From the Ministry of Dirt (A.K.A. Office of the Chief Economist, Department of Industry) today in its Resources and Energy Quarterly:

Forecast weakness in iron ore prices is expected to put downward pressure on Australia’s iron ore export earnings, despite robust growth in volumes. Australia’s export volumes are forecast to reach 852 million tonnes in 2016–17, up from 748 million tonnes in 2014–15, as large Australian mining operations increase their global market share in an environment of weak demand.

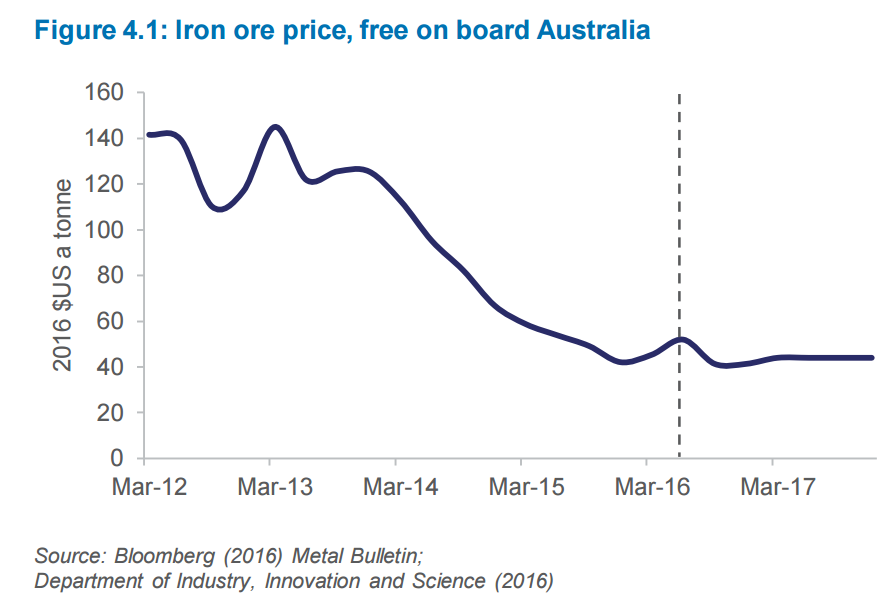

Iron ore spot prices were highly variable in early 2016, led by speculative activity on the Dalian Commodities Exchange in China. The volume of iron ore futures trades on the Dalian Exchange grew rapidly in early 2016—with daily traded contract volumes exceeding half a billion tonnes on 32 occasions between February and April. The spot price for a tonne of iron ore (FOB Australia) traded as low as US$40 a tonne and as high as US$66 a tonne over this three month period.

The iron ore price averaged US$48 a tonne in the first six months of 2016, down 13 per cent year-on-year. Despite the large movements in prices, the market fundamentals are broadly unchanged—demand growth is slow and the market remains well-supplied. With the expectation of weak growth in consumption and stronger growth in supply, prices are forecast to moderate over the remainder of 2016. For the year as a whole, the iron ore price is forecast to decline by 11 per cent to average US$45 a tonne.

In 2017, iron ore prices are expected to recover more slowly than previously forecast. On average, iron ore is forecast to be US$45 a tonne in 2017, representing no change from 2016. The revision is based on the assumption that loss making operations may continue to produce for longer than previously expected. It also factors in increased supply from India and additional cost savings reported by iron ore producers.

The outlook for iron ore prices is sensitive to the length of time that companies can operate at a cash loss. As financial losses accumulate there will be greater pressure to close high-cost capacity.

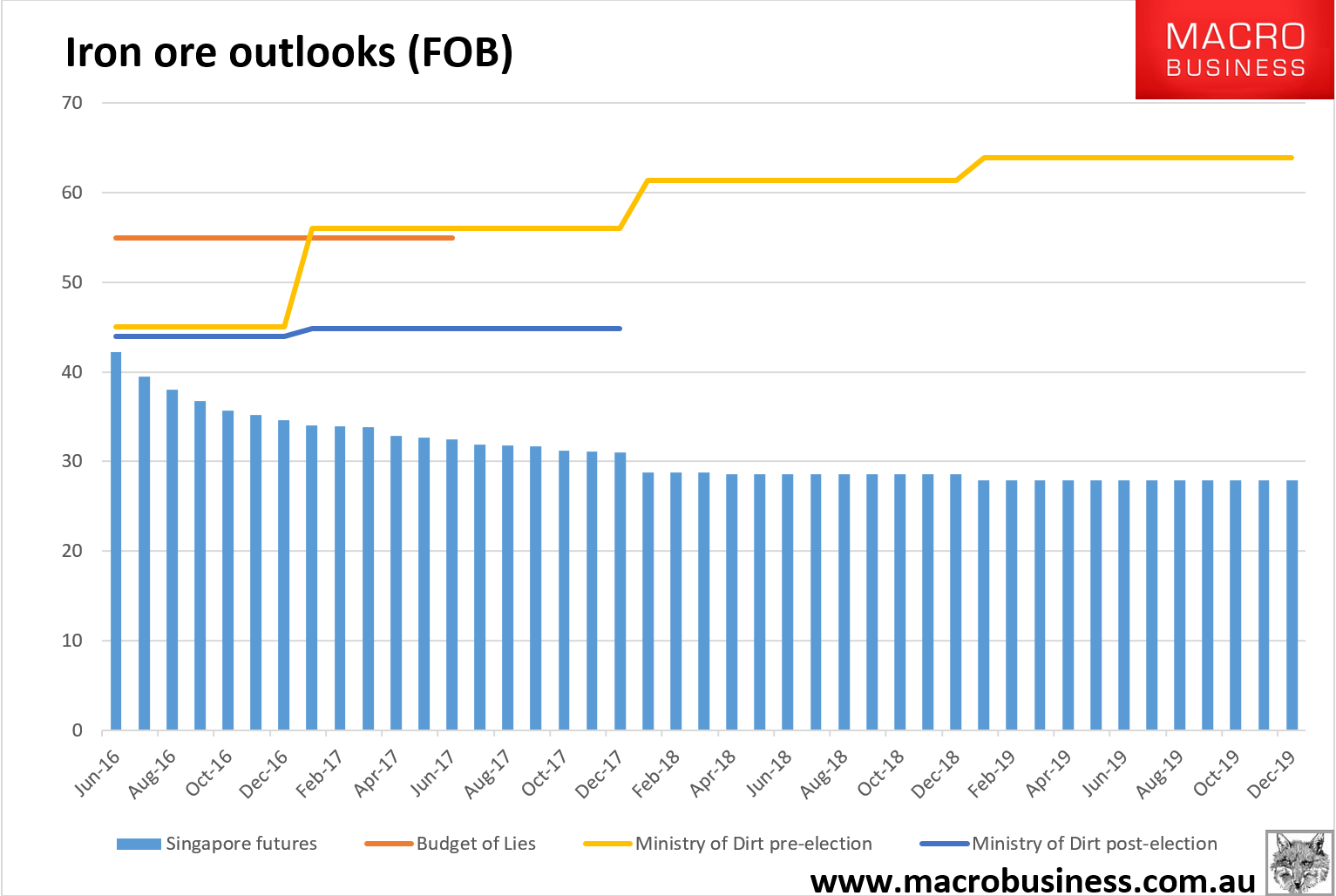

It’s time to shut the Federal government’s commodity price liar, the Office of the Chief Economist in the Department of Industry. It is doing the nation great harm.

Before the Budget and election this year, the Office released ridiculous forecasts for iron ore prices that gave cover to the Treasury in upgrading its own price outlooks:

Advertisement

This lead directly to a corrupted Budget process in which fictional forecasting numbers were allowed to substitute for prudent fiscal policy through the terms of trade crash.

Given this was an election budget as well, it debauched the entire basis upon which the election was fought, allowing first the Government and then the Opposition to pretend to policies that they have no hope of delivering.

Advertisement

All of this was confirmed on Friday by the Office when it downgraded its iron ore outlook -20% below its March quarter projection even though virtually nothing has changed in the most reliable futures market in Singapore.

This is either ineptitude on a grand scale or simple control fraud and either way the implication is very obviously that the Office should be shut immediately. Treasury can instead rely on futures pricing or Bloomberg analyst averages (around $40).

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.