The Australian’s Adam Creighton has continues to fight the good inter-generational fight, penning another ripping post on why one’s principal place of residence needs to be brought into the assets test for the Aged Pension if Australia has any hope of restoring the Budget back to health:

The elephant in the room at policy HQ is not superannuation but the family home.

The government’s planned renovations to the super tax architecture will not save it money unless the eligibility test of the Age Pension is severely tightened to include housing.

The proposed super tweaks will see a nation already obsessed with property… pour yet more of its savings into accommodation…

The family home — the value of which has enjoyed a remarkable, unexpected appreciation — is the ultimate tax shelter, not even counted for the purposes of social security payments…

So long as housing and financial wealth are treated so differently that discrepancy will widen and attempts to make the retirement system more sustainable will fail.

Taxes on income and consumption will grind higher, too, further undermining workers’ ability to buy a house if they don’t stand to inherit one.

As asset prices soar it is better that their owners tap their value to support themselves rather than insist other, poorer taxpayers — whose wages are now going backward in real terms — do so instead…

Brilliantly said Adam. I couldn’t agree more.

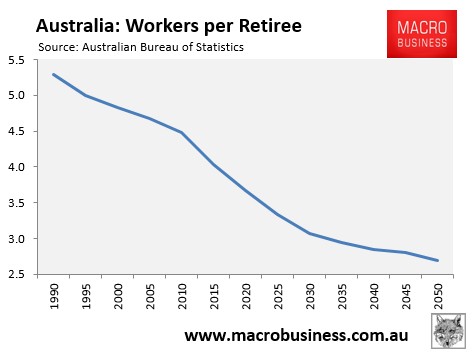

With the ratio of workers supporting retirees set to decline for decades, reforming the Aged Pension system will become inevitable, so better to achieve reform by targeting cuts at wealthier pensioners while helping the poorer ones.

Last year, the National Centre of Social and Economic Modelling (NATSEM) showed that around 260,000 Australian households have a net worth of more than $3m and yet are enjoying welfare payments of about $800 million a year:

Within the group of Australian households worth more than $3m, those of pension age are receiving about $3700 a year in cash payments, NATSEM found…

This shows starkly the ease with which retirees can qualify for the Age Pension — the federal government’s biggest and among the fastest-growing expense…

Ben Phillips, a principal researcher at NATSEM, confirmed the main cash payment going to high-wealth retiree households was the Age Pension..

Around 80% of retired Australians own their homes of which $926 billion in equity is locked up. Meanwhile, the Aged Pension (currently $44.2 billion in 2015-16 and rising to $50.4 billion by 2018-19) is the largest and one of the fastest-growing Budget expenses. This makes reform an absolute priority. My long-standing solution is:

- For one’s principal place of residence to be included in the assets test for the Aged Pension at some point in the future (e.g. 1 July 2020), thus allowing current retirees and prospective retirees adequate time to make arrangements.

- Replacing stamp duties for everyone with a broad-based land values tax.

- Extend the existing state sponsored reverse mortgage scheme, the Pension Loans Scheme, to all people of retirement age so that asset (house) rich retirees can continue to receive a regular income stream in exchange for a HECS-style liability that is recoverable from the person’s estate upon death, or upon sale of the person’s home (whichever comes first).

Under this plan, house-rich pensioners could continue to receive an income stream as they do now under the Aged Pension, but with less drain on the Budget and on younger taxpayers. The stamp duty to land tax switch would also deliver more efficient use of the housing stock.

Other notable analysts have also called for the family home to be included in the assets test for the Aged Pension, including The Productivity Commission, The Grattan Institute, The ACCI, and the The CIS.

Unfortunately, while the economics is straight forward, the political economy is not. Watch landed retirees fight like wounded bulls against reform.