Yesterday’s market action around renewed expectations for Australian monetary easing was quite discouraging. After the morning deflation shock, bank share prices took off for a bit but then got hammered through afternoon and finished down heavily. This is quite atypical for this cycle, during which falling interest rates have been the crucial support to bank valuations via the search for yield. With another round of monetary easing now inevitable, it’s time to revisit the crucial investment question of out time: when will Australian exceptionalism break at home or abroad?

Australian exceptionalism is old, enduring, deeply embedded and not to be underestimated. It has three characteristics that make it so strong. The first is domestic conformity. The second is external acquiescence. And the third is China. Each of these give the Australian economy – which is no more than a property hedge fund leveraging unstable commodity income – the gloss of a safe haven. Not until this halo of exceptionalism evaporates will Australia face its full reckoning. Will it happen in 2016?

Let’s run through the three dimensions.

Domestic exceptionalism stands upon three pillars: that the economy and housing markets and the banking system are “different”, that private debt is irrelevant, and a kind of institutional unity around the first two notions.

Yet conditions are bad. Income is stalled and falling. There is no domestic growth as the mining capex cliff keeps tumbling. Jobs are being created even as investment falls, strongly suggesting very uncertain and vulnerable labour gains. These will weaken and roll over by mid year as the residential construction boom peaks.

Advertisement

House prices are stalling and falling and will remain under pressure as the China bid evaporates and investors bunker. Perth will crash, Adelaide fall, and Sydney, Melbourne and Brisbane stall. Yet the faith remains strong. With media, government and business all hooked on the real estate bubble, punters will be cheered mercilessly on, especially when rate cuts resume as markets steadily disintegrate. The year ahead will be a titanic struggle between the powerful deflationary impulses of the Mining GFC and the rate cuts rolled out to support confidence. That struggle is about to get more pointed with renewed monetary easing some time in the next few months.

Australian economic conformity is extreme and it’s faith in cyclical responses to rate cuts verging on Pavlovian but there are two major reasons why we might expect more rate cuts to offer limited support to domestic demand. The first is that housing markets have already run hard where the conditions exist for them to do so. The second was recently summed up by Goldman Sachs:

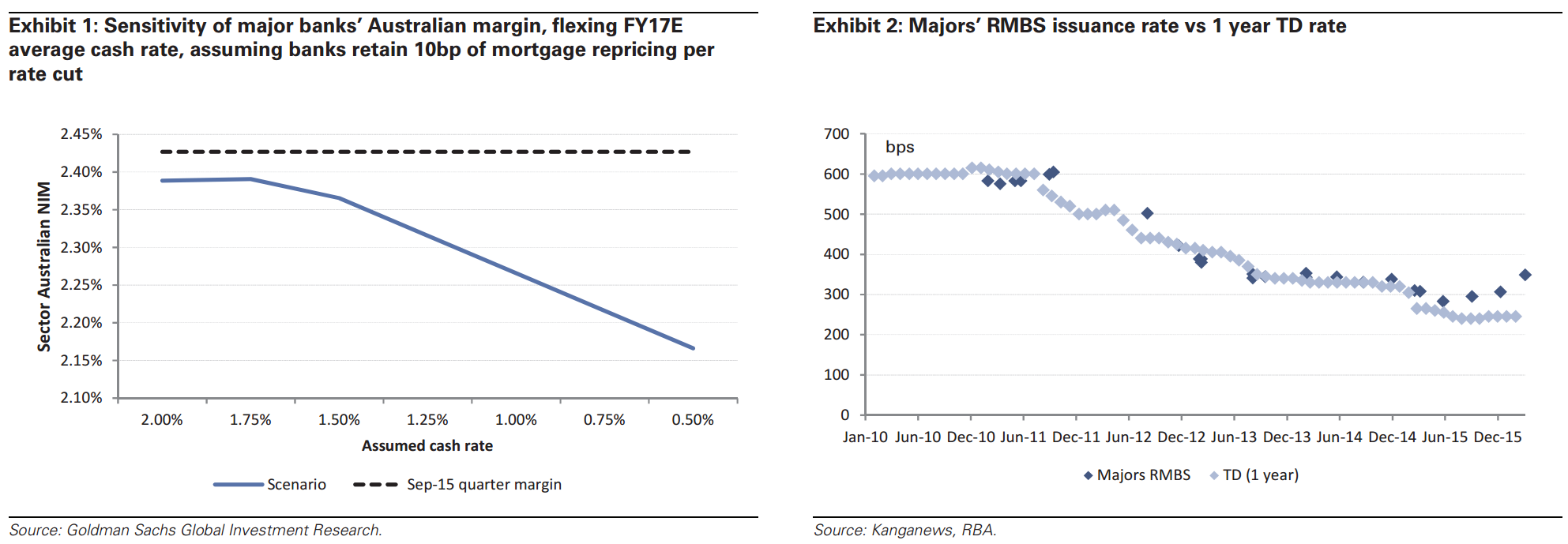

Our macro team has recently reinstated their view that the Reserve Bank of Australia (RBA) will cut cash rates two more times in CY16 (Australia and New Zealand Economics Analyst: Forecast Change: Why the RBA will cut again, February 18, 2016). In this piece we undertake a detailed, bottom-up assessment of the extent to which margins are at risk as cash rates fall, extending on the work we first published in March 2015 (Assessing the rate cut risk to banking net interest margins; prefer ANZ (CL-Buy), March 27, 2015).

We conclude that even if cash rates remain unchanged at 2.00%, margins will fall by about 4 bp versus the Sep-15 quarterly margin (previous GSe -2bp), driven by the grind lower of the replicating portfolio and higher wholesale funding costs, partially offset by the mortgage book repricing that has been announced by the banks since 4Q15. Beyond that, if we assume the major banks hold onto 10bp of mortgage repricing per rate cut then: x if cash rates fall 25bp to 1.75%, we estimate this will have no meaningful impact on margins; or x if cash rates fall 50bp to 1.50%, then margins will fall by a further 2bp, equating to a cumulative 6 bp reduction in margins versus the Sep-15 quarterly margin (Exhibit 1; versus previous GSe -2bp, therefore refer to earnings changes below).

However, if the cash rate was to fall below 1.50%, every additional rate cut thereafter would shave about 5 bp off sector margins. The sensitivity of margins to falling rates accelerates once the cash rate falls below 1.50% because the various levers the banks have at their disposal become less flexible as the cash rate approaches zero and we would particularly highlight the following:

1. Our expectation is that term deposit (and cash management to a lesser degree) pricing will become quite sticky as the cash rate falls below 2.0%, as was the experience in the both the United Kingdom and Canada in 2008/09. This will particularly be the case as the domestic banking regulator, APRA, shifts its focus in 2016 towards the Net Stable Funding Ratio (NSFR), which is likely to place pressure on the banks to both term out and improve the quality of their funding (i.e. preference for deposits over wholesale). Furthermore, we note that the recent move out in funding costs has historically correlated with higher rates being paid by the banks on deposits (Exhibit 2).

2. We estimate that the replicating portfolio represents about a 5bp p.a. margin headwind for the banks over the next 2-3 years.

Advertisement

In other words, once interest rates fall below 2%, deposit rates get sticky even as mortgage rates keep falling, crushing net interest margins. Banks will have no choice but to keep some large portion of rate cuts for themselves and that will not go down well with heavily indebted households which will hit bank credit quality. It’s a pincer on bank profits.

To this we must add that wholesale funding costs are also caught in a rising trend well ahead of other developed economies owing to our exposure falling commodities:

Advertisement

Here arises perhaps the key risk to Australian domestic exceptionalism. It was OK to have bumbling leaders when we had endless fiscal resources to waste. But as public debt-to-GDP marches inexorably higher, at some point the rating agencies will cut the AAA rating owing to the failure to reform.

Nonetheless, it is clear that with timid, politically compromised and ideologically lost leadership whatever reform path is chosen for Budget repair it will be very slow as authorities do their utmost to keep Australian households spending. There is nothing else now to drive the growth they need for incremental Budget repair: net exports and the capex crash cancel each other out, public spending can only be modest, leaving only private consumption to drive growth. Local exceptionalism is now hung squarely, and solely, upon the peg of “shop ’til you drop”.

Thus, if we are to grow and preserve the illusion of exceptionalism, we will also see the Australian current account deficit widen on consumption imports, which is already happening in trend:

Advertisement

That means that we’ll require yet more foreign funding, which is an appropriate moment to turn our assessment to the prospect for Australia’s external exceptionalism.

This is Australia’s position as a “safe haven” for global capital flows. More accurately it should be seen as as “safe harbour”, less certain. But it remains intact. As the commodity universe has fallen apart over the last four years, Australian dollar falls have lagged every other commodity currency on earth.

Advertisement

This exceptionalism is also built on three pillars:

first and foremost is the AAA sovereign rating and what it implies about the distribution of debt;

second is a larger interest rate spread to funding currencies than other developed markets;

third is Australia’s relative position as a China proxy with more robust growth prospects.

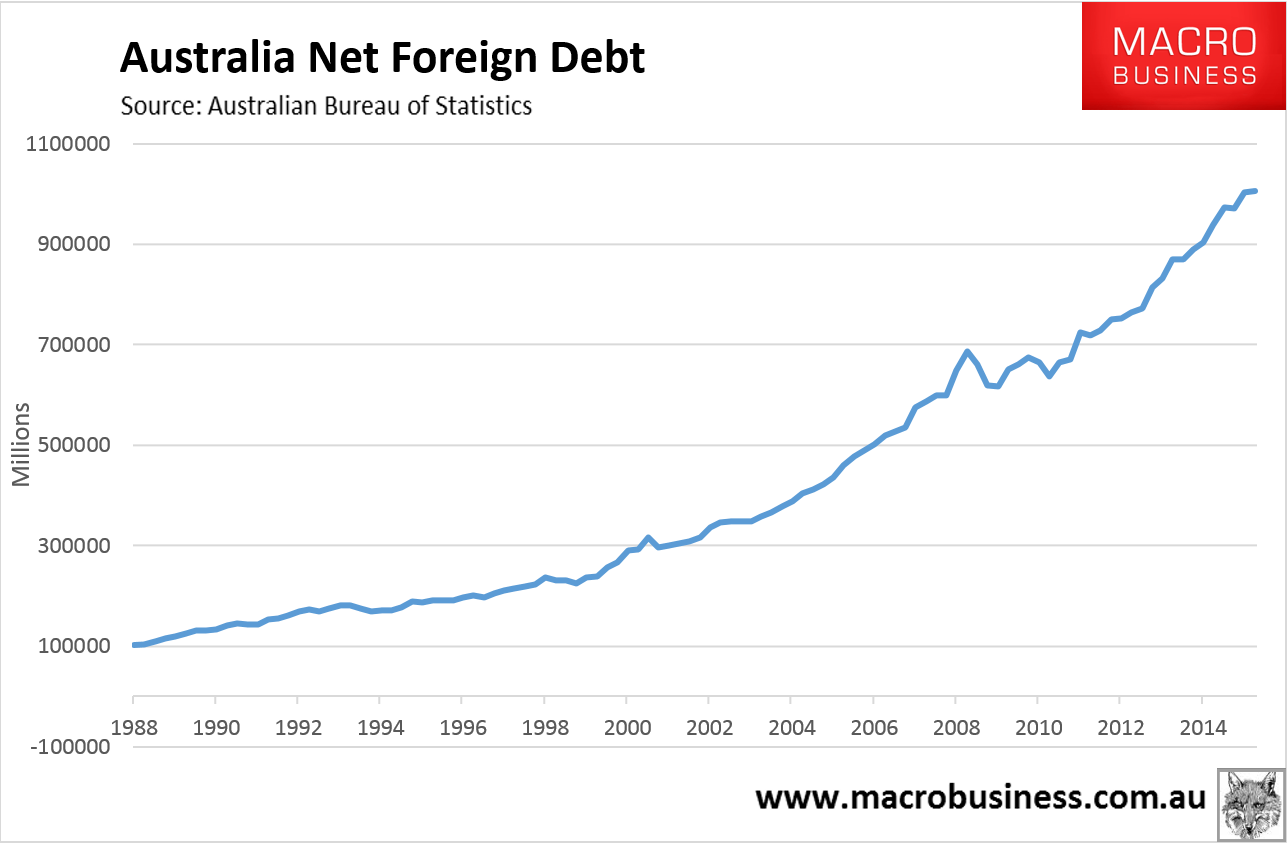

It is these three things that allow Australia to run larger and more persistent current account deficits than other nations, or, to put it another way, to sustain a bowel-shaking level of external debt without markets shitting themselves:

Advertisement

In gross terms we’re nearly at $2 trillion in external debt with a parabolic rate of climb. For comparison take Canada, which is a similar economy, which is at $600 billion.

So, how strong is each of the the three pillars of external exceptionalism?

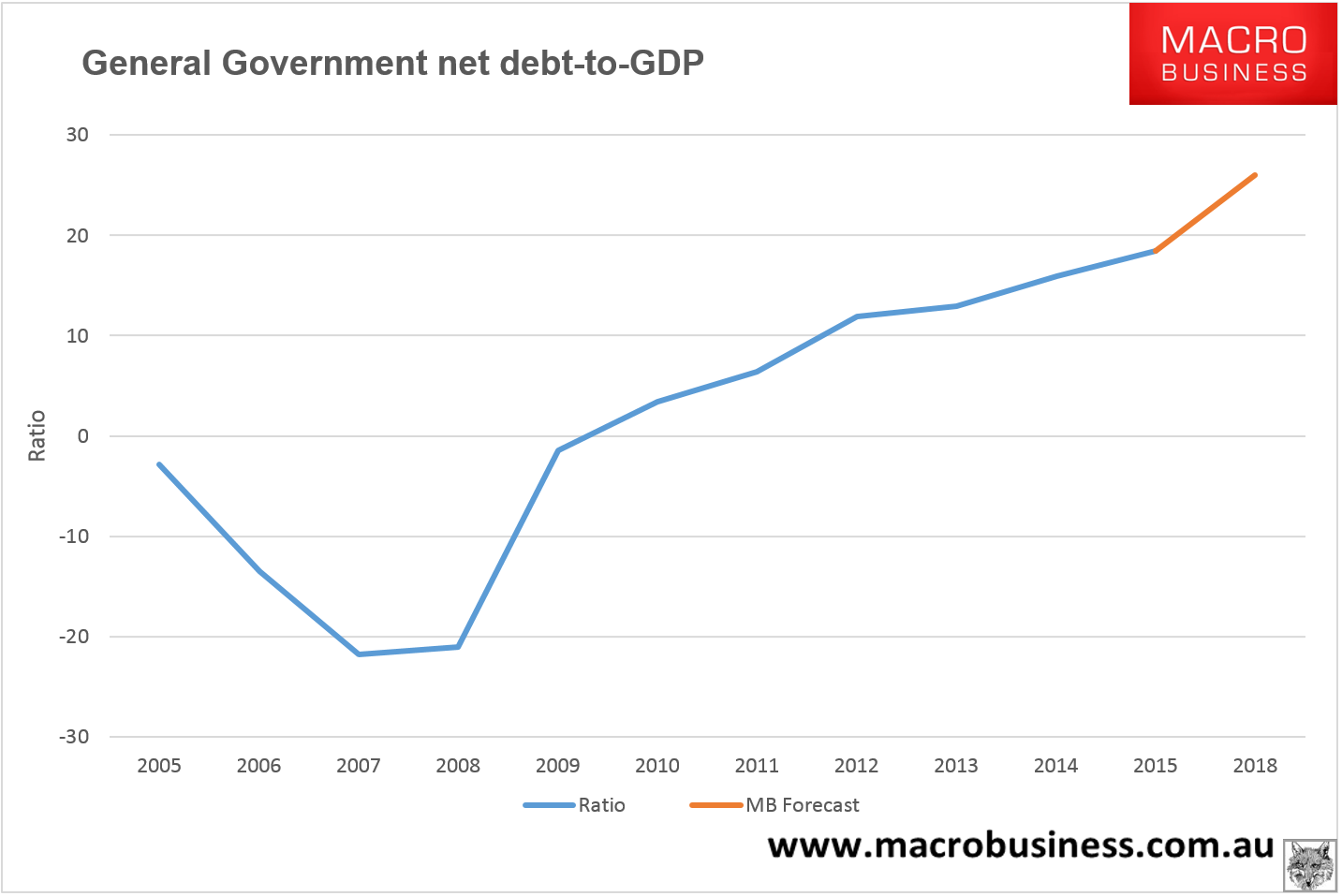

The first, the AAA rating, is not strong. The public net debt to GDP ratio is currently a (relatively) very low 18.5% and is supposed to top out in the forward estimates (or, more accurately, forward lies) in the low 20%s range but it is not going to:

Advertisement

S&P has made is clear that any breach of 30% will result in a downgrade and the realistic prospect of same will also also deliver it. Moody’s recently warned that the Budget measures to date are inadequate.

Markets are happy to fund Australia’s eye-watering external debt because it is based in the private sector. It is therefore thought to be somewhat productive, though it isn’t, given the lion’s share is used for house price speculation. That is essentially why the required AAA debt-to-GDP ratio is so low. It is S&P’s acknowledgement that, in reality, the massive external debt is permissible only because it is publicly guaranteed.

Advertisement

I doubt the rating agencies will have the cojonies to strip the rating this year but 2017 is a much stronger bet.

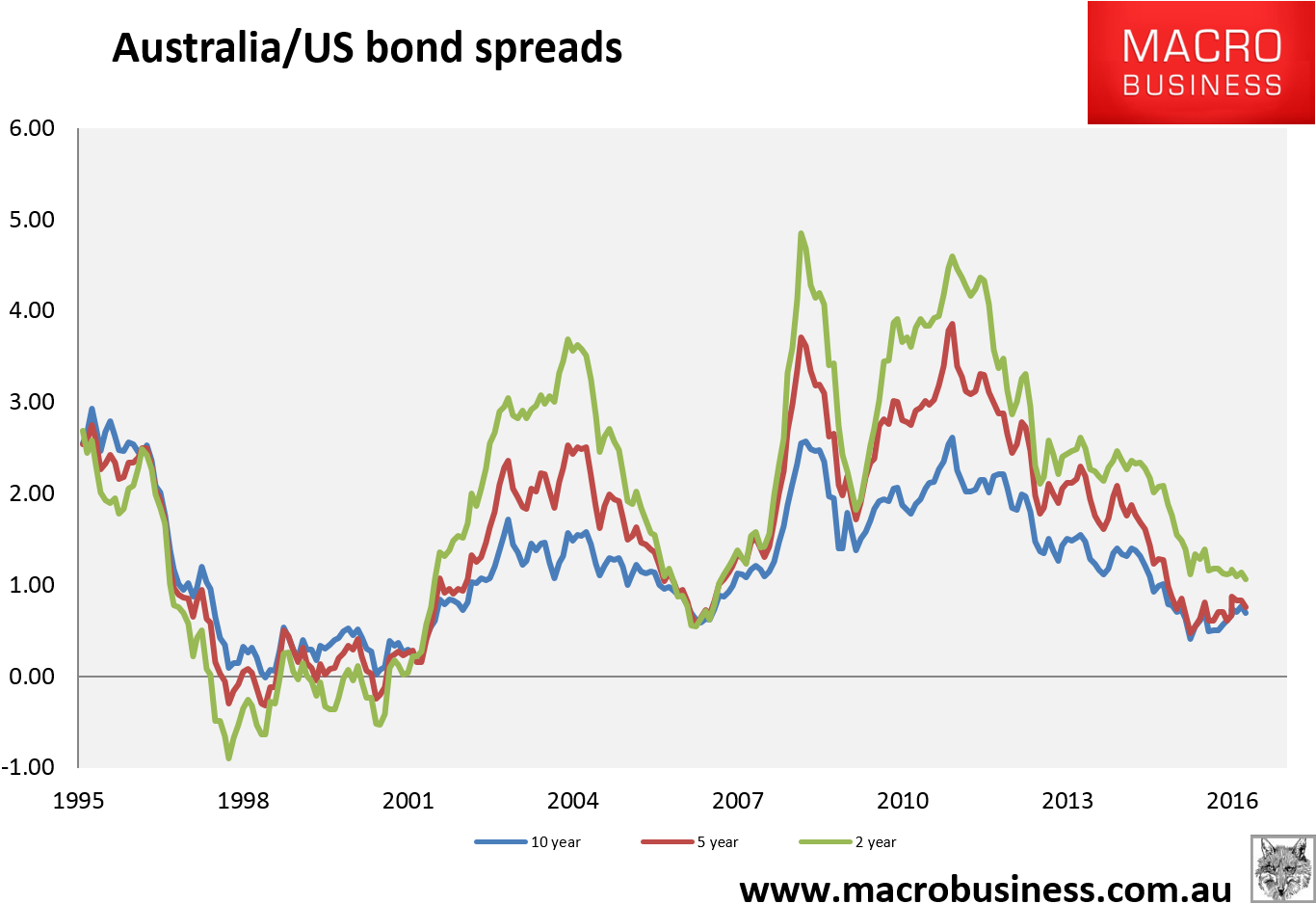

The second pillar of Australia’s external exceptionalism has also been weakening for some years as the spread between Australian yields and those of other AAA nations has been closing. More recently it has strengthened again as the US tightens while the RBA holds steady here. In fact, overnight, the spread at the short end of he curve hit its lowest point since the GFC:

Advertisement

While other jurisdictions are already at zero interest rates, further rate cuts here will by definition close the spread and weaken the pillar unless foreign central bank lunatics opt for negative rates (not impossible sadly). For Australia MB still thinks that to continue to fund the massive external debt the equivalent zero interest rate policy is in the 0.75%-1% range.

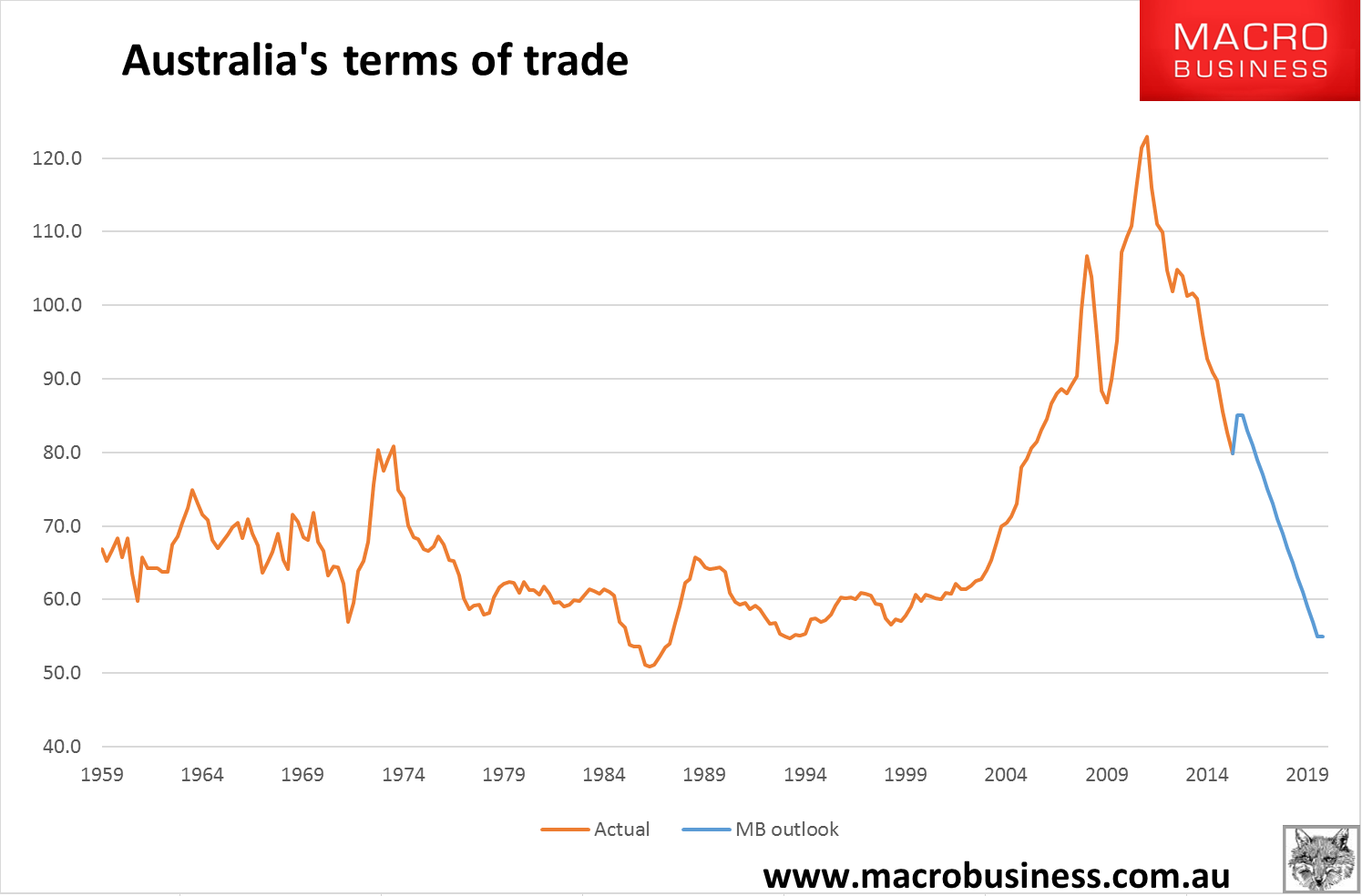

The final pillar of Australia’s external exceptionalism is our economic exposure to China. This lit up Australia as a safe harbour in the post-GFC period as our largest commodity exports exploded higher on massive Chinese stimulus when the rest of the world wallowed in balance sheet recessions. Today we’re seeing a mini-me version of that stimulus but it will pass in a few quarters (more like 2012/13 than 2009) and Australia’s terms of trade will resume falling:

Advertisement

Iron ore and coal revenues will more than halve yet and LNG severely disappoint as what promised to be $100 billion a few years ago delivers a lousy $20-30 billion instead. Services exposure may keep growing but there is no way it can offset this commodity downdraft and aggregate export revenues will keep shrinking at a good clip.

There really is no way to predict whether Australian exceptionalism will break at home or abroad first. My best bet is that it will still take an external shock to finish it off but as rate cuts resume and largely fail, it may be a close run thing. What we can say with confidence is that it is under intensifying pressure at its foundations. The greatest likelihood is that it keeps draining away through 2016 as we plod through our lost decade, punctuated by crises that make us all steadily poorer. But a tipping point in perceptions seems also to be firming, especially given 2017 looms as an outright recession prospect, and because can-kicking appears to be all we will get from a leadership that has no Plan B.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.