Commonwealth budget restraint required to keep AAA rating.

There has been a modest fiscal tightening in recent years, a headwind for the economy of around 1/4-1/2% of GDP. With a General Election at some point over the next six months, where the government and opposition will be releasing policy initiatives and making promises, a question for investors is whether fiscal restraint will continue.

The Commonwealth Government Budget on May 3 – just three weeks from now – will be the key signpost. In recent weeks the Prime Minister and Treasurer have indicated the budget will be “prudent and responsible” indicating some fiscal restraint will continue. Press leaks suggest this will mostly be on the expenditure side rather than in the form of new taxes.

A quick look at Australia’s recent fiscal trajectory makes it clear why restraint will be required – at least if keeping the AAA rating is a desired policy outcome.

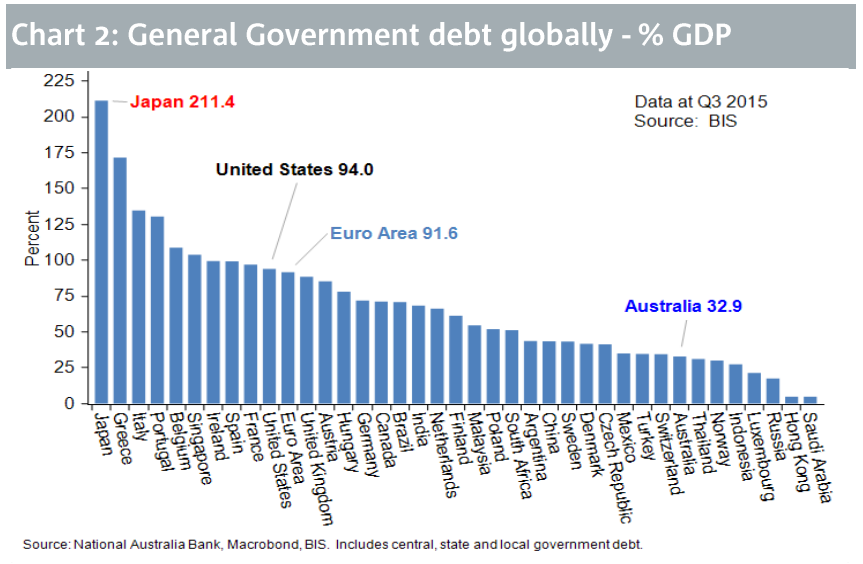

Chart 2 above shows that from the from a global perspective the gross debt of the Commonwealth, State and local governments remain fairly modest. The BIS calculated that Australia’s debt load at 32.9% of GDP at Q3 2015, considerably less that levels of 94% in the United States, 92% in Europe, and a staggering 211% in Japan.

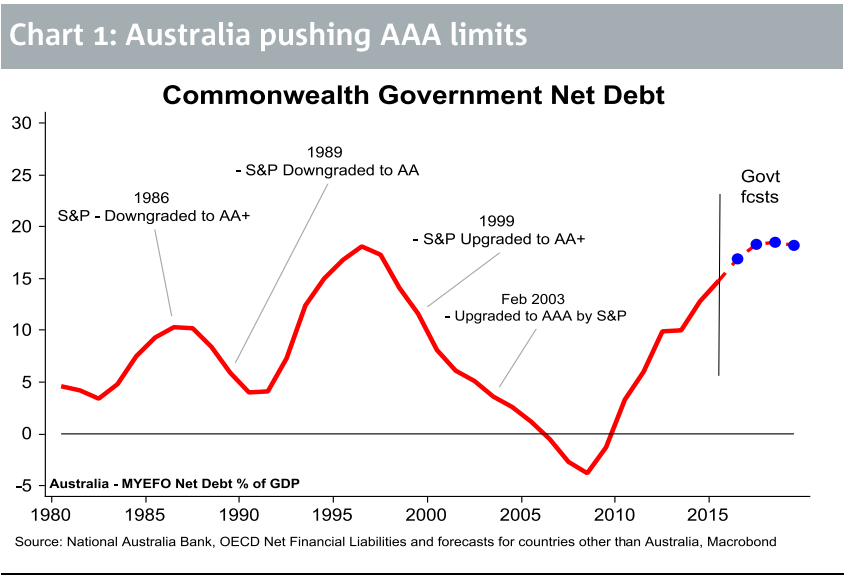

While the global comparison is healthy, a comparison to Australia’s recent past is less flattering. Chart 1 shows the Commonwealth government’s net debt as a share of GDP since 1980. The latest ratio is 15% of GDP to June 215 is above the long run average and is forecast to rise further and peak at 18.5% of GDP by June 2018.

There are more factors than simply debt load that go into ratings agency’s assessments of a sovereign’s credit worthiness. Ratings agencies also assess factors like the economy (a strength of Australia), institutional frameworks (a strength), the external liabilities of all of Australia (a weakness), monetary flexibility (a strength), as well the government’s fiscal positions (for now a strength).

What’s clear from the charts and the ratings agencies’ comments is that the Commonwealth is starting to push against the AAA boundary.

On 18 January Standard and Poor’s wrote Australia’s AAA stable outlook “is based on our assumption that Australia’s continued conservative budgetary policies will result in consistently narrowing deficits over the forecast horizon, maintaining the general government debt near or below current levels. We see strong public-sector savings as a necessary countervailing force for private-sector external indebtedness.”

The good news is that for now the ball remains in the court of the government. But it is clear that to keep the ratings agencies comfortable with Australia’s AAA, the 3 May Budget will need to demonstrate ongoing restraint. That likely means fiscal policy will remain a modest headwind for the economy.

Arguably we should already have been downgraded given private sector debt and offshore liabilities are now so much larger than they were in the late 1980s. Moreover, monetary policy and institutional frameworks are clearly losing strength.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.