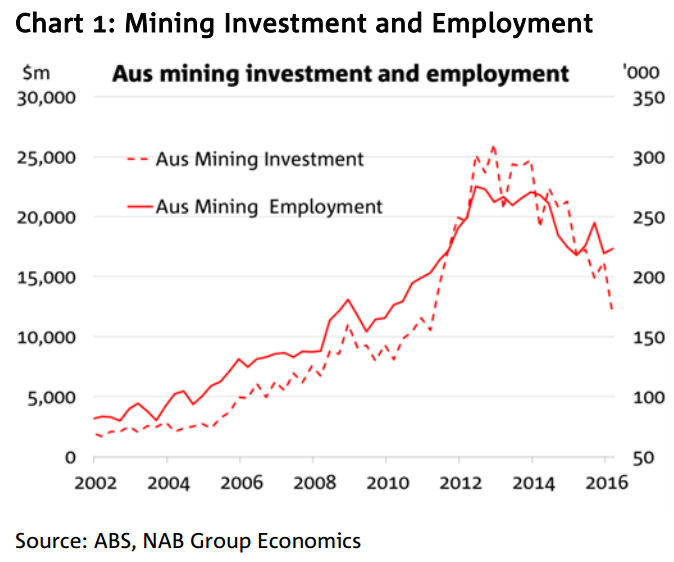

More than half way through the mining investment downturn

The economic significance of Australia’s once in a generation mining boom has not been lost on most people. China’s seemingly insatiable demand for commodities and the determination of major mining firms to meet this demand before their competitors – seemingly at any cost – saw unprecedented levels of mining investment and commodity exports supporting Australian growth during a very difficult time in the global economy. However, this situation was never going to last indefinitely, and a combination of slowing demand from China and increased commodity production saw bulk commodity prices peak in late 2011. Mining firms’ enthusiasm for investment also began to wane as the financial viability of new projects declined along with commodity prices.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.