Just kidding, both are sells. But right now the relative valuation differentials are stark, from UBS comes their weekly estimate of the earnings outlook versus current spot prices:

All else equal, our BHP & RIO earnings estimates for CY16E would be 97,815% (very low base) and 150% higher respectively, under a spot scenario. At spot, S32’s CY 16E earnings would increase 47% to US$89m. Iron ore: The spot iron ore price is 38% above our CY 16 forecast but combined with FX and freight implies a 68% upgrade to FMG’s FY 16E earnings.

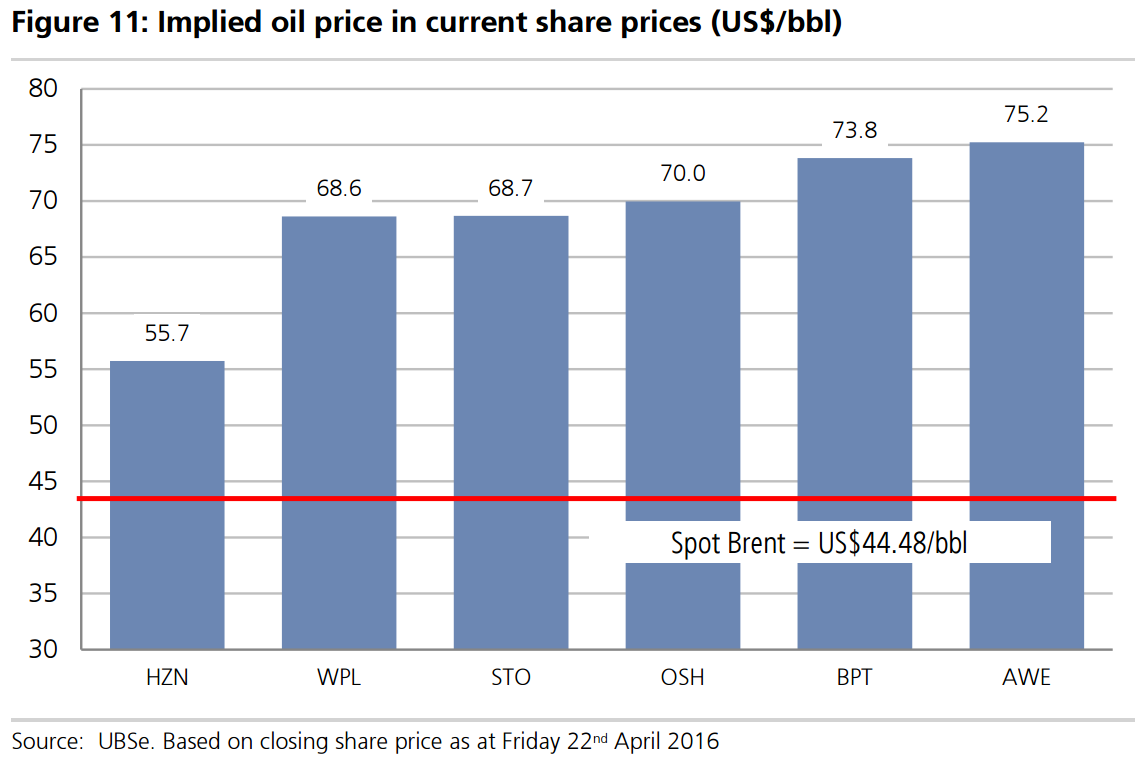

Big iron stocks are still heavily discounted (quite rightly). But for the LNG it’s the opposite:

Advertisement