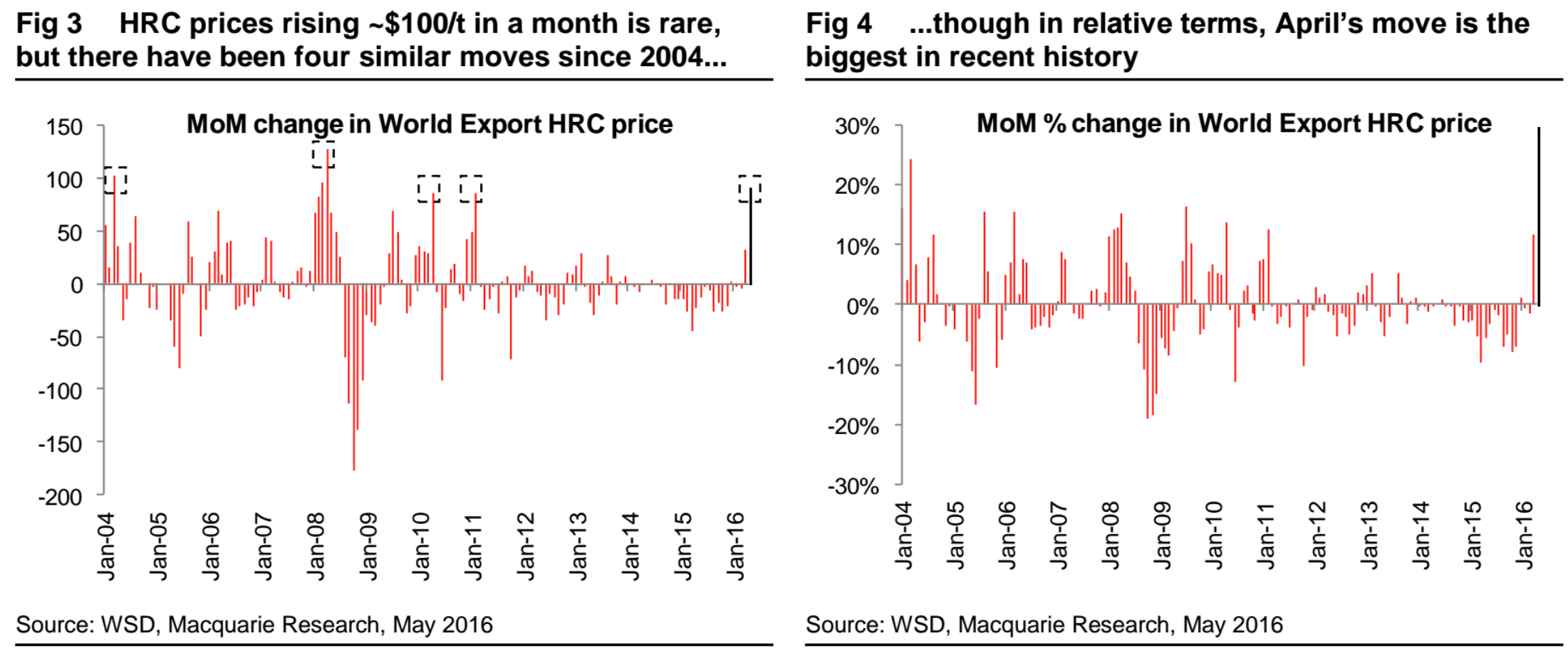

Firstly, there is the obvious one. These moves tend to take place in H1 of any year – seasonality plays a big part. The sequential rises in demand are very important as the northern hemisphere industrial economy moves out of winter. Also, previous events have taken place at times of strong global YoY demand growth, and generally when both China and ex-China are strong. Raw material constraints can help, and interestingly all have come at times of base metal prices peaking out but oil prices gaining strongly. There is no obvious correlation with inventory levels nor capacity utilisation. Chinese steel exports have generally been stable into the price moves, but risen in the subsequent months, and in three of the four precedents pricing was lower six months after the aggressive rise, each of which saw some Chinese tightening (of various degrees).

The April 2016 move does look slightly odd when compared to previous examples. While there is similarity in oil prices rising, there is no evidence of raw material constraints and, importantly, the demand environment is nothing like as aggressive as that seen in the past. The low inventories in China have clearly been an important catalyst for the April move, and hence why this is an area we will be focusing on in the current months to judge the sustainability of price moves. History also suggests Chinese steel exports pick up after rising prices (though there are barriers to this in 2016) and should we see any Chinese government tightening prices will come under pressure.

In the near term, demand is clearly strong enough to keep steel prices elevated, and certainly Q2 prices are coming in well ahead of previous expectations. However, in an environment where demand growth forecasts are barely positive (although we did recently upgrade our China assumption) and overcapacity at record levels, we struggle to see the recent gains in global steel prices being maintained save for regions with enhanced protectionism. And with the Chinese government likely to have a slight tightening bias over the coming months, Chinese prices could well lead the path lower.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.