the level would be – 6.80 was our previous assumption but 7.10 now seems more realistic. The recent depreciation at a time when the dollar has not been strengthening suggests policymakers are increasingly giving in to capital flow pressures and are willing to the test the limits of depreciation. Further depreciation could reinforce capital outflows in the short term but should eventually help capital flows reach equilibrium.

7.10 peak – our base case, 80% probability

The next wave of RMB depreciation will see USD-CNY trade up to 7.10 by mid-2017. Since USD-CNY bottomed in early 2014, there have been five waves of depreciation and each has followed a predictable pattern: three to five months of USD-CNY increasing (+3.5% on average), followed by modest gains (+1%) spanning an equivalent time span, before another round of depreciation ensues. The predictability is suboptimal from a policy perspective, but it appears to be the PBoC’s standard playbook. While there could be some consolidation or modest strength after the current depreciation phase ends (3.6% since April), the ensuing wave and medium-term path should see USD-CNY reach 7.10 over the next year.

Cumulative depreciation of 6% over the next year would be similar to what has been experienced since October. This would not be an atypical base case for a country in a structural slowdown, with perceptible credit and banking sector risks, an imbalance in the supply-demand of capital, a tenuous reserve adequacy position, and local residents harbouring a strong desire for FX diversification.

We continue to believe that consensus is underestimating the chances of CNY depreciation, both from the ability and willingness of policymakers to prevent further depreciation. Consensus is at 6.80 in one year, which was our prior out-of-consensus call immediately following the August devaluation (back in late August consensus was at 6.50).

A gradual and controlled depreciation with periods of stability and bouts of accelerated weakness is still the most likely scenario (80% probability). A move to 7.10 may continue to be absorbed by investors without disturbances to broader market sentiment occurring, and as such we see no need to revise our EM forecasts, which currently entail modest spot depreciation that broadly matches the forwards.

Importantly, the USD-CNH trading pattern since 2014, of only retracing a portion of its gains and never revisiting the lows after an up move, should remain in place. Coupled with little fundamental justification for a stronger CNH over a 12-month horizon and fairly neutral speculative positioning, it is unlikely that USD-CNH will trade below the 6.50-6.55 area.

8.0 – the new risk scenario, 20% probability

Back in January (CNY7.50 World) we identified USD-CNY trading up to 7.50 as the risk scenario for the currency. Given ongoing capital outflows, the ability of the market to absorb recent depreciation without negative consequences, the policy decision to weaken the renminbi when the USD has been stable, and our new forecast of 7.10, the risk scenario for CNY is now much higher.

The new risk scenario for CNY is 8.0 (20% increase in USD-CNY). We assign 20% probability to this scenario. The caveat is that the pain threshold for the market appears to be much higher than before and the implications for the global financial markets will primarily depend on the speed of depreciation. We believe that it would take significantly more pressure on capital flows than what we have seen over the past few years, or an economic hard landing, for our risk scenario to unfold. Note that we have a 30% probability of a hard landing of the Chinese economy. We think that an economic hard landing might not necessarily trigger a sharp devaluation, as the authorities would most likely respond with strict capital controls amid concerns over capital flight.

Within the risk scenario, the path to 8.0 could be abrupt (not likely), slow (more likely), or fast (most likely).

Scenario 1: one-off devaluation (<10% probability): A one-off move (i.e. step devaluation) where the PBoC then chooses to defend the new level. There would be enormous political backlash with the appearance of any active pursuit of devaluation. This would also be too risky for Beijing’s taste given that no one can say for sure how much depreciation is enough to equilibrate supply and demand. However, we assign it a nonzero probability because the authorities might ultimately decide it is the best way to realign expectations and halt domestic capital outflows.

Scenario 2 (free float over the next year – >70% probability): The PBoC fast-tracks currency reforms through a big-bang approach to currency flexibility because either: a) capital outflows remain large and the depletion of FX reserves too great; or b) it deems the domestic and global financial markets able to absorb the shock.

Scenario 3 (slow and steady move – 20% probability): The current strategy of steady depreciation picks up pace and intervention is used to limit overly destabilising volatility. The risk to a steady creep higher in USD-CNY is a build-up in speculative pressures and resident outflows that creates a vicious cycle of depreciation.

We can break up the impacts of this into five categories:

political, as it provides a free kick to anti-globalists everywhere, with Donald Trump the next cab off the rank;

trade, as Chinese competitiveness rises everyone else will have a new excuse to devalue (we can see it already coming in Japan);

monetary, as it creates a new wave of deflation for commodity prices in everything from gas to copper to iron ore as Chinese production slams into seaborne imports;

capital flows, as it accelerate both capital flight and efforts to stamp it out creating turbulence for global assets markets, and

rebalancing stalls, given this is inherently a shift of losses in the banking system to the household sector versus the external sector.

Advertisement

For Australia, if we reach 7.1 USD/CNY then what was floor price of $40 where Chinese iron ore drops out big will drop to $33.50. If we reach 8 USD/CNY then that same figure will drop to $29. This is how Australia enjoys the final leg in its iron ore bear market right down into the teens.

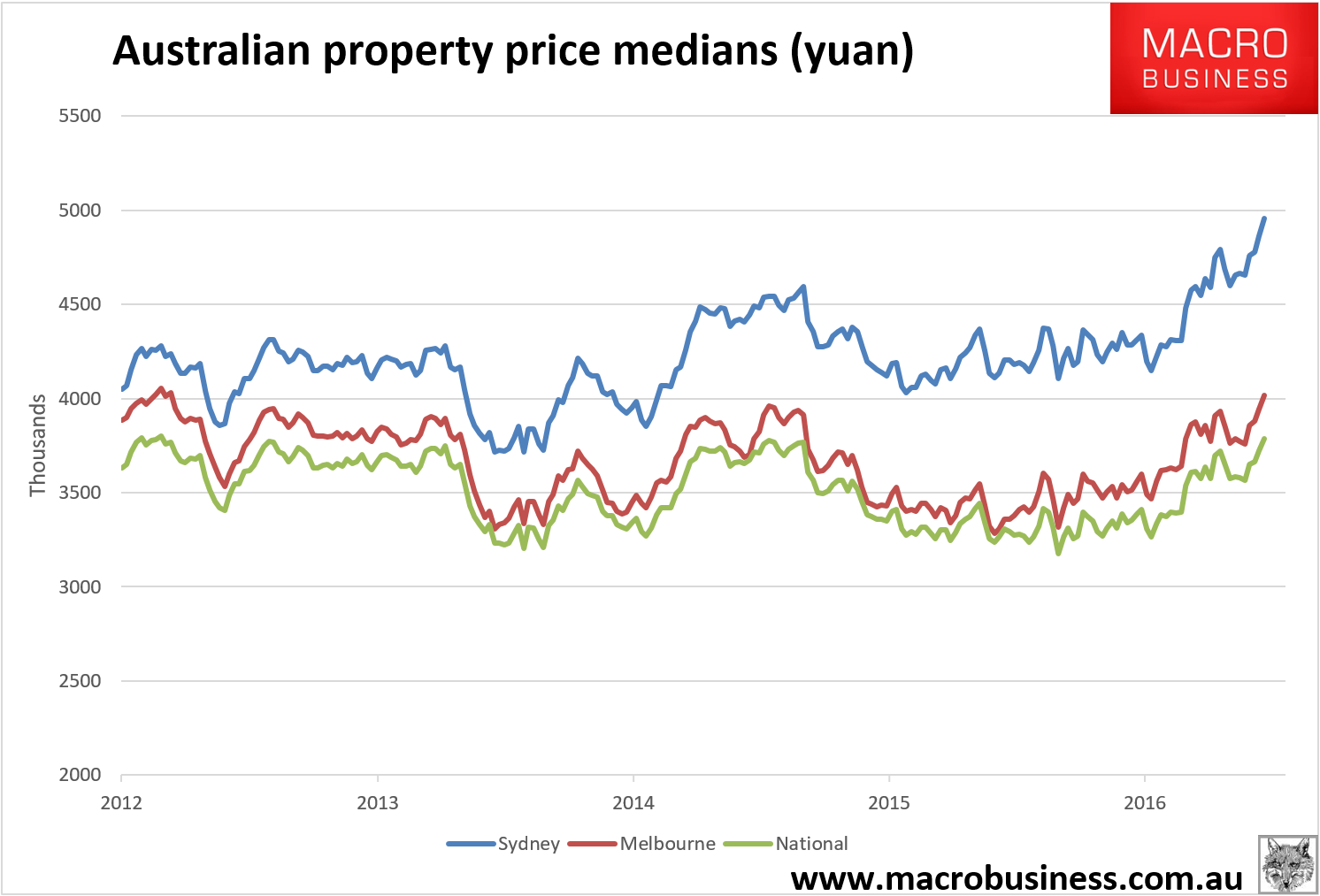

The second front will be the shift in yuan denominated Australian property prices which will rise more quickly:

Advertisement

That will bring forward demand at the expense of later.

We can expect the Aussie to drop as well though perhaps not enough to outpace the yuan given it is falling even faster against the basket than it is the USD. Anyway, whichever way you look at it a falling yuan does more harm than good for Australia.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.