From Domainfax:

The Reserve Bank and the Australian Prudential Regulation Authority may have been surprised by the surge in housing prices in May after efforts to suppress prices in the past year but experts expect the regulators to sit tight and allow incoming housing supply to absorb the price rises.

CoreLogic’s head of research, Tim Lawless, said the latest uptick – which saw the national house price rate back to 10 per cent in the year to the end of May – was “still relatively fresh and may be short-lived”.

“Despite lower mortgage rates in May, lending conditions are tighter now than they were a year ago,” he said.

“Recent data from APRA highlights that interest-only lending is now at its lowest level since March 2013 and new mortgages with a loan to value ratio to higher than 90 per cent are at the lowest reading since March 2011.

…”The RBA will be watching this closely during forthcoming monetary policy deliberations, as the risk of overheating the housing market is one of the potential risks of lowering rates further,” ANZ’s Daniel Gradwell and David Cannington said.

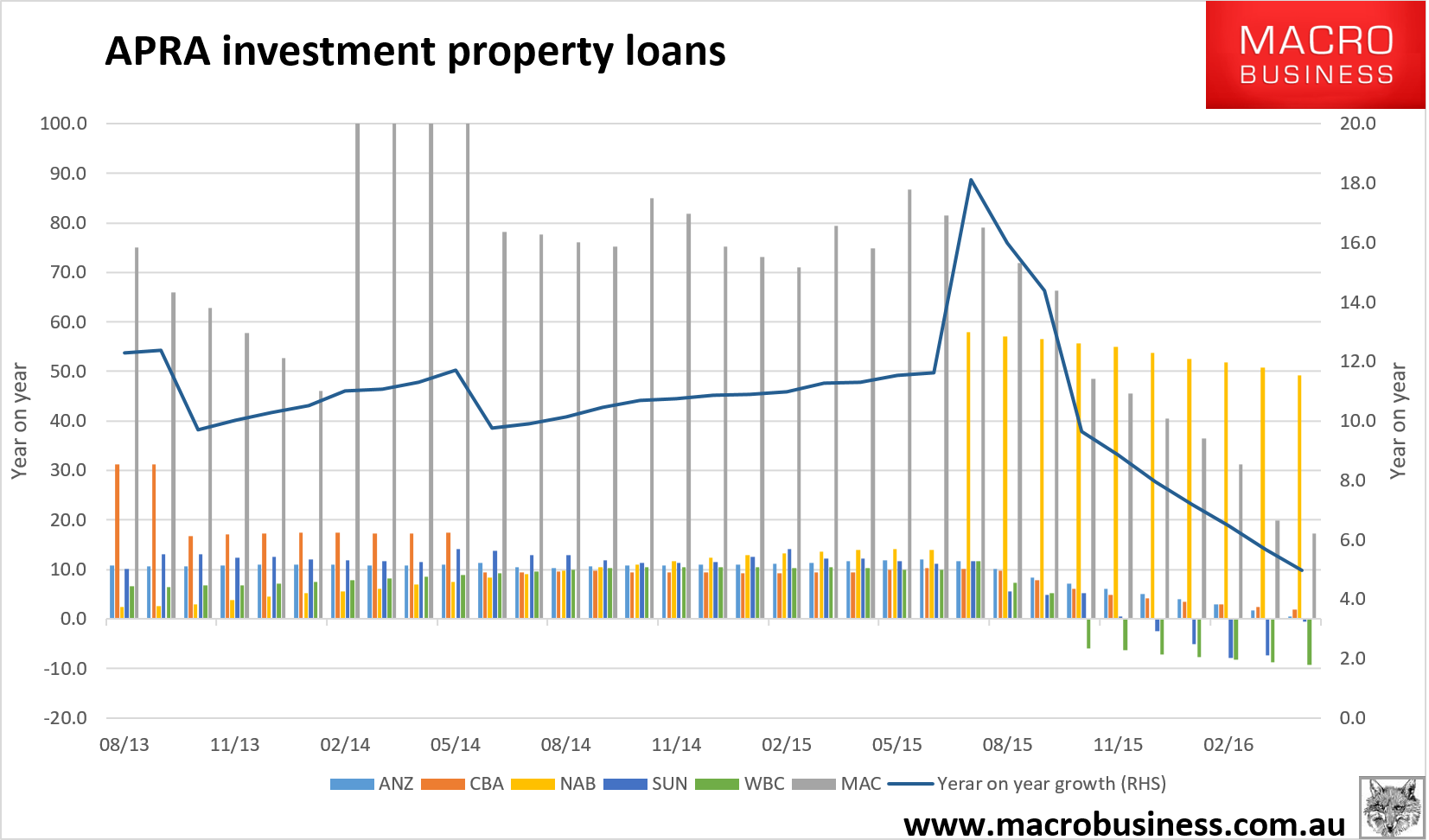

If inflation remains low, and it should, then the RBA will have to cut anyway. MB is of the view that the recent CoreLogic price jumps are untrustworthy but, even so, it’s clear that house prices are not falling off a cliff with investor lending growth at 5% for major banks on APRA data:

| ANZ | CBA | MAC | NAB | SUN | WBC | |

| Apr-16 | 0.5 | 1.9 | 17.3 | 49.3 | -0.6 | -9.3 |

| Mar-16 | 1.8 | 2.4 | 19.9 | 50.7 | -7.3 | -8.8 |

| Feb-16 | 2.9 | 3.0 | 31.2 | 51.9 | -7.9 | -8.3 |

| Jan-16 | 3.9 | 3.5 | 36.5 | 52.5 | -5.1 | -7.7 |

| Dec-15 | 5.0 | 4.2 | 40.6 | 53.7 | -2.5 | -7.2 |

| Nov-15 | 6.0 | 4.9 | 45.5 | 55.1 | 0.5 | -6.4 |

| Oct-15 | 7.1 | 6.1 | 48.5 | 55.6 | 5.2 | -6.0 |

| Sep-15 | 8.4 | 7.9 | 66.3 | 56.6 | 4.8 | 5.2 |

| Aug-15 | 10.2 | 9.7 | 72.0 | 57.0 | 5.6 | 7.3 |

| Jul-15 | 11.7 | 10.1 | 79.1 | 58.0 | 11.7 | 11.7 |

| Jun-15 | 12.0 | 10.2 | 81.6 | 14.0 | 11.1 | 9.9 |

| May-15 | 11.8 | 9.9 | 86.8 | 14.1 | 11.6 | 10.0 |

And the chart:

The last thing APRA wants to see is any return of competition in investor lending. One of the lessons from NZ macroprudential is that you need to keep tightening or it will rebound. Banks are already dropping owner occupier credit standards and, frankly, APRA should be moving on that front too. And may already be, also from the AFR:

Lenders are discreetly imposing tough new borrowing conditions that are reducing the amount property buyers qualify for by thousands of dollars, excluding many buyers from the market who qualified a few months ago, according to Mortgage Choice, the listed broker.

Conditions used to assess a property loan are being tightened so that living expenses are increased, assessable incomes reduced and the maximum amount borrowed cut in some cases by more than 10 per cent, the company, which has 570 brokers across the country, said.

Borrowers who sought pre-approval for a loan six months ago before looking for a new property are being told their home loan application expired and no longer qualifies, it claims.

“This is squeezing a lot of homebuyers out of the market,” said Jessica Darnbrough, a spokesperson for Mortgage Choice, the nation’s largest network of mortgage brokers

“It means customers who are applying for finance can effectively borrow thousands of dollars less than they could six months ago when the benchmark was different,” Ms Darnbrough said.

For example, six months ago couple earning net income of about $116,000 could have qualified for a loan of about $1.1 million, according to Mortgage Choice analysis.

Under the new rules they would qualify for about $70,000 less. During this period variable rates have been reduced by up to 25 basis points.

Good. APRA should also protect the gains it has already made and lower its investor lending cap again to 5% immediately.