Opinion polls ahead of next week’s referendum have made a powerful move toward Brexit (Figure 1). Our attempt to clean up the polls for methodological issues suggests a lead for leave in the 3%-5%-pt range at the time of writing. Prior referenda suggest that a swing toward the status quo is often seen, both in polling over the final two weeks of the campaign and in comparing the result with final projections from the polls. In the Scottish independence referendum, for example, polls made a small move back toward remain ahead of the vote, and the eventual 10%-pt win for remain compared to an average projection of a 5%-pt win from the eve-of-vote polls. This time around, however, the swing toward leave appears to have accelerated as we moved into the period when we would expect status quo bias to show. Moreover the dispersion in polling results and controversy over methods suggests the margin of error around any estimate derived from the polls is high. In our view, it is now unlikely that the polls will offer clear guidance on the outturn of the referendum before the vote takes place. Hence here we update and summarize views on the economic, political, and policy implications of Brexit for both the UK and the rest of Europe, should it occur.

If the result is a vote to leave we would anticipate a 25bp cut in the Bank rate at the July meeting, followed by a further 25bp move alongside the August inflation report. The speed and magnitude of the response will be sensitive to moves in financial markets; the MPC likely would interpret a weaker currency as reflecting weaker growth expectations provided it is accompanied by weakness in other UK asset markets. The Bank of England has already planned emergency liquidity auctions and will stand ready to provide more if needed.

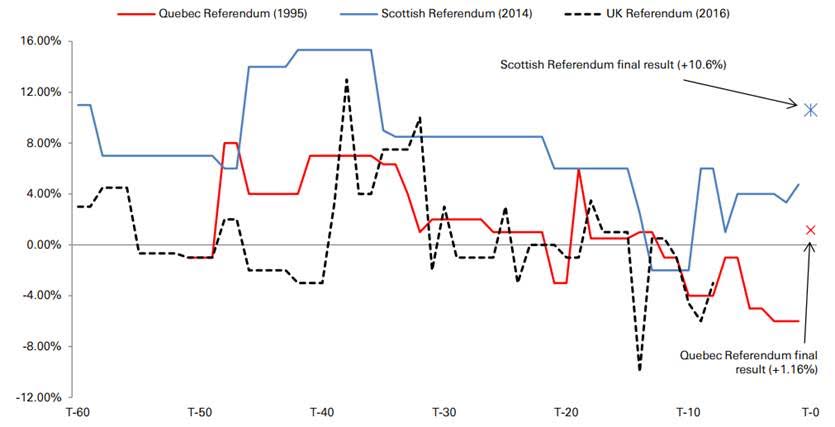

However, Deutsche explores previous secession polls in Scotland and Quebec and comes up with some reassuring logic:

From a highly dubious sample size of two, we can conclude that there is usually a late swing towards the status quo, which makes sense given the burden of proof is really on the “yes” camp so undecided voters will tend to vote “no” at the last minute.

Advertisement

Thus Brexit may need a polling lead of 6% plus this coming week to have a chance of getting up.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.