…if you think about Hockey’s [superannuation] proposal in terms of what it would do for housing affordability, it doesn’t add up. It is, indeed, a “thought bubble” that would promote a property bubble if ever adopted.

The problem is that tinkering with the property market in this way would only serve to artificially inflate demand for property and therefore push up house prices even higher than where they are now.

Such as policy would have a similar distortionary effect as the first home owner grant and exacerbate housing unaffordability.

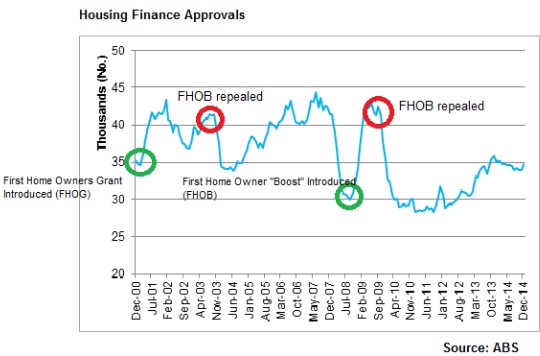

The problem with the first home owner grant, when it was first brought in, and for subsequent boosts, is that house prices were almost instantly lifted beyond the value of the boosts. While the grants were intended to improve affordability, they had the opposite effect. The chart below highlights the impact of the grants on housing prices…

With Sydney vendors now asking for over $1 million for a house, a 10% deposit on a Sydney home, if raised through super, would erode almost entirely the retirement savings of most people in that age group [20s to 30s]. Is Hockey even familiar with house prices and average super balances?

We are of the belief that the less government intervention there is in the property market, the better. Governments all round should be doing more to promote housing affordability, not unaffordability.

Reducing negative gearing, a highly distortionary policy, would have a far more beneficial effect on promoting housing affordability. If negative gearing was repealed or altered, investors who are now gobbling up property would back off buying houses, which is what those who are demanding lower dwelling prices want to see. We know Joe was at least looking at negative gearing last year and we strongly encourage him to reduce or eliminate negative gearing. For starts, he would potentially save over $5 billion a year on the budget!

According to the Australian Bureau of Statistics (ABS) first home buyers accounted for just 14.5% of total owner occupied housing finance commitments in December 2014. This compares to around 50% for investors. It’s investors who are doing the heavy bidding at auctions, and with interest rates falling, that trend will continue through 2015.

So, if anything needs to be done, it is to eliminate existing distortions, and not introduce more.

Well said. You can subscribe to SQM’s free weekly newsletter here.