From a prozac-popping Jessica Irvine:

Never underestimate the ability of journalists and politicians to put a gloomy spin on things.

On the eve of an election, it suits incumbent governments to spread it about that there is trouble afoot on the economy. Don’t risk a switch to the other guys!

It suits journalists to find the cloud inside every silver lining, too. We sell more newspapers that way, which, in a way, is your fault: you’re more interested in buying bad news than good.

So, at risk of your eyes glazing over, I must tell you that this week’s news on the economy was unadulterated good.

Sorry chicken littles, the sky is not falling in on the Australian economy.

Nobody said the sky is falling, Jessica, that’s a silly and polarising “straw man”, quite beneath your usual standard.

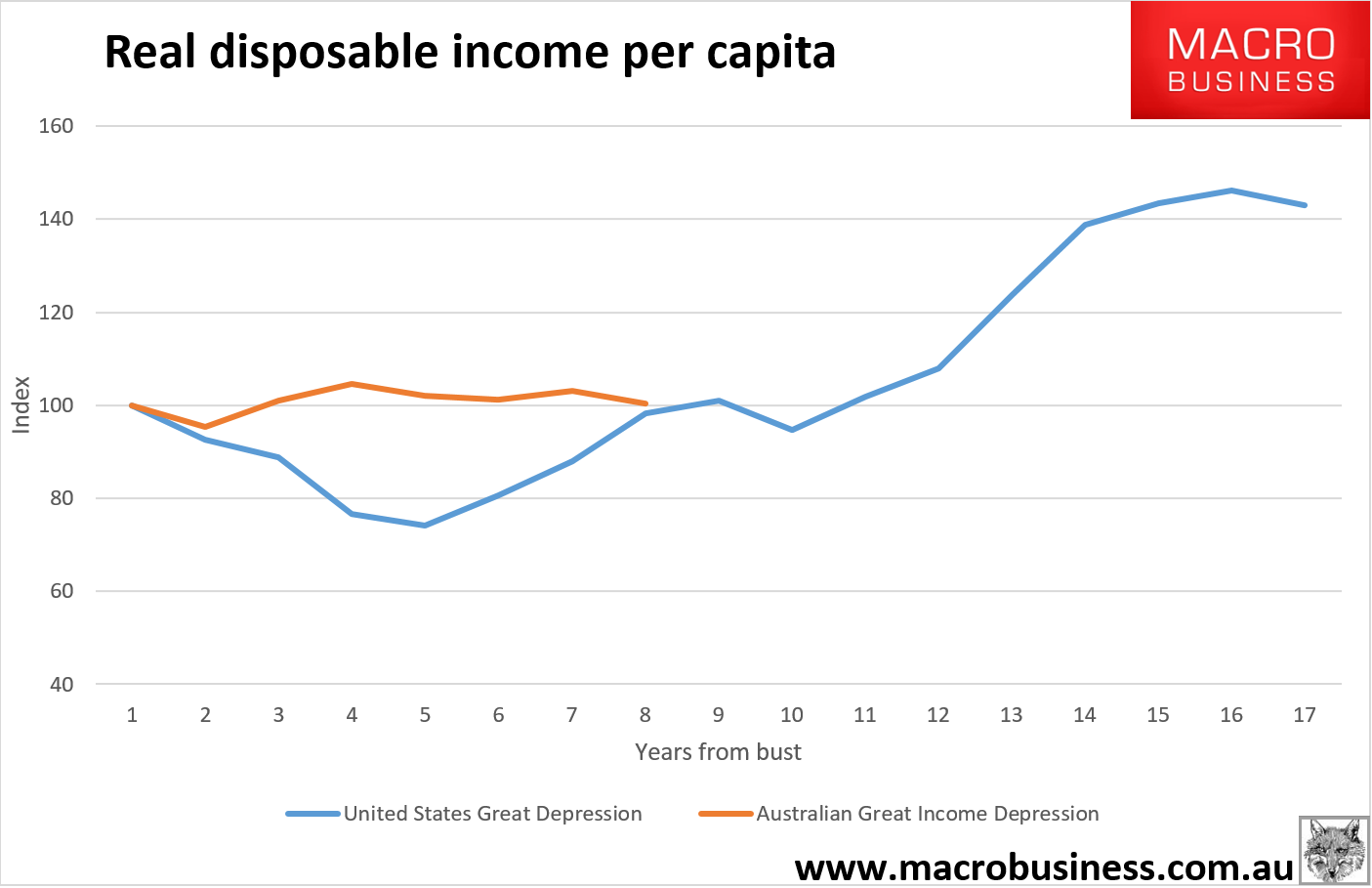

Last week’s data was more evidence of the ongoing grind lower in Australian living standards that has been running for eight years. According to the Australian Bureau of Statistics, the metric real per capita national disposable income is “considered a good measure of progress for living standards because it is an indicator of Australians’ capacity to purchase goods and services for consumption”. Here’s what Australia’s RDI per capita looks like since 2008 versus the United States experience of the Great Depression of the 1930s:

Thankfully, Laura Tingle took our Jessica to the woodshed:

No-one is at all sure of what awaits whoever wins the election in the Senate. But more significantly, both sides of politics know both that there is no great prospect of things being really fabulous economically in the next three years, and that neither of them have really been able to find a miraculous answer to the elusive search for more growth, and more jobs.

There is the spectre of a credit rating downgrade on the other side of July 2 and a re-booting of the whole debate about the country’s fiscal position. There is more readjustment of the economy from the resources boom to the non-resources economy. There is more skimming along the bottom of a deflationary cycle that the political cycle hasn’t yet fully learnt to adjust to.

…Neither side has got the wherewithal to actually do anything about declining living standards felt by voters. And they don’t even have much scope to do anything about lifting the activity and production which might eventually help stop the decline.

The Coalition’s ‘plan’ rests entirely on its $50 billion, 10-year plan for a company tax cut. At the halfway point through the election campaign, the plan feels as much a liability as an asset.

The government’s forecasts of the growth it would generate – and of the impact on the budget bottom line – have started to look a little sick as they have been unpacked.

…But the truth is that, for its part, Labor doesn’t really have a growth plan either.

It talks of ‘inclusive growth’ coming from a community that is better educated (thanks to Labor’s education spending plan) and healthier (thanks to Labor’s health spending plan)

But it can’t really answer voters questions either about how to make the economy grow faster – or more correctly, how it can boost national incomes and, along the way, the incomes and sense of well-being of voters.

…It is the dirty little secret of the campaign which both sides know they will have to confront if they win on July 2.

Exactly. Journalism has only one role and it is to expose the lies of government. Richard Denniss also showed the way:

Optimism is a central part of the Coalition’s political strategy. When the economy is going well it cuts taxes for business and high income. When the economy turns down and budget revenues shrink it cuts spending for the services people on low and fixed incomes rely on. The “right wing ratchet” means that taxes should only ever go down and spending should only ever go down. The only thing up for grabs is the timing.

…Step one: be optimistic. Despite his government now borrowing the same $100 million per day that caused a “budget emergency” when the ALP was in power, and despite the fact that unemployment has risen, the Coalition is trying to assure the public that everything is OK. Indeed, Trade Minister Steve Ciobo said on Q&A this week “the fact is that as a nation, on any objective measure, what I’m saying is Australia isn’t doing too badly and things aren’t all rotten”.

Step two: tell everyone that things are looking pretty good, but that if we cut taxes they will look even better. But the Prime Minister has discovered that his task of selling the benefits of trickle-down economics is a lot harder than Costello or Colin Barnett’s simple task of cutting taxes in the middle of a boom.

…Step three in Turnbull’s plan is proving even harder than the second. He has to explain to a sceptical public why, if cutting the tax rate for business is such a good idea, we should wait 10 years to do it.

…Cutting the corporate tax rate is not a “plan” for jobs and growth, it is a hope that the economy will pick up in the next 10 years. It is up to us whether we invest more money in education or infrastructure or give away billions in tax cuts. The world economy doesn’t care one way or the other, but in 20 years’ time we probably will.

As did Alan Mitchell:

It is the fall in the terms of trade that has driven the wedge between real GDP and income growth, which in turn is fuelling the slow-burning fiscal crisis in Canberra.

…Caught unprepared, the two major political parties have shuffled through leaders and strategies to boost growth and get the budget out of deficit, nearly all of which have failed the basic tests of political acceptability.

Malcolm Turnbull, who calls himself the leader of a reformist government, is still struggling to pull together a strategy that is both workable and politically sustainable.

Australian voters strongly oppose paying more tax, but are equally unwilling to accept any reduction of government services. If anything, the debates over child care and school education reform suggest that the demand for more and better quality government services has grown disproportionately with rising real incomes.

Having baulked at major tax reform, Turnbull now is sitting on the mother of budget sink holes: a state health funding gap estimated at almost $200 billion over the next decade and a half.

And Bill Shorten is sitting on the sink hole with him.

Both men are promising a relatively easy path back to budget surpluses based on the same forward estimates and, therefore, the same assumption that the states’ fiscal gap will be closed mainly by state government reform.

And Adam Creighton:

Both main political parties are rightly and routinely admonished for doing little to stem the rising tide of federal and state government debt, which has tripled to about 34 per cent of GDP over the past 10 years. But the spectacular ascent of private debt, which has doubled to about 160 per cent of GDP over the past 20 years, hasn’t rated a mention by either side of politics in this election.

…Almost all the increase in private debt since the 1990s has entailed households borrowing to buy houses to live in and (increasingly) to rent out. Ever lower interest rates and financial deregulation have fuelled a mutually reinforcing explosion of dwelling prices and debt.

“Australia’s household debt ratio has grown above peaks established in countries where housing bubbles formed and burst, as in Ireland, Spain and the United States,” say Philip Soos and Lindsay David, economists at LF Economics. “So highly leveraged is the housing market that even small declines in residential land prices will have adverse consequences.”

…Deutsche Bank recently calculated the ratio of average Australian weekly mortgage interest payments to weekly income had increased from a low of 53 per cent in September 2013 to 66 per cent in December last year. That’s higher than the 57 per cent average and comes despite exceptionally low interest rates. David and Soos blame the influence of what call they call the FIRE industry — finance services and real estate — for keeping the focus on public debt. “The FIRE sector has fuelled an immensely profitable land market bubble enriching its participants,” they say. But it is leveraged voters too, of course, who have a powerful vested interest in keeping debt high and rising.

The bigger problem is that the economy appears to require debt to grow more quickly than income to generate rates of economic growth that are considered normal. News of weak growth in lending aggregates is typically reported glumly by the media. But if such lending growth isn’t sustainable than neither is the economic system.

Even News.com got the memo:

QUITE some time has passed since your last pay-rise, and let me tell you, you’re not alone. Wages growth has been bad nationwide.

Skinny paycheques are spreading economic trouble, causing anaemic retail sales and falling overseas travel.

And yet. The new GDP figures were amazing. Australia actually grew as fast as China for a little while there (3.1 per cent growth in the last year and a startling 1.1 per cent in the last three months).

…It’s not just you and me working harder for the same money. It’s the whole country. How can a whole country take a price cut? The answer is the terms of trade, or the price of what Australia sell vs. what we buy.

…How low can they go? It’s frightening to think.

We don’t need them to stop falling, if all we care about is GDP. But if we actually care about incomes, and we want them to go up, the terms of trade become pretty important.

The one thing we must do is sell products the world will pay top dollar for. As a nation we don’t just have to churn out coal as its value tumbles. The way to stop the rot in our terms of trade is to move to high-value exports — and fast.

And today David Uren sees GDP sucked down with income before long:

Falling commodity prices have been depressing Australian national income for the past five years, but the March quarter national accounts show the income weakness has now spread across the economy, with non-resource profits falling and wage growth depressed.

The ABS reported last week that mining profits over the year to March were down 17.7 per cent (using the broad national accounts measure of operating profits), while profits across the rest of the economy were down 3.3 per cent. Eight of the 15 industrial sectors counted by the ABS suffered falling profits over the year.

Wage growth is also at a record low. The national accounts show average earnings per person have risen by only 1.8 per cent over the last two years. This is weaker than shown in the ABS wage price index and reflects that fact low-income and part-time jobs have been growing while high-income and full-time positions, particularly in the resource and construction sectors, are being lost.

These deflationary pressures have reduced the nominal growth rate in the economy to just 2 per cent, well below the budget forecasts that assume nominal growth lifts from 2.5 per cent in 2015-16 to an implausible 4.25 per cent next year. The nominal economy is the base for tax revenue collections, so the disappearance of pricing power across the economy means further big blowouts in budget deficits.

…The year ahead will see most of the remaining LNG plants and mining expansions completed, so the drag on growth from falling business investment in resources will come to an end. As these plants reach capacity, so too will the boost to growth from rising exports. The other big driver of growth — housing construction — is also likely to fade over the next year.

Slowly but surely the truth about Australia’s broken economic structure is emerging. It is coming out across ideologies and the media duopoly. That’s the first step in changing it for the better for our fellow Australians.