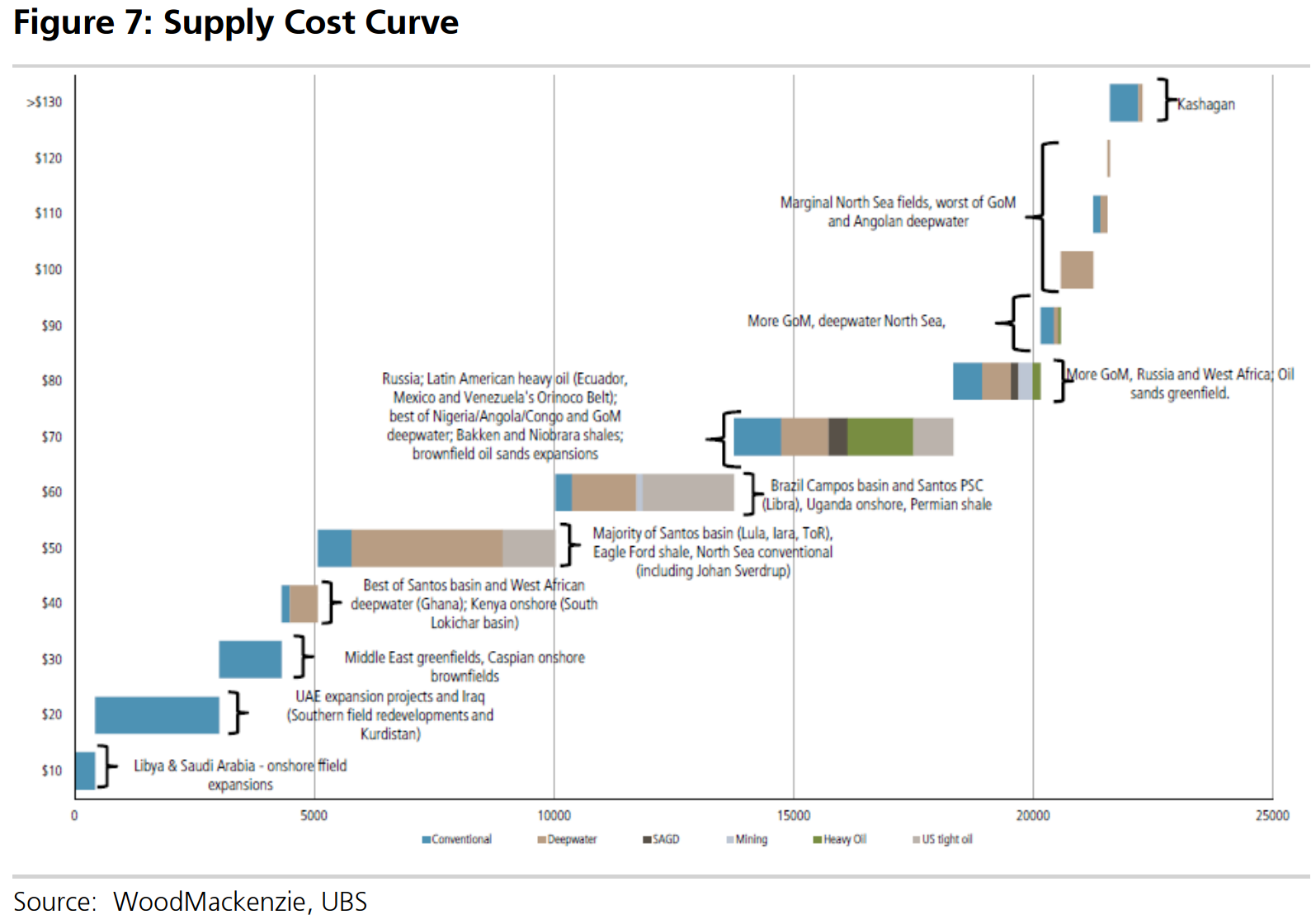

With cash cost of production for most global oil supplies well below US$40/bbl, less than 0.1% of global oil supplies have been shut in because of lower oil prices. Bringing oil markets back into balance therefore requires oil demand to increase and/or oil supplies to decline.

Unlike other commodities, oil production suffers from “natural” field decline. Oil is typically under pressure in the reservoir, so once wells are drilled, oil will flow into the well and to the surface due to the pressure differential between the reservoir and atmosphere. Over time however, two key things occur to reduce oil production rates: 1) the pressure in the reservoir declines, reducing the flow rate…Globally, if zero capex was spent on mitigating oil decline, total oil production would decline by 8-10% per annum. However a small spend rate (recompleting wells, installing pumps etc.) can reduce this rate of decline to 3-5% per annum. With global oil supplies at approximately 95 mmbbl/d, zero investment in new crude supplies translates into annual decline rates of 3 – 5 mmbbl/d.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.