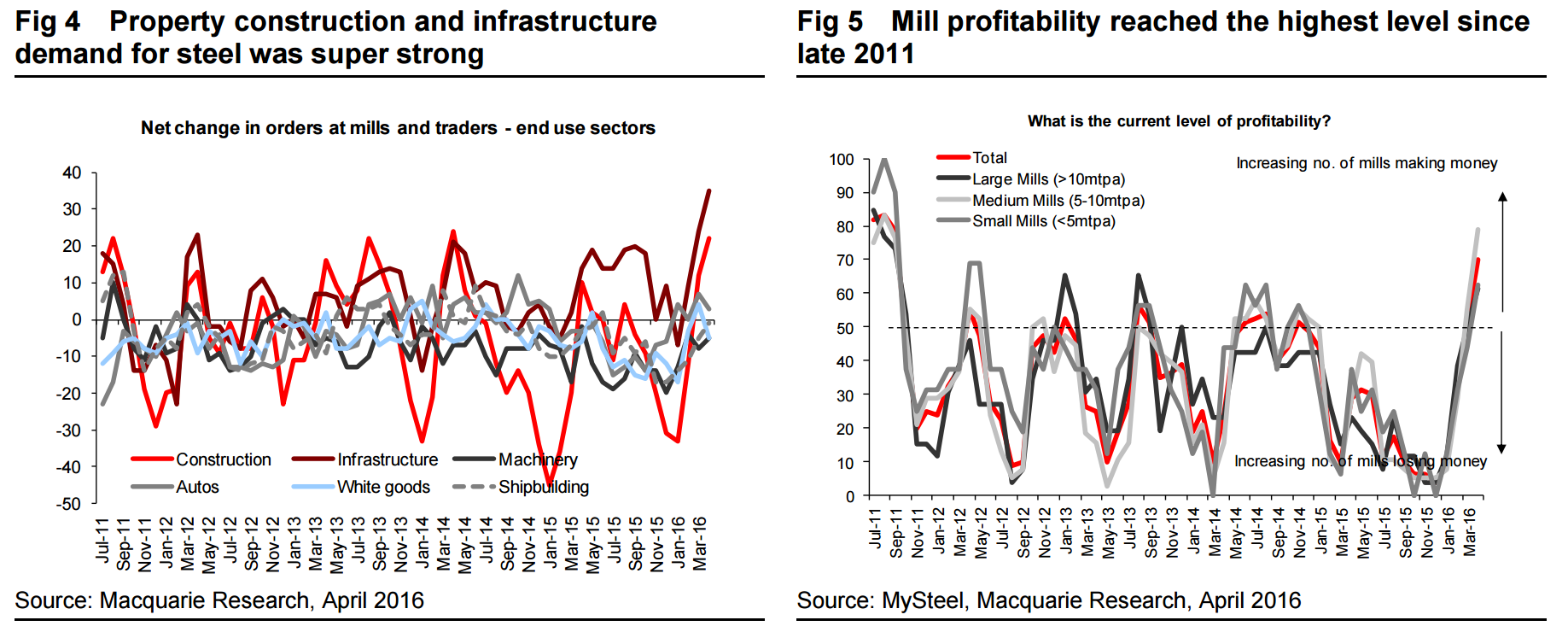

Our steel survey result for April shows a continued strengthening in demand from infrastructure and construction, with order indices for both of them reaching the highest level in the history of our survey. Sentiment among steel mills rose sharply and is now at its highest level since early 2013, while iron ore traders took a dip, perhaps reflecting the pressure from rapid supply increases from both domestic and overseas mines. With profitability also rising to the highest level in history, capacity utilisation has further recovered but still below the level seen in 1H14.

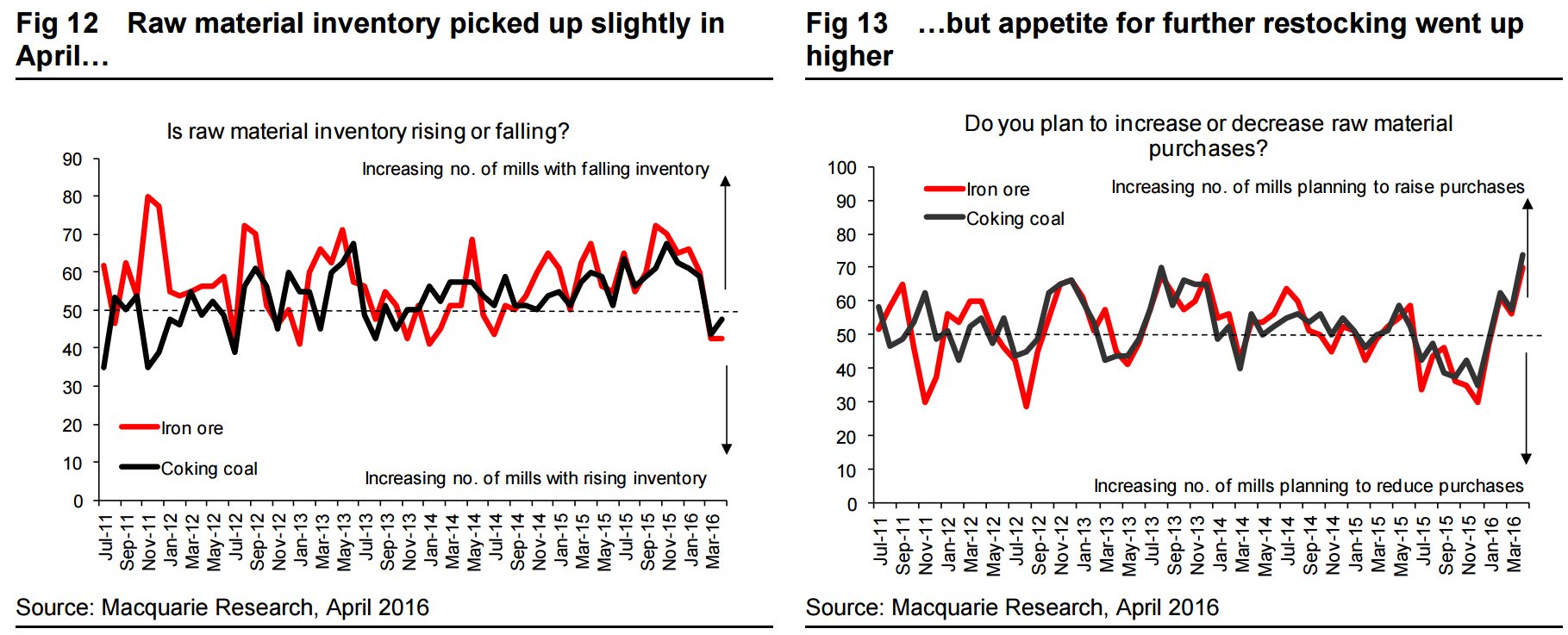

Given strong expectations of production ramp-up, mills’ appetite for raw material restocking jumped up again. Following the stronger than expected macro figures released last week, the near record steel production output in March, and an ongoing decline in steel inventories, we believe the outlook for the steel market remains positive near term.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.