So far as I know, MB is the only outfit that correctly called “no bottom” in the RBA’s easing cycle over the past twelve months or so. (Forgive me if that’s not entirely right. Deutsche, Macquarie and Capital Economics have all been dovish and may actually have kept their easing forecasts. But even the likes of sensible bears like Goldman lifted their outlook for a while).

Why is this so? It’s not (just) a trumpet blowing question, it matters great deal to your investment outlook why we got this right and what the lessons are. Let’s take at some sell-side post rate cut ruminations to explain. From UBS, here’s the optimist’s view:

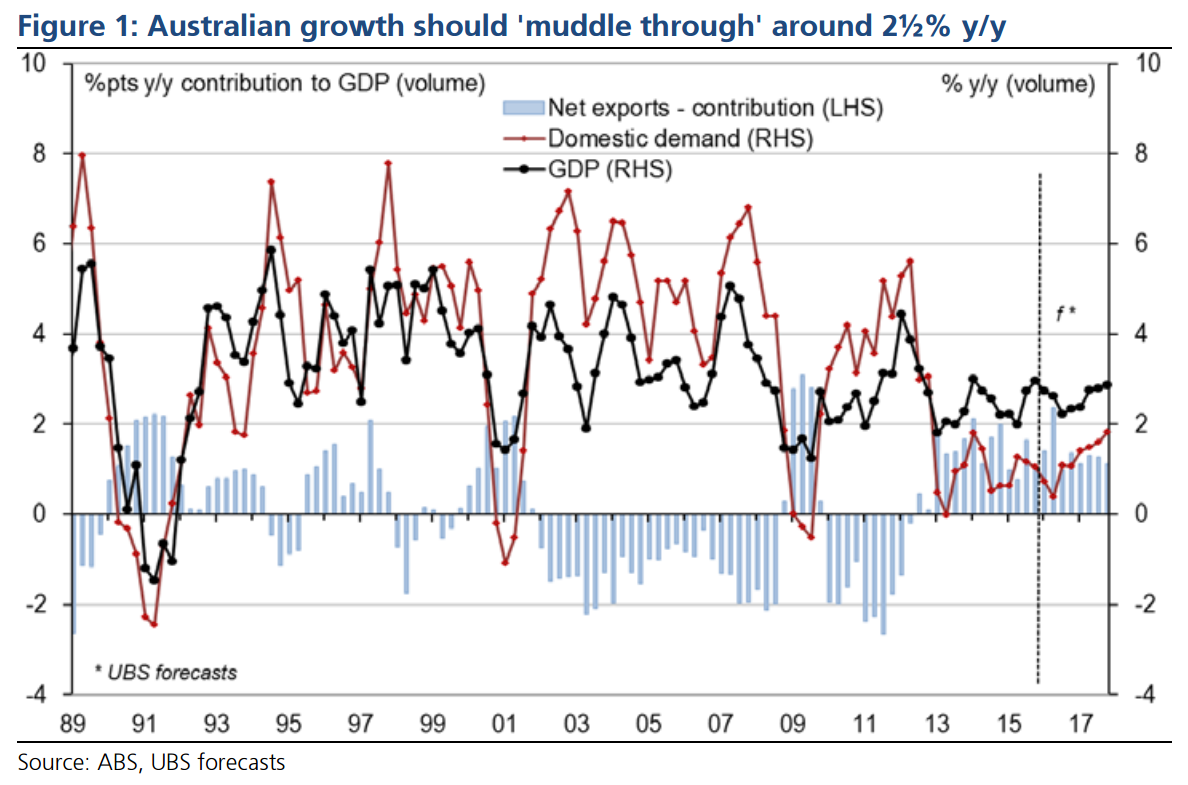

Overview: This week the RBA trimmed the cash rate 25bp to a new low of 1.75%, against our long held view that rates would most likely remain steady at 2%. While we’ve been highlighting that any move this year would be lower, the firmness in recent jobs & growth data left us a little surprised the RBA chose to cut, albeit it was much less of a surprise given the recent jump in the AUD and sub-target print for core Q1 CPI.

So where to from here? How have recent developments impacted our outlook for 2016-17? Key developments over recent weeks have been 1) upgrades to China & Europe GDP forecasts, 2) higher than expected commodity prices & AUD, 3) near-term easing in both interest rates & fiscal policy & 4) lower than expected domestic inflation.

On balance, we’re keeping our GDP outlook unchanged for 2016 & 2017, at 2.5% & 2.7%, leaving us a little below consensus (of 2.6% & 2.9%). We’ve added a follow-up RBA cut in Aug, post Q2’s CPI, which together with the modest near-term fiscal easing (~¼%pt of GDP), sees prior downside risks to growth replaced with upside risks. We continue to see the AUD heading lower (USD0.68 end-17), albeit its 2016 average is higher & more of a drag on growth. We’ve lowered our CPI forecasts, while events have tilted the growth outlook more domestic, reflected in our modest upgrades to the consumer & housing, but similar modest downgrades of ~¼%pt to net exports.

Overall, we continue to see the Australian economy ‘muddling through’ at around a 2½% y/y pace of growth over the coming year or so, as it balances the clear improvement in the domestic economy, but remains constrained by the headwinds of a still unfolding capex cliff, low commodity prices and ongoing fiscal consolidation.

And from Mac Bank, the less optimistic view:

Advertisement

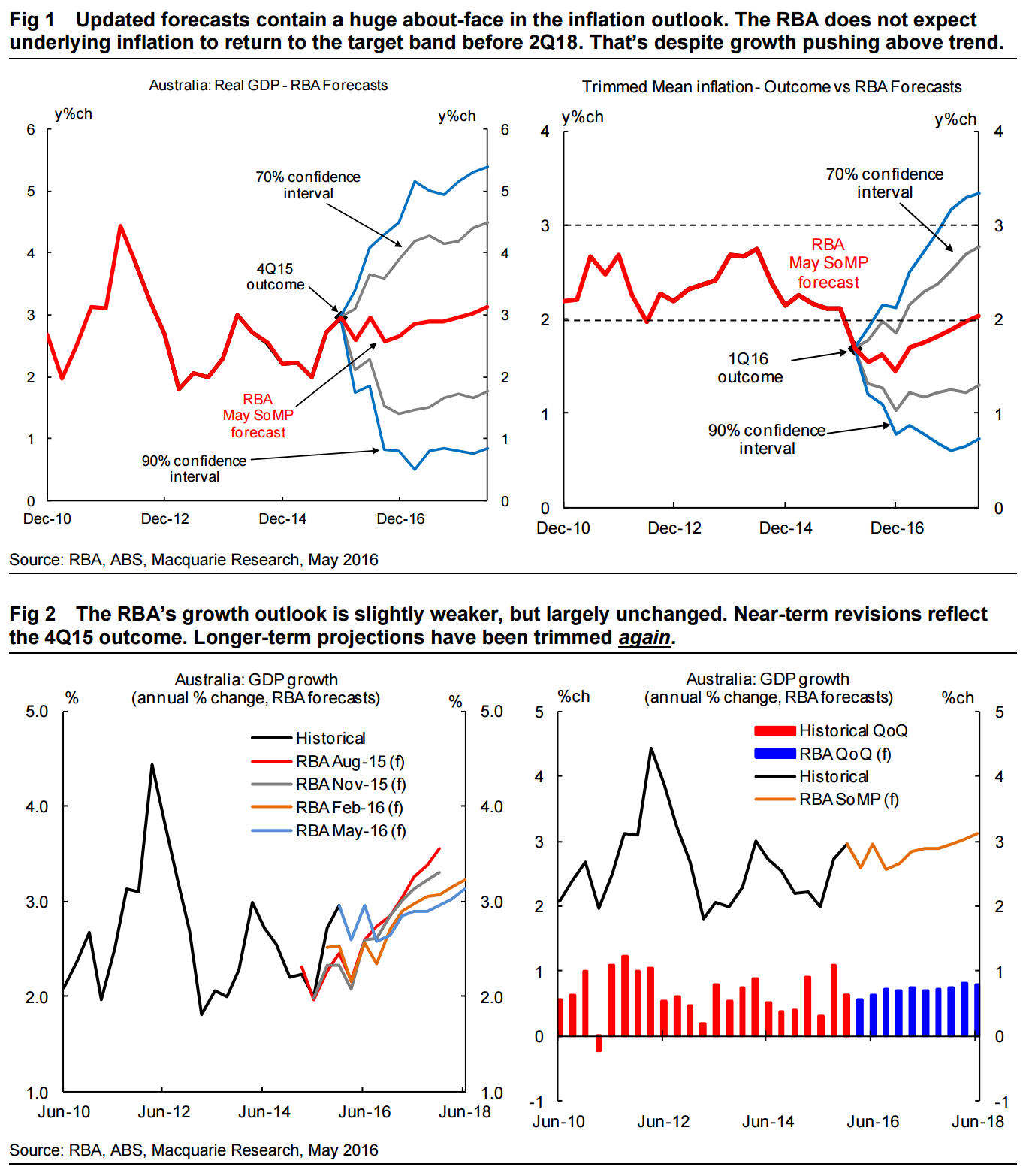

The SoMP forecasts provide a very clear message on the outlook for monetary policy. And that message is, “expect more rate cuts”.

Despite cutting the cash rate to 1.75%, and incorporating market pricing— which was factoring in a further 25bp cut—the RBA’s inflation outlook remains substantively below the bottom of the 2-3% target band. Right up until the end of the forecast horizon. In addition to incorporating an additional 25bp of easing, the RBA’s weak inflation outlook incorporates a steady, then declining, unemployment rate.

In our view, this is a big shift. We are surprised by the extent of the downgrade in the RBA’s inflation outlook. The takeaway from the forecasts is that further rate cuts are required to return inflation to the bottom of the RBA’s target band (i.e. further than current market pricing). And that any deterioration in the unemployment rate will be a further downside risk.

It is difficult to take in the RBA’s outlook changes and not come to the conclusion that the RBA will be following up with a further 25bp rate cut in August. Following the 25bp cut earlier this week, we retained our forecast for the next cut to arrive in November but acknowledged the risks of an earlier, August move. However, against the backdrop of the RBA’s updated outlook, that risk now looks to be the base case.

Following the shock 1Q16 CPI outcome, we exerted flexibility in shifting our August rate cut forecast forward to May. It is clear from the inflation outlook presented by the RBA that further flexibility is required. We think a 25bp August rate cut is now likely.

For some time, we have articulated a risk case that global disinflationary pressures, and further monetary policy easing, could drag the RBA cash rate down towards 1%. The message from the RBA’s outlook assessment is that what we previously considered a risk is also increasingly starting to look like a base case. How the economy and A$ responds to the RBA’s outlook shift and cut to 1.50% will be key to determining whether the RBA proceeds further, and when. Persistent A$ strength (i.e. >US$0.75) would, in our view, see the RBA push down towards 1.50%.

And from Deutsche the as bearish as it gets view:

The RBA has had a fundamental re-assessment of the inflation outlook. The timing on our rate cut forecasts (additional easing in August 2016 and May 2017) may not be aggressive enough

In the February 2016 Statement on Monetary Policy the RBA appeared to be forecasting quarterly core inflation outturns around 0.6% qoq. Come May, we estimate1 that the Bank sees core inflation running around 0.4% qoq for the next two quarters, before lifting to 0.5% qoq around the December quarter of this year and staying there for the next few years. As a result, the longer-term inflation forecasts published in this (i.e. the May) Statement on Monetary Policy have inflation running in a 1½ to 2½% range (two percent midpoint). Come the end of this year the Bank sees core inflation at 1½%.

While those forecasts – at least based on market reactions – appear to have been taken as somewhat dovish, as Figure 1 shows they also assume a quick end to the downtrend in core inflation outturns and indeed a reasonable reversal. That would seem to require a near-term end to the downtrend in wages growth, given the AUD is broadly within ranges seen over the past 12 months and will not, in our view, provide much additional inflation. Here we note a slightly different view on the part of the Bank, with the Statement stating that: “The substantial exchange rate depreciation over recent years is expected to continue to place some upward pressure on inflation for a time.”

As was the case in the February Statement the forecasts are prepared on the assumption that the cash rate moves in line with market forecasts. While we shouldn’t overplay this, it is worth noting that an assumption of another rate cut only gets inflation back to the bottom of the target band (using the midpoint of the 1½ to 2½% forecast range).

That means our forecasts that have the RBA cutting 25bps in August this year and May next year might not be aggressive enough. Indeed, in the run up to the June RBA board meeting we think the wage price index deserves much, much more attention than it typically gets. In a broader sense we will be shifting our focus, when it comes to the RBA, from the trend in the unemployment rate to the trend in wages growth.

Elsewhere the SMP cites: “broad-based weakness in domestic cost pressures. This is evident in the further decline in non-tradables inflation in the March quarter. In part, this reflects lower-than-expected growth in labour costs, with unit labour costs being little changed for four or more years now.”

Of course these are all still too optimistic. The Australian cash rate is going to fall as far as it can without triggering a currency crisis, we think that’s 0.50-0.75%.

Advertisement

It is very important for investors to understand why MB has been right and these banks wrong. There are three main reasons.

The bullish bias. It is simply not done to be seen to be too out of step with the RBA’s own view. This is combination of group think and access. After all, one doesn’t want to short-circuit any career opportunities by being overly critical of the bank in such a small pond.

Data dunces. Market economists almost by definition focus too much on cycle and not enough on structure. As such they miss the big drivers of growth and price changes because they are overly focused on daily data oscillations. An extreme example of this is the Kouk wind vane who predicted four rate hikes last year and another four this year based upon cyclical measures when structural drivers were clearly deteriorating.

Modelling mayhem. The neoclassical economics that underpins the training of all of the above has a basic flaw in its assumption that economies exist in a natural state of equilibrium that they will always return to. This leads them to ignore such inputs as debt which can defenestrate equilibrium for generations at a time.

So, why has MB been right where billion dollar economists have been wrong and what does that mean for the future? Basically it’s because unlike the above, MB is focused on structure over cycle, doesn’t give a hoot about the RBA’s feelings and uses all kinds of different models to understand reality. Thus it is through experience that we have reached the following conclusions about the real drivers of the Australian economy:

Advertisement

we derive income from selling dirt offshore;

we leverage that income in global markets and stick the borrowings into unproductive housing speculation at home;

that drives malinvestment and excessive household spending and a chronic current account deficit

which, over time, gives us “Double Dutch Disease” we hollow out non-endowment tradables.

Moreover, we concluded at the start of this business cycle that these imbalances have now reached a critical point and that the last of Australia’s fiscal and monetary firepower would have to used up quick smart if the broken model was to be sustained before it collapses anyway.

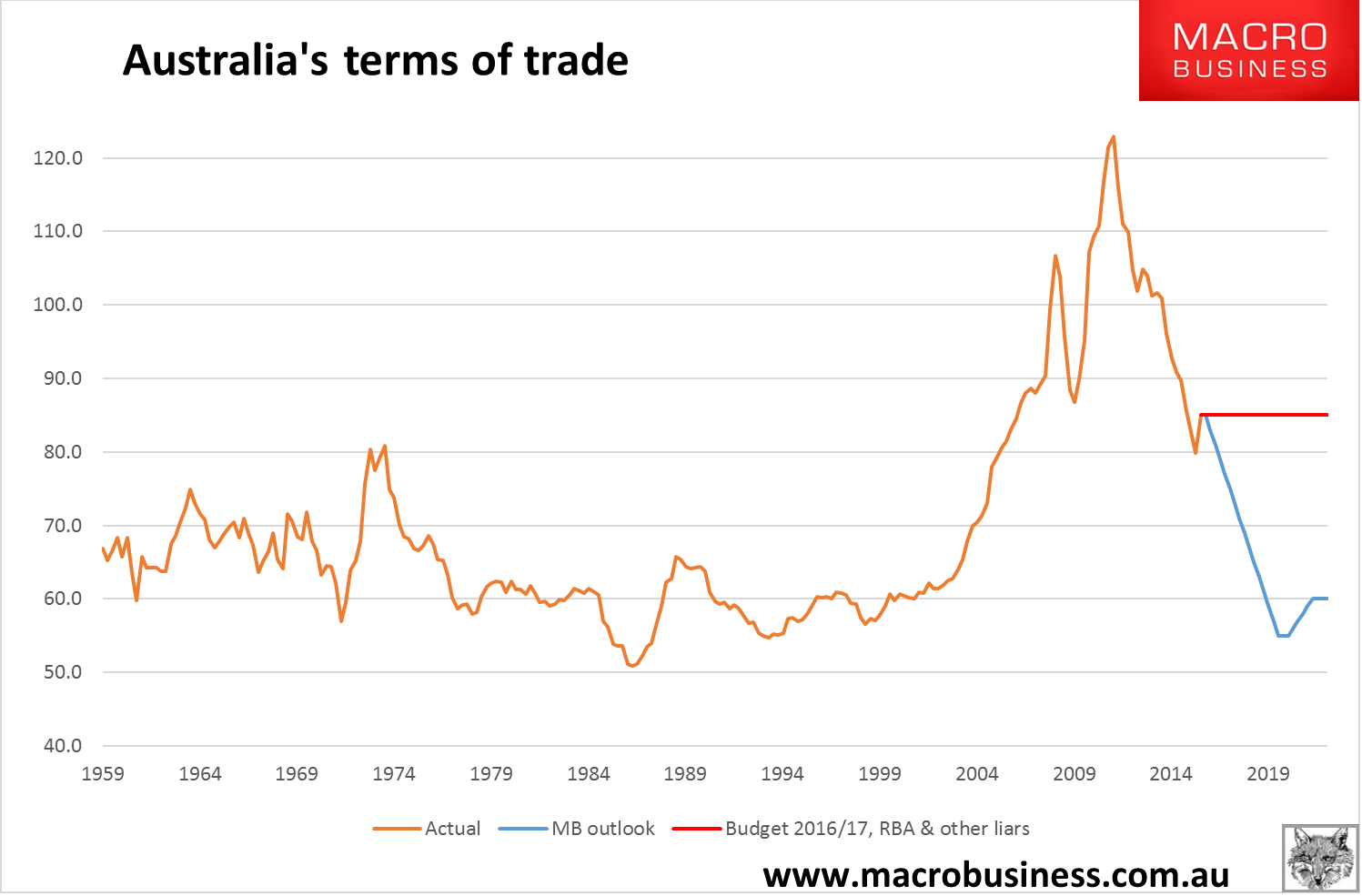

To illustrate just how far we are into this bust, and far yet it has to go, consider the following chart of Australia’s terms of trade which is the prime driver of Australian income:

Advertisement

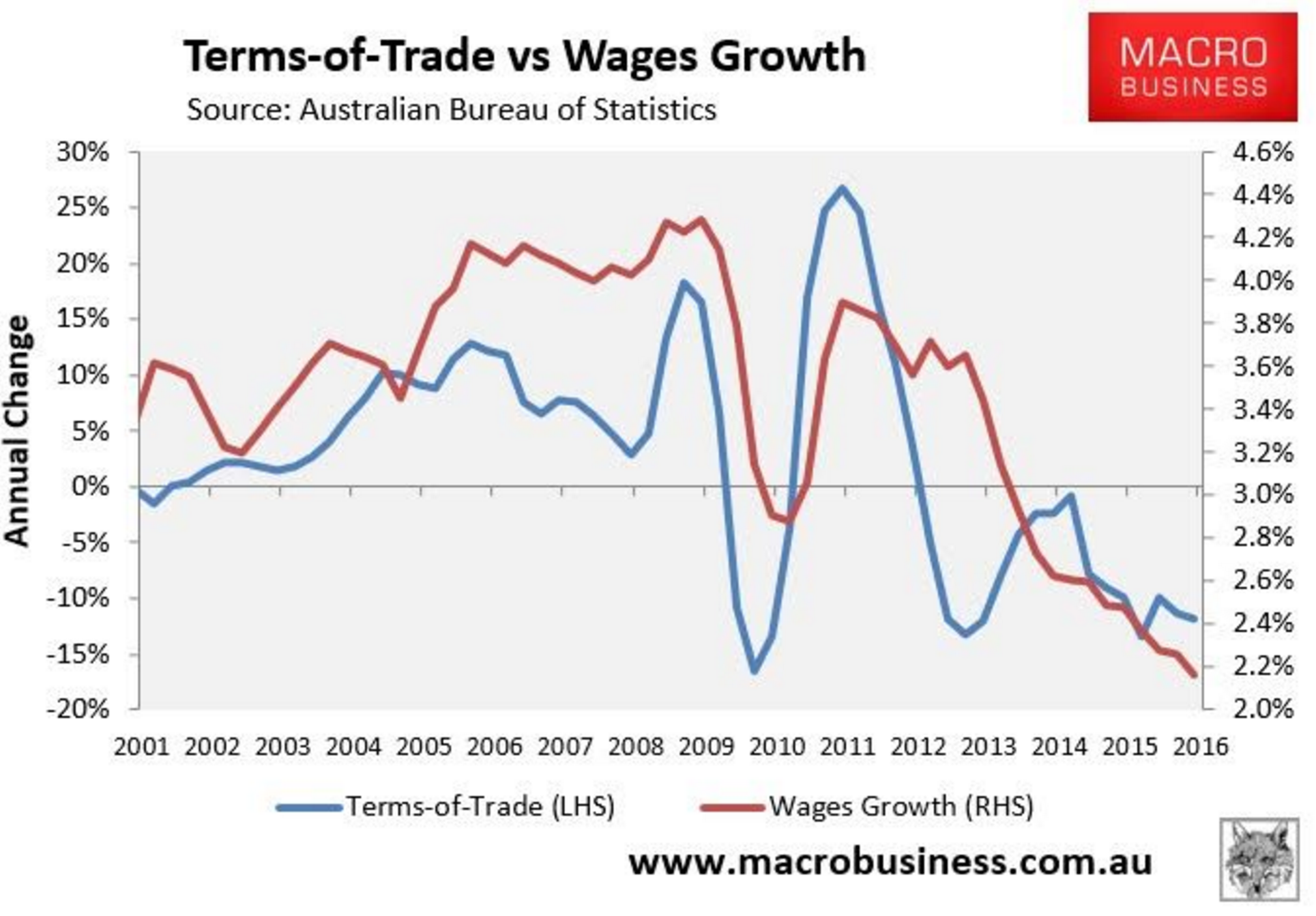

The post boom adjustment is roughly halfway through. All things equal, that means no wages growth for another five years:

Advertisement

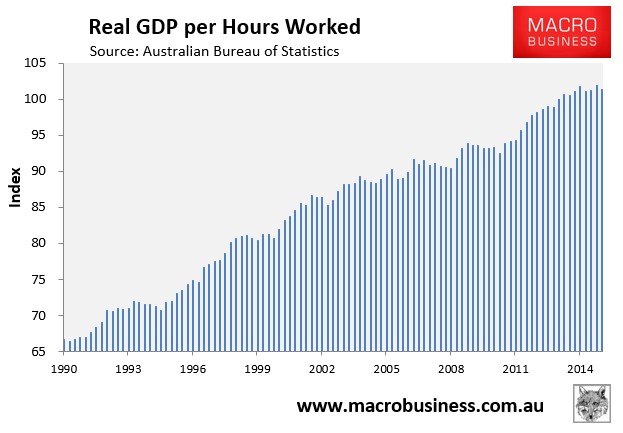

There is one way to short-circuit this process and that is to improve productivity which also grows incomes. We have already seen the bust to date mitigated a little by improving labour productivity:

But the improvement stalled two years and the more important measure of multi-factor productivity (which includes capital) is falling.

Advertisement

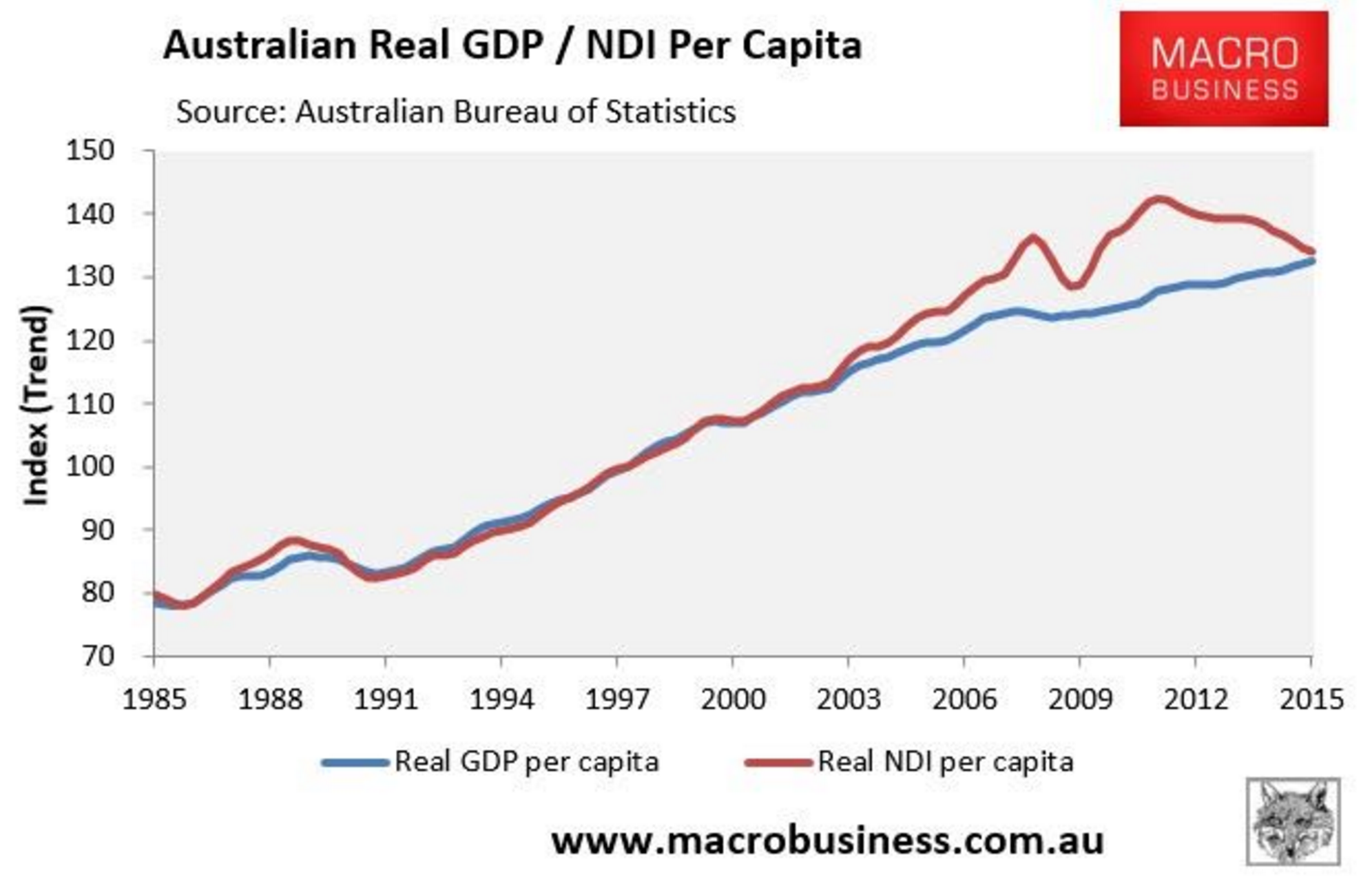

In short, the structural drivers of Australian growth will continue to push down income until it meets productive capacity and then overshoot below it for a long period as well before the two eventually reconnect:

As that process transpires, the only way to grow is to borrow more and thus the rate of interest must keep falling. It is already so low that it is likely to fall to our equivalent of zero before the adjustment is complete meaning that the economy will still need to find new growth drivers once we run out of rate cuts. That means further deflation and improvements to competitiveness will be needed to restore tradable sector growth. It’s a multi-generational bust we’re talking about here that will wring the excesses from Australia one squeeze at a time.

Advertisement

That’s how MB outgunned everyone on interest rates. We looked where nobody else dared.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.